The growing list of US credit busts, from subprime auto lender Tricolor Holdings to Broadband Telecom Inc., raises a troubling question: If such “cockroaches” proliferate — if many more enterprises collapse under the weight of excessive debt — who will ultimately bear the losses?

If your retirement savings are entrusted to a US life insurer, there’s a growing risk it might be you. Regulators must get a better handle on the problem — and soon.

Life insurers manage trillions of dollars on behalf of individuals to whom they’ve promised regular income in old age. This financial service should not be complicated: Invest in high-quality assets that will pay off when customers eventually need their money. Low risk, stable returns.

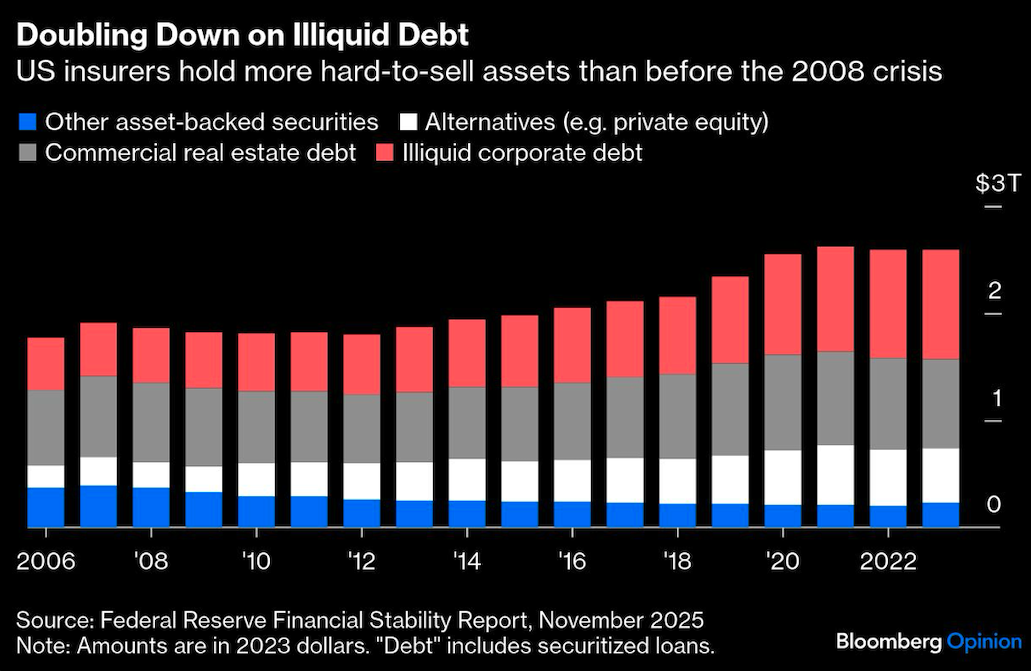

Lately, though, large investment firms have transformed the industry. Why, they reason, should insurers pay a premium for highly liquid bonds if they don’t need the money back anytime soon? Better to focus on harder-to-sell stuff with higher returns, such as real estate debt and loans to smaller companies. As of 2023, US life insurers’ illiquid investments amounted to more than $2.5 trillion, or about 37% of total assets — up from 31% a decade earlier and more than just before the 2008 financial crisis.

While boosting profits, the shift carries significant downsides. For one, the quality of illiquid assets can be hard to assess. Insurers often rely on confidential private ratings and invest through opaque chains of intermediaries — for example, via business development companies that in turn hold tranches of securities collateralized by loans to the actual operating businesses. Each link might employ added leverage to amplify returns, increasing the risk of defaults at a time when insurers’ own loss-absorbing equity capital is already near its thinnest in two decades.

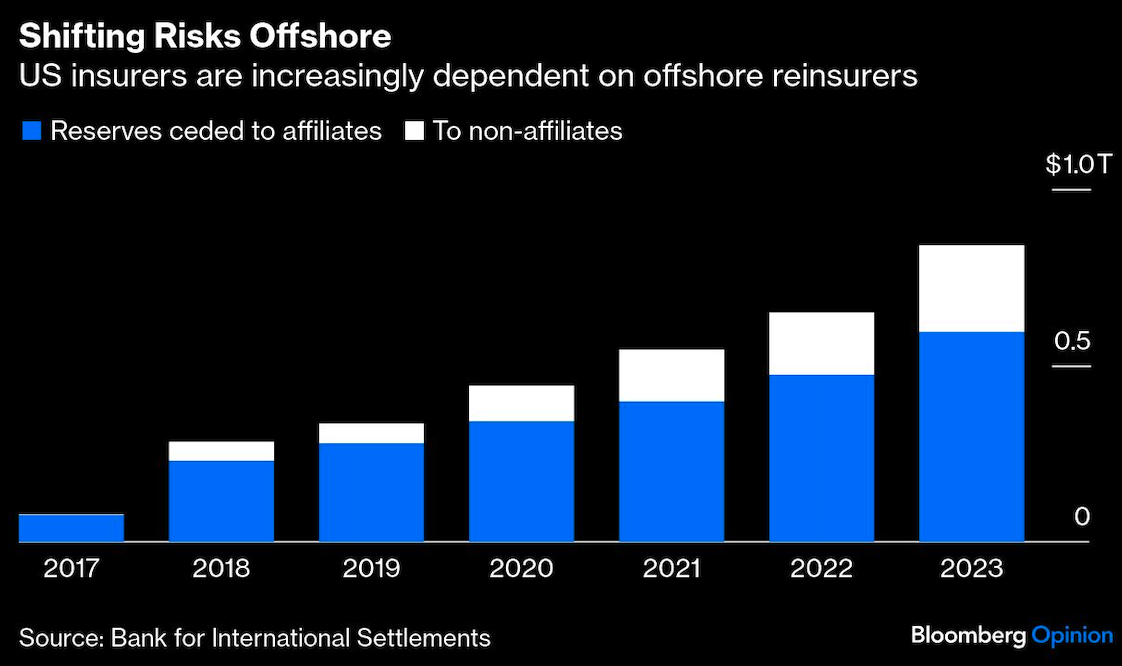

To complicate matters further, US insurers have moved large chunks of their obligations and related assets to reinsurers — often their own affiliates — in offshore jurisdictions with more advantageous tax and regulatory regimes. Life insurance assets in Bermuda, for instance, now exceed 150 times that country’s gross domestic product. This can hide risks from the state regulators who oversee US insurance companies — until something breaks, as when Bermuda-based reinsurer 777 Re recently failed, hitting several insurers in Utah and South Carolina.

Life insurers’ liabilities have also evolved, not for the better. Their funding is typically considered stable, because policyholders face penalties for withdrawing early. Yet surrenders can happen, particularly when higher interest rates make other options more attractive, as the 2023 run on Italian life insurer Eurovita SpA demonstrated.

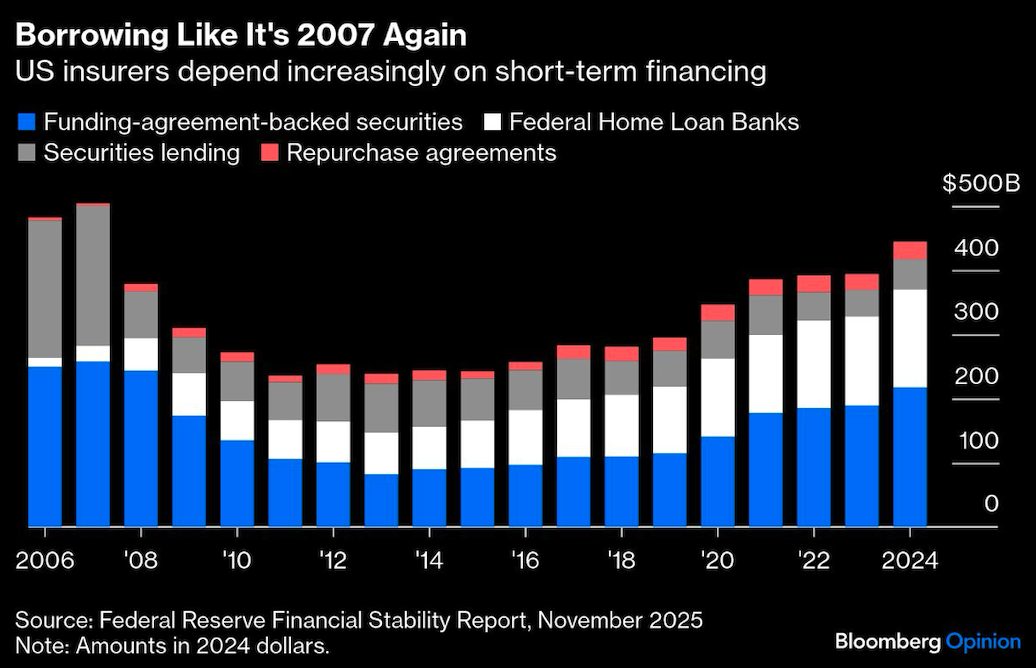

Worse, insurers are increasingly borrowing outright on short-term markets and implicitly via derivatives, raising the risk of sudden cash or collateral demands, akin to a bank run. As of 2024, short-term borrowing at US insurers exceeded $400 billion, up 82% in inflation-adjusted terms from a decade earlier.

All told, US life insurers are becoming a potential nexus of contagion. Suppose, for example, further credit blowups left them holding impaired, unsalable assets, raising concerns about their solvency. Their customers — many of whom became so involuntarily, when the insurers took over employer-provided pensions — wouldn’t be the only ones exposed. They’d have to pull back on lending, precipitating a credit crunch that would affect good businesses and bad. They might have to sell liquid bonds and stocks to meet surging cash demands, tanking markets more broadly. The government might be compelled to bail out the largest, most interconnected institutions at taxpayer expense, as happened with American International Group Inc. in 2008.

Authorities recognize the danger. Global regulators have developed a standard designed to better capture and compare the risks that the largest insurers present. Yet the US hasn’t adopted it, while measures by the National Association of Insurance Commissioners to improve disclosure and tighten capital requirements can achieve only so much when supervisory power is fragmented among 50 separate states.

The US must do better. Its Financial Stability Oversight Council, for example, should reassert its power to subject systemically important insurers to federal supervision — or at least push state regulators toward more consistent and complete scrutiny of insurers’ entire operations, including their vulnerability to runs and severe losses. Beyond that, adopting global capital standards or something equivalent, and nudging other nations to do the same, could enhance resilience and inhibit offshore regulatory arbitrage.

Whatever benefits the innovations in life insurance might offer, they shouldn’t be putting policyholders and everyone else at undue risk.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.