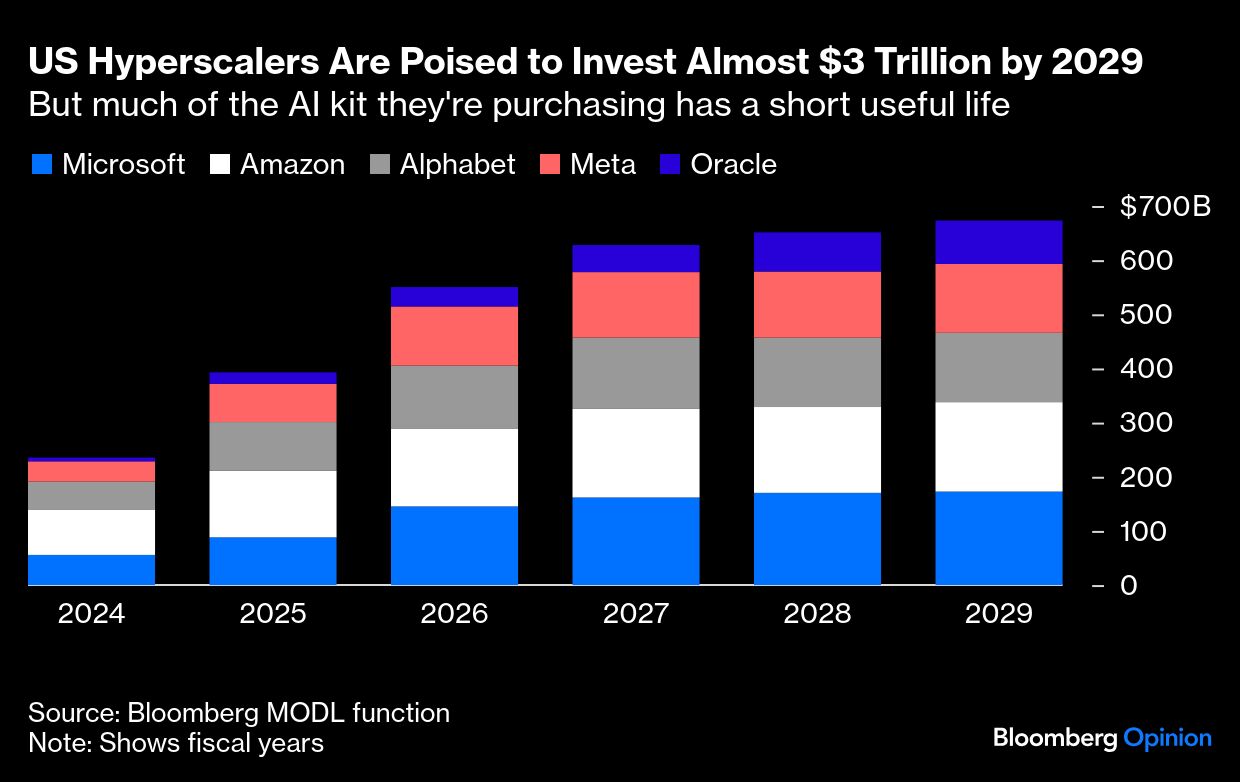

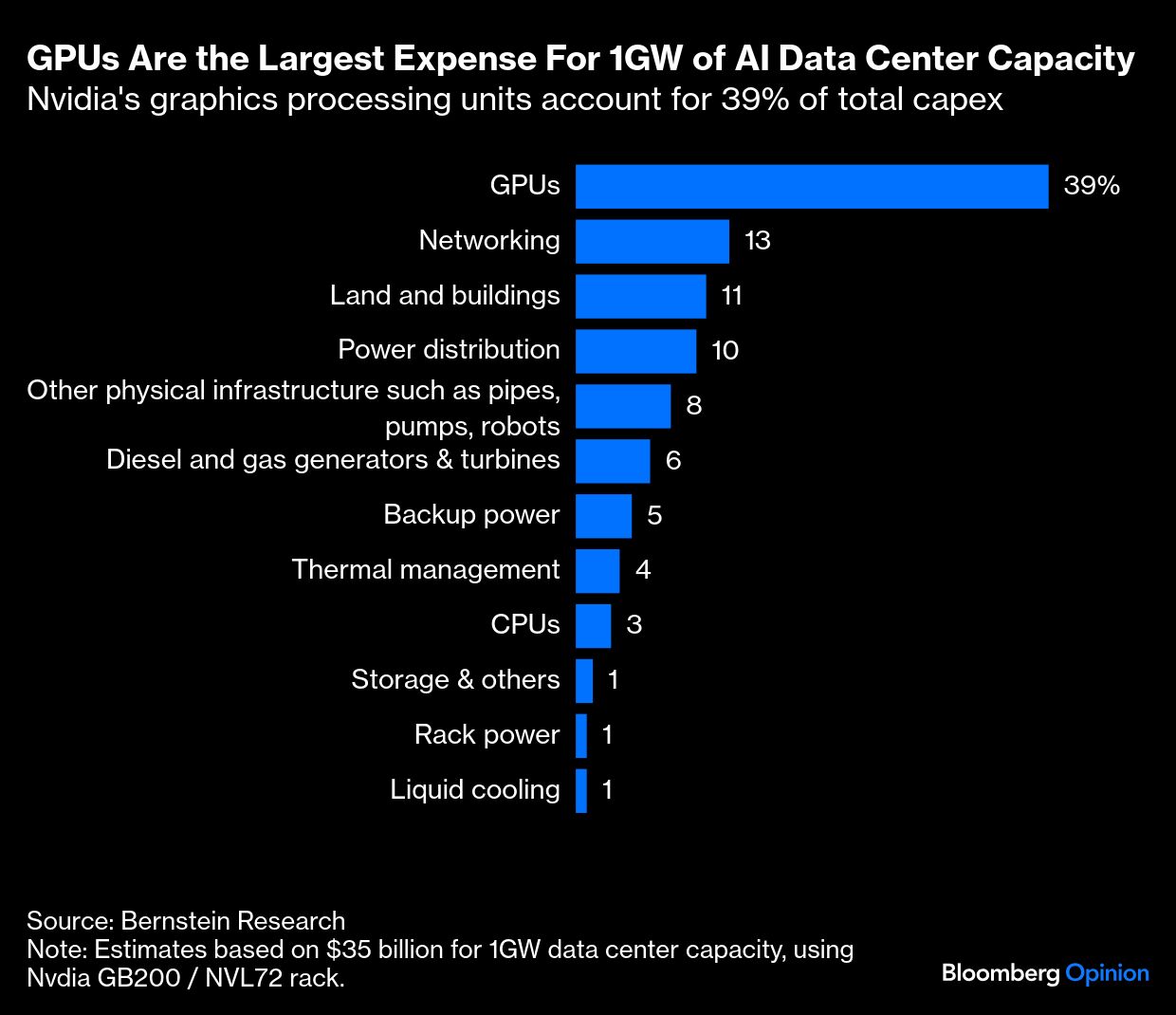

Costing tens of thousands of dollars each, Nvidia Corp.’s pioneering AI chips make up a hefty chunk of the $400 billion that Big Tech plans to invest this year — a bill expected to hit $3 trillion by 2029.

But unlike 19th-century railroads, or the Dotcom boom’s fiber-optic cables, the graphics-processing units (GPUs) fueling today’s AI mania are short-lived assets with a shelf life of perhaps five years.

As with your iPhone, this stuff tends to lose value and may need upgrading soon because Nvidia and its rivals aim to keep launching better models. Customers like OpenAI will have to deploy them to stay competitive.

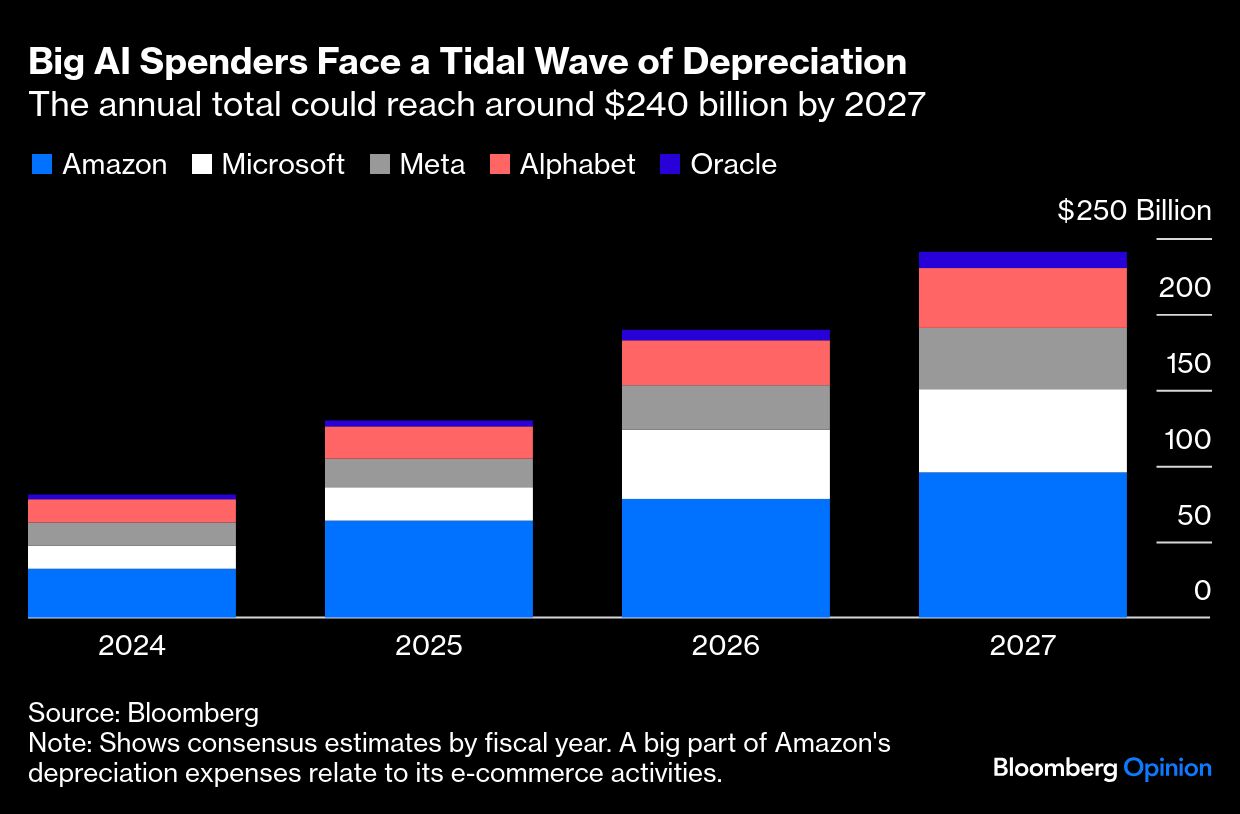

So while it’s comforting that the companies spending most wildly have mountains of cash to throw around (OpenAI aside), the brief useful life of the chips and the generous accounting assumptions underpinning all of this investment are less consoling. Michael Burry, who made his name betting against US housing and who’s recently turned to the AI boom, waded in this week, warning on X that hyperscalers — industry jargon for the giant companies building gargantuan data centers — are underestimating depreciation.

Far from being a one-off outlay, there’s a danger of AI capex becoming a huge recurring expense. That’s great for Nvidia and co., but not necessarily for hyperscalers such as Google and Microsoft Corp. Some face a depreciation tsunami that’s forcing them to be extra vigilant about controlling other costs. Amazon.com Inc. has plans to eliminate roughly 14,000 jobs.

And while Wall Street is used to financing fast-depreciating assets such as aircraft and autos, it’s worrying that private credit funds are increasingly using GPUs as collateral to finance loans. This includes lending to more speculative startups known as neoclouds, who offer GPUs for rent. Microsoft alone has signed more than $60 billion of neocloud deals.

Magnetar Capital, Blackstone Inc. and Macquarie Group Ltd. are among those providing such financing. Nvidia, meanwhile, is reportedly looking at using special-purpose vehicles to raise debt to buy and rent chips to customers such as OpenAI and Elon Musk’s xAI.

“The problem is we’re about to go from tens of billions of debt that’s funding quickly depreciating GPUs, to hundreds of billions of dollars. And then there could be serious trouble,” Gil Luria, head of technology research at DA Davidson, tells me.

Such worries may seem arcane when tech firms boast of colossal revenue and sizeable productivity gains from AI investments. But tech investors may have forgotten how much depreciation can hurt.

Starting from around 2020, hyperscalers began extending the depreciable life of servers to about six years from as little as three years, meaning the earnings hit from their heavy spending was more spread out. At the time this seemed justified because the pace of computing advances, known as Moore’s Law, appeared to be slowing. And tech companies found ways to keep their equipment running longer.

These changes have certainly helped profit. Meta Platforms Inc.’s January decision to adopt a 5.5 year useful life for most of its servers and network assets, up from four-to-five years previously, boosted its net income by close to $2 billion in the nine months to September.

Of course, GPUs don’t suddenly become useless when a new version arrives. Not everyone needs leading-edge kit to train frontier AI models. Processors can be repurposed for less demanding AI inference and other computing tasks, or they can be resold in emerging markets. And software innovations can extend their economic life. The head of Alphabet Inc.’s AI and infrastructure team, Amin Vahdat, has said that its seven- and eight-year-old custom chips, known as TPUs, have “100% utilization.”

“You won’t always need a Porsche 911 engine to run these workloads, a VW engine will do fine,” says Anurag Rana, senior technology analyst at Bloomberg Intelligence.

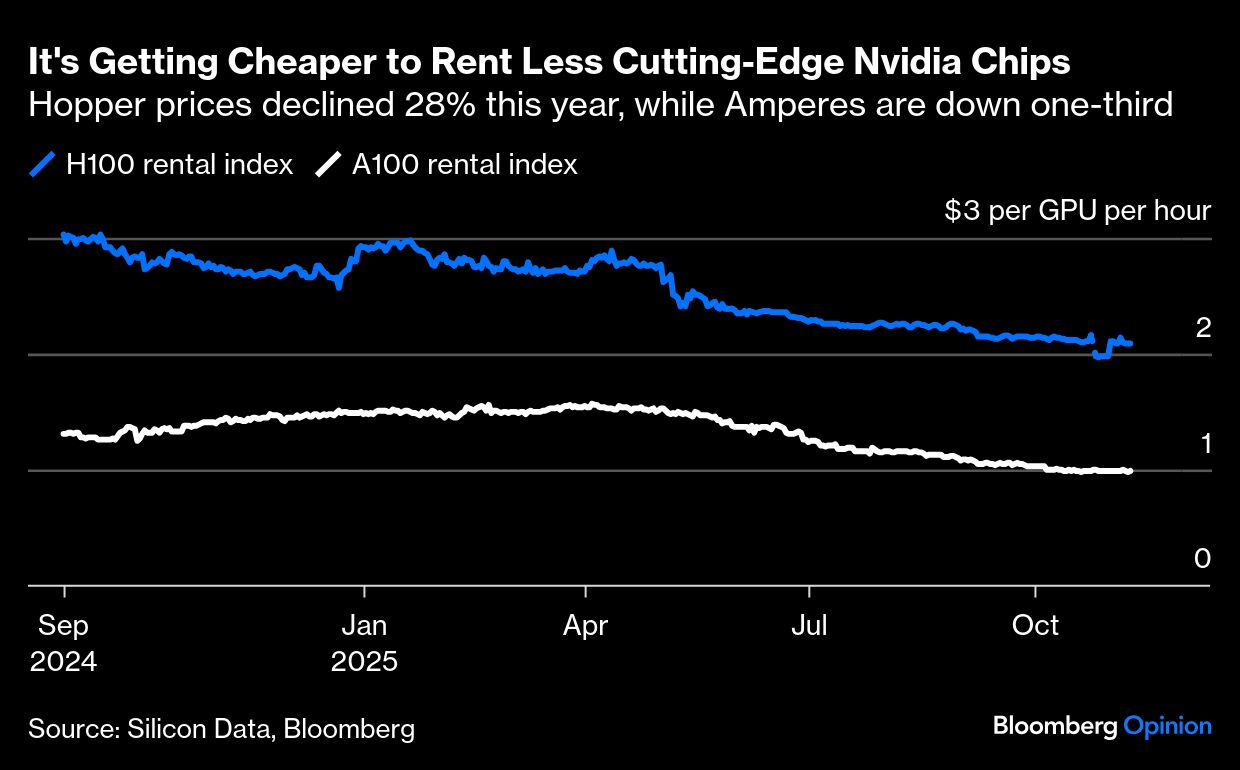

Nevertheless, the flattering accounting is questionable. Nvidia has moved to a yearly product cycle from its previous two-year approach. Chief Executive Officer Jensen Huang said in March that once next-generation Blackwell chips start shipping “you couldn’t give Hoppers away”, referring to the prior model.

Huang was joking. But as chip shortages have eased, rental rates for Nvidia A100 (Ampere) chips, launched in 2020, and the 2022 Hopper, have slumped.

As GPUs become an asset class, their residual value will depend on a “cocktail of unknowables,” warns short-seller Kerrisdale Capital. This includes future semiconductor architecture shifts, hyperscalers developing their own custom silicon, and trade politics such as the US export ban on advanced chips to China. I’d add that electricity constraints holding back data-center construction could make it less economic to operate older, less efficient chips.

It was striking, then, that early this year Amazon reverted to a more conservative five-year useful life estimate for a subset of servers and networking equipment (from six years). It saw “an increased pace of technology development,” particularly in AI and machine learning.

Unfortunately, there’s little agreement about the durability of such equipment.

CoreWeave Inc., a publicly traded neocloud with a roughly $50 billion market value, says it’s “incredibly comfortable” with its six-year GPU depreciation policy, pointing to its success in re-contracting processors after the initial rental term ends, which on average is after four years. However, Amsterdam-based rival Nebius Group NV uses a four-year depreciation schedule. Paris neocloud Scaleway thinks three years is more realistic.

If tech companies underestimate how rapidly processors lose value and technological relevance, they may have to book impairments. In the short term you’d expect to see reported profit much higher than cash flows, because the former doesn’t include all the upfront capital spending. But if this gap persists, it could be a sign that replacement costs are starting to bite and earnings are overstated.

The onus is now on the companies who own GPUs to quickly jack up their AI revenues. Otherwise they risk being swamped by higher depreciation costs and they may not be able to afford the next round of capex.

About half of Microsoft Corp’s near $35 billion of third-quarter capital expenditure was for short-lived items such as GPUs and CPUs. Reassuringly, its bookings of future AI sales match the expected depreciation. Plus it’s been careful not to buy too many of one generation of chips, and its AI kit is “fungible,” according to executives.

I reckon most hyperscalers should be able to hedge against overbuilding and obsolescence because they have so many businesses and customers hungry for computing power. If AI demand disappoints, they can cut back on capex and sweat existing assets.

But neoclouds lack Big Tech’s vast profits and cash piles, so they’re borrowing billions instead. CoreWeave has $16.9 billion of net debt including lease liabilities, according to data compiled by Bloomberg. It’s using the money to fund as much as $14 billion of capex this year and more than double that in 2026. That will take it beyond the usual spending of an oil major like Shell Plc.

Although CoreWeave has made progress in lowering borrowing costs, some initial loans have double-digit interest rates. Hence its interest expenses exceed operating income.

Such risks should be manageable if neoclouds can recoup spending via multi-year contracts with reliable renters of their services, rather than relying on spot markets or revenue from less tested startups. CoreWeave said this week that more than 60% of its $56 billion revenue backlog relates to “investment-grade” customers. It echoed Microsoft by saying its infrastructure is fungible.

Still, rose-tinted neocloud financial models may be undone if GPUs lose value quicker than expected. A lack of demand or AI breakthroughs that are less thirsty for computing power could create a need to offload chips en masse.

Nvidia’s soaring stock price is the simplest barometer for AI mania. But it’s the more opaque, more complicated world of debt finance and accounting depreciation that could yet puncture the AI bubble.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.