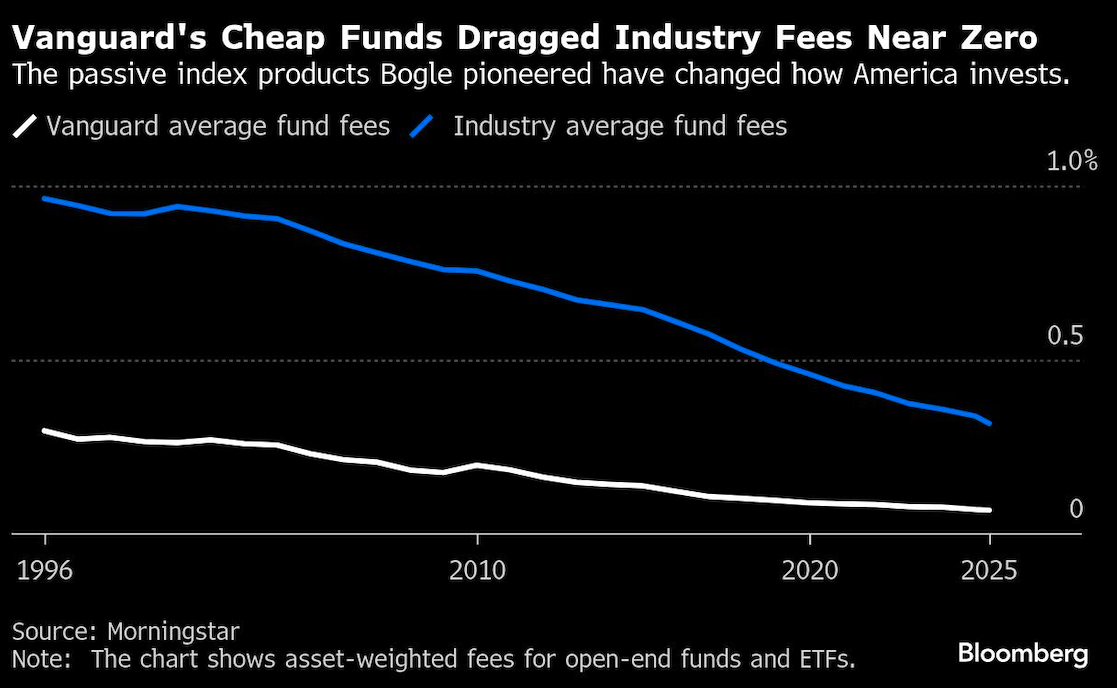

For half a century, Vanguard has been the high priest of passive investing. Its low-cost index funds have reshaped finance, humbled stockpickers, and made the Pennsylvania-based firm an $11.6 trillion behemoth.

But now, with billions of dollars flowing in the other direction — into active exchange-traded funds, specifically — Vanguard is in an unusual position: compete, or risk becoming an afterthought in virtually the only part of the ETF industry it doesn’t dominate.

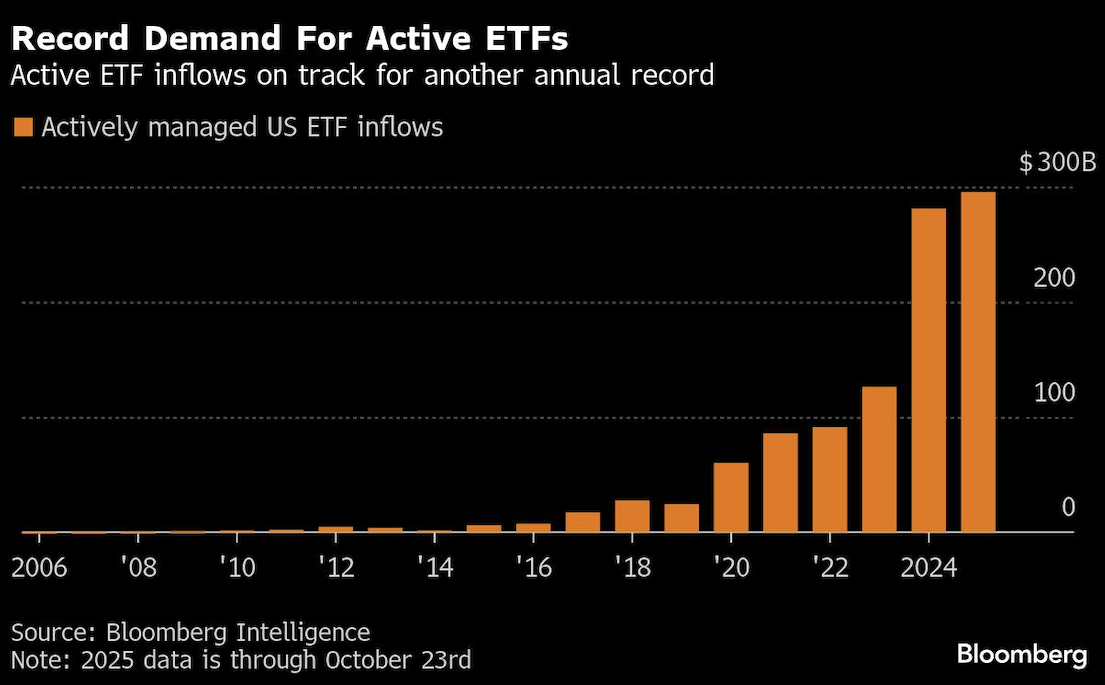

Once a sideshow, the share of actively managed ETFs in the $12.9 trillion US ETF market has doubled in less than a decade, with JPMorgan, Capital Group, and Dimensional commanding the field. In response, Vanguard has aggressively expanded its actively managed lineup this year, launching its first junk-bond offering and even filing for traditional stockpicking ETFs. So far, Vanguard is on track to launch a record seven active ETFs this year, data compiled by Bloomberg showed.

It’s a remarkable change of posture for Jack Bogle-founded Vanguard, which has become virtually synonymous with passive investing. After decades of pressuring peers to lower their fees in order to match its rock-bottom expense ratios, Vanguard is now squaring off against competitors on an uncharacteristically level playing field, one where rivals have been able to make their mark with cheap products.

“We’re in this world where the disruptor has become status quo,” said Daniel Sotiroff, senior manager research analyst at Morningstar Inc. “They were the leaders for a long time, and there’s this sense that they haven’t missed it, but they’re a little bit behind when it comes to getting more active strategies into the ETF vehicle.”

Vanguard controls about $1.9 trillion of active assets globally across its fund structures — of that, about $19 billion is in its active ETFs, according to data compiled by Bloomberg. The vast bulk of its actively managed assets sit in mutual funds, which haven’t been spared from industrywide outflows as investors gravitate to the low-cost ETF wrapper. Its focus going forward will be bringing more of its active capabilities specifically to ETFs, where its prowess is perhaps less well known, according to Ryan Barksdale, the firm’s head of active equity product.

Stiff Competition

Dimensional got a head start in the active arena by converting billions of dollars worth of its mutual funds into ETFs. It could further extend its lead in 2026 after the Securities and Exchange Commission gave its blessing for the firm to issue ETF share classes of existing mutual funds — a fund structure that Vanguard originally pioneered.

Another rival, JPMorgan, now helms both the biggest actively managed bond and equity ETFs, and ranks as the fastest-growing active asset manager over the past five years when looking at combined ETF and mutual fund flows, according to Bloomberg Intelligence data. Though Vanguard still controls a larger share of active assets than JPMorgan because of its mutual funds, its market share has declined over the past several years. That’s a rare slide for a firm that is dominant in nearly every investing category.

“We’re so well known for indexing,” said Jeffrey Johnson, Vanguard’s head of fixed-income product. “We have $1.1 trillion in active fixed-income assets, but if it’s possible for Vanguard to fly below the radar anywhere, it’s maybe been the case in active fixed income.”

Secret Sauce

While Vanguard has an uphill battle, the firm has a powerful tailwind in its relative outperformance. As of early September, about 54% of Vanguard’s active mutual funds had outperformed the S&P 500 year to date, compared with a beat rate of 45% among its mutual fund peers and 39% within active ETFs, Bloomberg Intelligence data showed. Over rolling one-year periods, beat rates for Vanguard’s actively managed mutual funds tend to be “consistently at the higher end, suggesting a durable edge,” according to a report.

Vanguard attributes the outperformance to its low costs. For example, the average weighted fee on its actively managed bond funds is just 0.1% after Vanguard unleashed its biggest-ever fee cut earlier this year, versus an industry average of 0.61% for active bond funds. Because of the low expenses, its managers don’t have to take on as much risk to justify the cost, according to Vanguard’s Johnson.

The result is consistent — though somewhat contained — excess returns. Vanguard’s active equity funds have beaten their benchmarks by 0.85% on an annualized basis over the past two decades, according to Vanguard data.

“They absolutely have the ability to generate alpha over the benchmark, but they’re not going to be swinging for the fences,” Morningstar’s Sotiroff said. “It’s actively managed on the label, but it’s not going to be super aggressive like some of the other stuff out there.”

The push into active ETFs comes as Vanguard also seeks to make inroads into two decidedly un-Vanguard-like areas: private assets and cryptocurrencies. Vanguard filed plans in partnership with Wellington Management and Blackstone in May for a retail-friendly interval fund that will invest in public equities and bonds alongside private markets. While Vanguard does offer private equity funds, they’re a minuscule part of the firm’s assets, and investors must have $5 million in Vanguard assets to invest.

The asset manager is also mulling whether to allow crypto ETFs on its platform, potentially backtracking on its decision to not offer trading of Bitcoin and Ether funds on its site. Bogle famously detested cryptocurrencies, advising investors to avoid Bitcoin “like the plague.”

Joining the Pack

While Vanguard still has many unique characteristics — chief among them, that its fund shareholders elect the firm’s board members — its recent moves have made the Valley Forge, Pennsylvania-based firm look a little more like the rest of Wall Street, according to Bloomberg Intelligence’s Eric Balchunas.

“Vanguard is slowly starting to march to the beat of the market’s drummer a little more,” said Balchunas, Bloomberg Intelligence senior ETF analyst and the author of The Bogle Effect.

Part of the spiritual shift could be attributed to the fact that for the first time in its 50-year history, Vanguard isn’t being helmed by a homegrown CEO. The firm made waves last May when it named Salim Ramji to the top job, a BlackRock veteran once considered in the running to succeed Larry Fink at the world’s biggest asset manager.

At Vanguard, Ramji has made his mark by hiring outsiders, creating a new financial advice and wealth management unit, and by pushing into unfamiliar territory for the firm. While it may seem like Vanguard is deviating away from its public ethos, it hired an outsider CEO for a reason, said Jeff DeMaso, editor and founder of The Independent Vanguard Adviser.

“It’s much easier for him to say, ‘Here’s where we can improve’ and push that,” DeMaso said. “If you’ve been somewhere for 20 or 30 years, it’s really hard to then say we need to do something differently.”

From Vanguard’s perspective, when it comes to the focus on actively managed ETFs, the firm is seemingly returning to its roots. Bogle was fired as CEO of Wellington in 1974, at loggerheads with partners over investment strategy and personnel. However, Wellington agreed to run active strategies for a fledging Vanguard, and it’s still the Boston-based firm’s largest client.

The relationship has gone on to produce a series of actively managed mutual funds and interval funds, including the Vanguard Wellington Fund — a $120 billion behemoth that ranks as one of the largest active funds globally. Still, Vanguard’s application for its first fundamental equity ETFs — filed in partnership with Wellington — are the pair’s first joint-venture in the structure.

“It’s not like we rolled out of bed yesterday and decided that we want to talk about active,” said Vanguard’s Barksdale. “We have 40 to 50 years of history.”

A message from Advisor Perspectives and VettaFi: Did you know that we provide daily updates when key market and economic indicators change? Visit the AP Charts and Analysis site to get our expert insights.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.