That passion took him to MIT to study mathematics and later to New York, where he traded credit derivatives for Deutsche Bank AG. In 2013, after returning to Mexico, he co-founded Konfío, a start-up seeking to disrupt a market long ignored by the country’s traditional banks: credit for small and medium-sized enterprises.

A decade later, Konfío has become Mexico’s largest fintech serving this crucial segment of the economy, with 10.8 billion pesos (nearly $600 million) in outstanding loans. Its secret? Using digital tax receipts to instantly assess a borrower’s repayment capacity before approving a loan. More than 98% of the credit decisions happen in real time after the client applies online — making the process faster, cheaper and free of collateral requirements.

“The opportunity here is huge — really huge. And there’s still a lot to do,” Arana, 40, told me recently over coffee, adding that his loan portfolio is growing between 30% and 40% per year.

Konfío’s rise is emblematic of Mexico’s untapped potential. Arana and his partner Francisco Padilla saw opportunity where big banks didn’t even bother to look: Access to credit for small firms remains abysmally low, accounting for just 4% of total banking loans, well below regional peers. That chronic underperformance extends beyond finance. Whether in healthcare, insurance, energy or infrastructure, many of Mexico’s indicators lag behind those not only in developed nations but also in its Latin American neighbors. Exaggerating only slightly, one could say that in Mexico, almost everything is still waiting to be built.

Regular readers of this column already know the obstacles that have long held Mexico back: corruption and insecurity, a large informal economy, a shortage of quality jobs (especially for women), weak competition and poor public policies. This year’s disastrous judicial reform, which threatens to further undermine the rule of law, has only made matters worse. Together, these hurdles explain why Mexico’s economy has grown by just 1.7% a year on average over the past two decades, with productivity stalled.

And yet, there is still a case for optimism: If any country stands to gain from today’s shifting geopolitical and trade dynamics, it’s Latin America’s second-largest economy.

Before you dismiss my point as wishful thinking, hear me out.

To begin with, Mexico’s fundamentals are solid: The world’s 13th largest economy carries relatively low public debt, has kept inflation mostly in check and enjoys a sound banking system backed by decades of macroeconomic stability. Its 130 million people put it among the most populous nations, with a still-young median age of 30. It boasts a vast and growing domestic market, fueled in part by a minimum wage that has almost tripled in real terms since 2015 and lower poverty rates. Mexicans are hardworking, resourceful and accustomed to adapting quickly. The country’s universities produce more than 175,000 graduates in science, technology, engineering and math a year — and many of those who study abroad, like Arana, return to apply that knowledge at home.

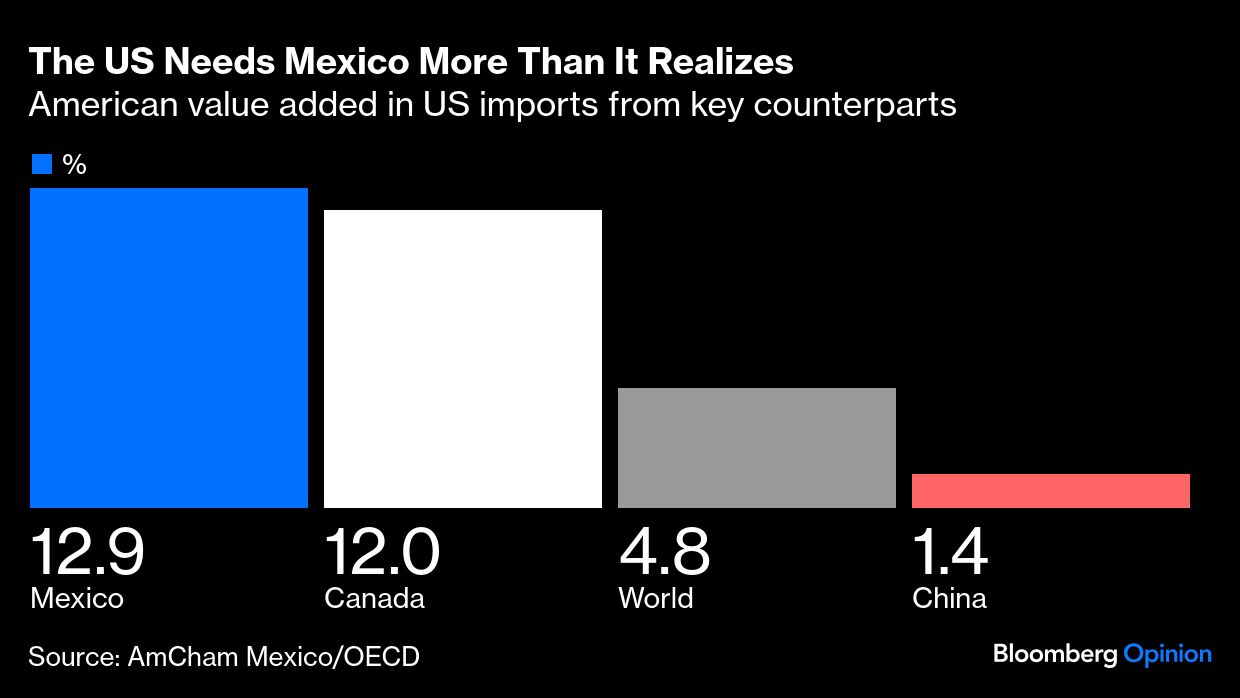

But Mexico’s biggest selling point is geography. Its free-trade deal with the US gives local exporters privileged access to the world’s largest market — a huge advantage when President Donald Trump is slapping tariffs across the globe. The US-China trade war and the 2020 replacement of NAFTA with USMCA have only deepened those ties. Mexico now accounts for nearly 16% of US imports, up from less than 13% when Trump first took office in 2017, overtaking China as its top trading partner. What’s more, Mexico has built a coproduction system with the US, where industrial inputs ping-pong from one side of the border to the other, adding value in manufactured goods such as automobiles, electronics and medical devices — while establishing resilient supply chains in the process. Despite the current climate of uncertainty, non-oil exports to the US grew 6.1% so far in 2025.

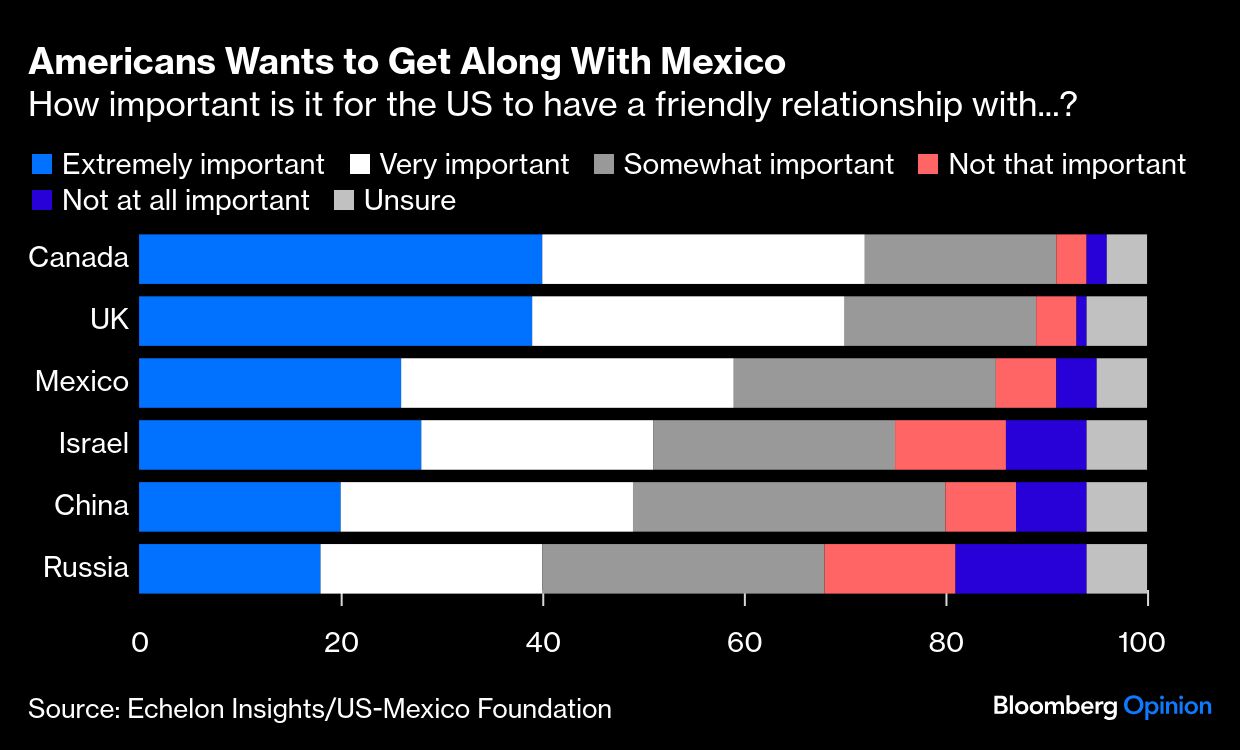

Next year’s scheduled USMCA review will likely be tough, but even with a less favorable outcome, Mexican firms will remain well positioned. Whatever the new terms, the country will look more attractive relative to other US suppliers, and if Trump’s White House is serious about an industrial revival, it won’t be able to achieve that without Mexico, which offers a younger workforce, lower costs and business and cultural affinity. For major global firms — from General Motors Co. to Netflix Inc. — expanding operations south of the border isn’t just smart; it’s a strategic necessity. Furthermore, polls suggest that despite periodic tensions, most Americans understand that maintaining good relations with Mexico is essential for the US.

As consultant Julio Madrazo puts it, “we live on the best street in the best neighborhood in the world.” Compared with other regions, Mexico faces no wars, no demographic collapse, no fiscal or pension crisis; it has geographical access to the Pacific and the Atlantic markets — and a wealthy friend next door. The problem, Madrazo adds, is that Mexico has the shabbiest house on the street: “the paint is peeling, some windoows are broken and we leave the trash outside.”

He’s right. Mexico’s biggest opportunity lies within reach — but to seize it, it must get its own house in order.

Enter Claudia Sheinbaum. Mexico’s first female president has just completed her first year in office with approval ratings above 70%. Unlike her predecessor, Andrés Manuel López Obrador, who resented private enterprise and would have nationalized everything if he could, Sheinbaum has built a constructive partnership with the business sector despite her leftist roots. Ask executives in Mexico City and they will talk of her discipline, policy expertise, tireless work ethic and clear sense of direction. Her Plan Mexico — a long-term program to promote development, import substitution and nearshoring — represents a serious attempt to reignite economic growth, which is expected to come in at just 1% this year and 1.5% next.

Sensing the moment, the World Economic Forum recently brought a delegation of 60 top business leaders, headed by BlackRock Inc.’s Larry Fink, to meet Sheinbaum at the National Palace. They spent almost two hours together, perhaps the clearest sign yet that global investors perceive something is stirring in Mexico. “There’s stronger signals now towards a business-friendly policy with investments and jobs,” WEF President Børge Brende said after the meeting.

Yet big business still needs to see more. Sheinbaum recently claimed that “Mexico is in fashion, here and around the world.” That may be true for the country’s heavenly cuisine and stunning tourist destinations, but it’s less so when it comes to an investment boom. Despite its open economy, geographical advantage and multiple free-trade agreements with 52 countries, Mexico attracts about 36% less foreign investment than Brazil — and most of that is reinvestments by companies already established here. Meanwhile, gross fixed capital formation, a key measure of domestic investment, fell almost 7% in the first seven months of the year.

There is no better way of attracting capital than by strengthening the institutional and legal framework, and that means reducing entrenched corruption, a problem where Mexico still appears at the bottom of global rankings. While Sheinbaum has shown some early success in reducing murder rates and improving overall security, there is still a long way to go to reclaim full control of the country’s territory and dismantle the criminal groups that dominate the narcotrafficking and extortion businesses.

That’s why the government must be willing to sacrifice some political dogma for the sake of speed. A flip side of Sheinbaum’s disciplined and less improvisational style is a decision-making process that moves too slowly. If the administration is serious about boosting infrastructure, Mexico should already have 20 or 30 projects worth, say, $5 billion each — ports, highways, transmission lines, renewable energy parks — under way to truly reshape the economy within a couple of years. It should rely more on private auctions and less on state-led ventures or military-managed projects. As Madrazo also says, Mexico should just get three or four large mixed infrastructure projects going and refine the model as it learns: “There won’t be a perfect new framework for public-private partnerships. Perfect is the enemy of good, and new investments are urgent to take advantage of our strengths.”

There is another powerful lever within reach in the form of private savings, with the country’s pension and investment funds already holding combined assets equivalent to over 30% of GDP. These funds could finance additional long-term infrastructure while providing solid returns for Mexican workers. But that requires greater trust in the private sector — and a recognition that business can often deliver what the government cannot, given its financial constraints and lack of technical capacity. That’s a hard admission for any statist administration to make, yet it’s essential if Mexico wants to unlock its potential. Policymakers would also do well to admit — even if privately — their dreadful track record with big projects, from the disastrous management of oil giant Pemex to white elephants such as the $25-billion-plus Maya train.

It’s been more than 30 years since Mexico joined the rich nations’ club — the Organisation for Economic Co-operation and Development — a move that raised some eyebrows back in 1994. The country still has all it takes to reach developed-nation status; if it fails to do so now, it will have only itself to blame.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.