Federal Reserve Chair Jerome Powell agrees that there’s probably something to the claims of a K-shaped economy. But at last week’s press conference, he failed to note how the Fed has helped to create it — and the implications it has for monetary policy.

“If you listen to the earnings calls or the reports of big, public, consumer-facing companies, many of them are saying that there's a bifurcated economy there and that consumers at the lower end are struggling and buying less and shifting to lower cost products,” Powell said last week. “But that at the top, people are spending at the higher income and wealth.”

With its restrictive interest rates in recent years, the Fed has contributed to this bifurcation. Fed officials do not target a specific demographic group when setting interest rates. Their mandate is for maximum employment and stable prices for the country as a whole. Nevertheless, raising or lowering interest rates creates differences across households.

An analysis of credit card usage by researchers at the Boston Fed showed that after 2022 — the year when the Fed sharply increased its policy rate — inflation-adjusted spending by low-income consumers has nearly flatlined. Higher-income consumers have driven the aggregate growth in real spending with credit cards.

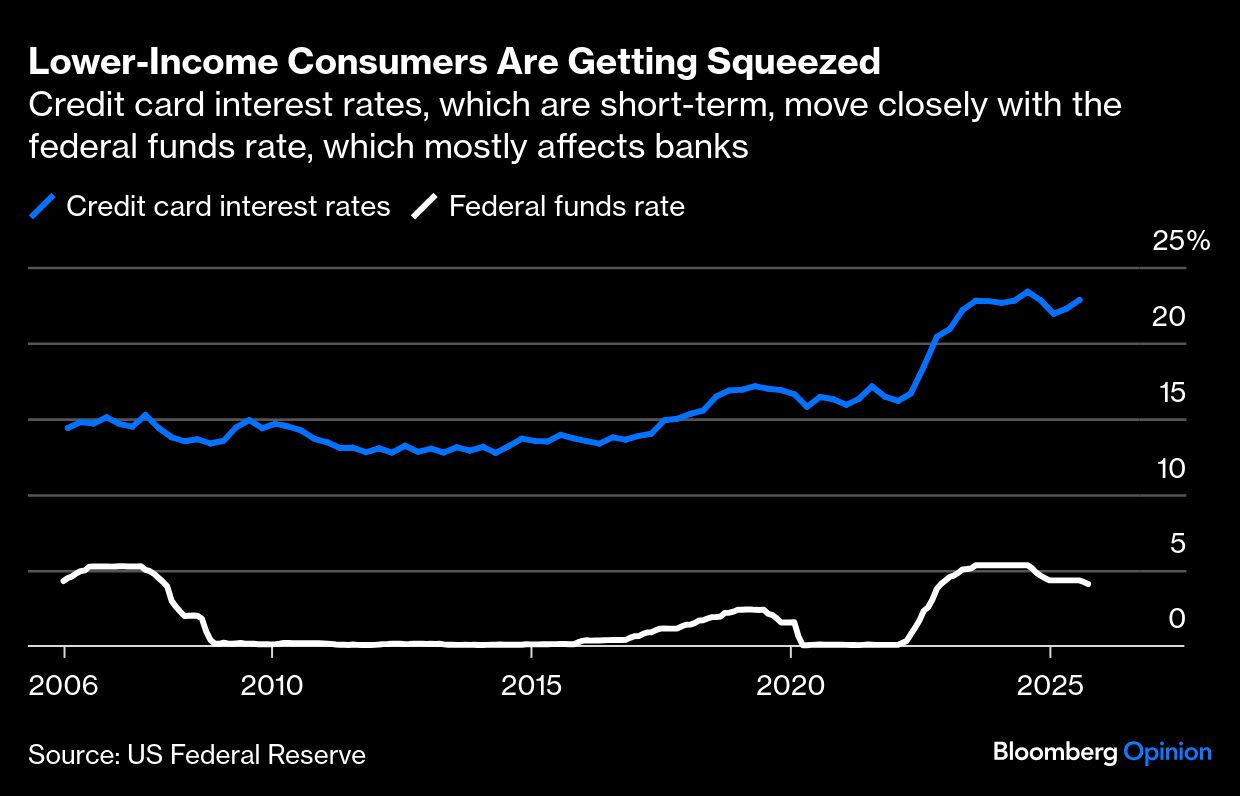

Credit-card interest rates, which are short-term, move closely with the federal funds rate, so it’s a reasonable place to look for the effects of monetary policy.

Another team of researchers used contract details in the same credit data to isolate the direct effect of an increase in the federal funds rate on credit-card spending. They found that an increase of one percentage point in the annual percentage rate of a credit card reduced aggregate card spending by almost 9% in the following month. But the pullback was far from uniform. The percent reduction was about twice as large among account holders who carry a balance on their card and those with low credit scores. Spending among those who pay off their balance each month, as well as those with high credit scores, was unaffected by the higher rates.

It makes sense that borrowers are more sensitive to changes in interest rates: They face the extra cost directly. When rates rise, the interest payments on their existing balances increase. That requires additional money to cover the borrowing cost, or a reduction in new spending. High-credit-score borrowers, who tend to have higher incomes and more liquid financial assets, followed the first path and kept spending, even paying down some of their revolving balances. Low-credit score borrowers took the second path and cut their spending.

The Fed’s goal has been to restrict overall demand to reduce overall inflation. Still, the pullback in demand is concentrated among households whose spending was already constrained, pulling down the bottom arm of the K.

The divergent effects of monetary policy on households also extend to businesses. Powell explained last week that capital expenditures in AI, which have been a driver of GDP growth, are not sensitive to interest rates. Hecited the long-run expectations about the technology. That’s a valid point. At the same time, large, profitable firms like Amazon, Meta and Google are making these investments, and the reliance on debt financing for AI investments has been limited.

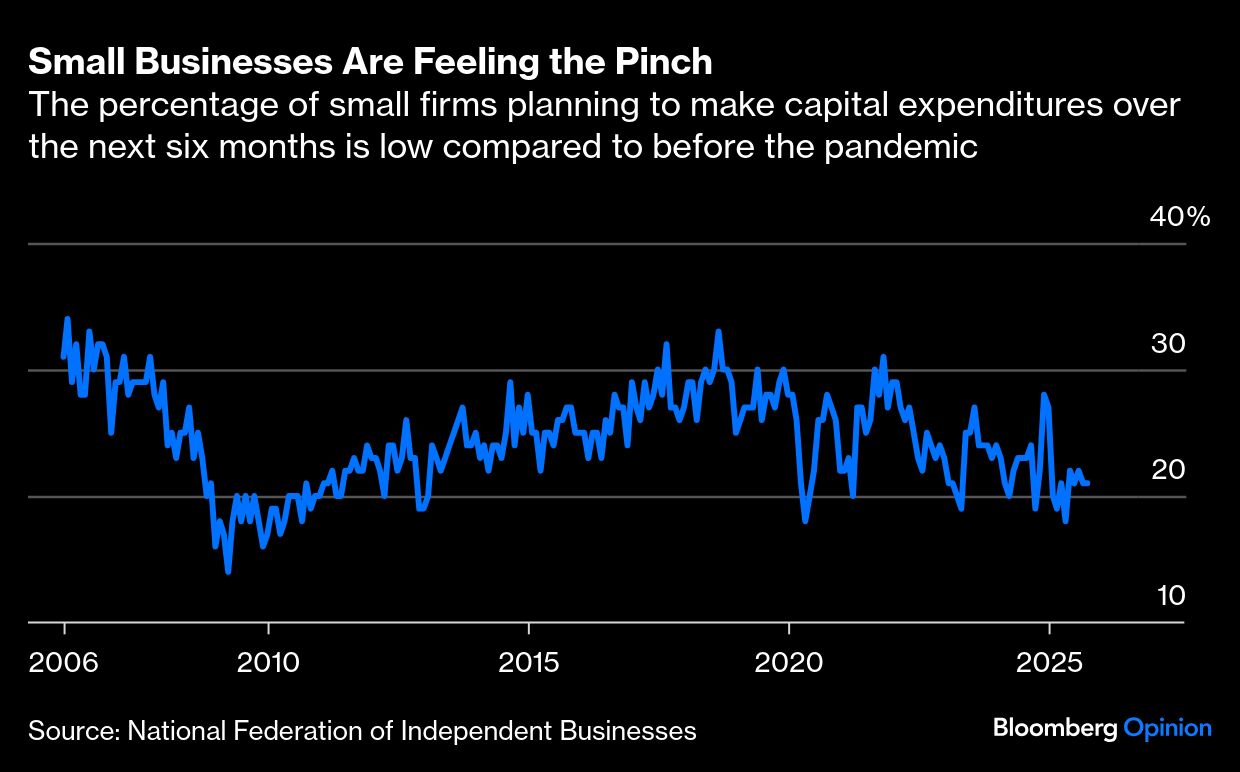

Meanwhile, research has long shown that investments by financially constrained businesses, such as young or small firms or those reliant on debt financing, react more strongly to changes in interest rates resulting from monetary policy. According to the NFIB survey of small businesses, capital expenditure plans over the next six months remain depressed relative to before the pandemic. That’s consistent with reports of elevated financing costs and greater difficulty with loan approvals. The Fed’s role in the bifurcation of business investment, like that of consumer spending, is about holding back the bottom of the K.

The K-shaped economy is both a feature and a bug of restrictive monetary policy. Interest rates are a blunt tool, far less targeted than the tax-and-transfer toolkit of fiscal policy. Even if the Fed wanted to, it would be difficult for it to rein in AI investments or shield low-income households. Increasing rates slows the economy from the bottom up, not the top down.

And just because Fed policy is contributing to the bifurcation in the economy is not a reason to cut rates. Inflation remains above the Fed’s target, and the unemployment rate is relatively low. But the slower growth at the bottom does suggest that the federal funds rate remains restrictive and there is still room to cut. It’s also a reason to be optimistic about more breadth in consumer spending and business investment as the Fed lowers rates.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Claudia Sahm