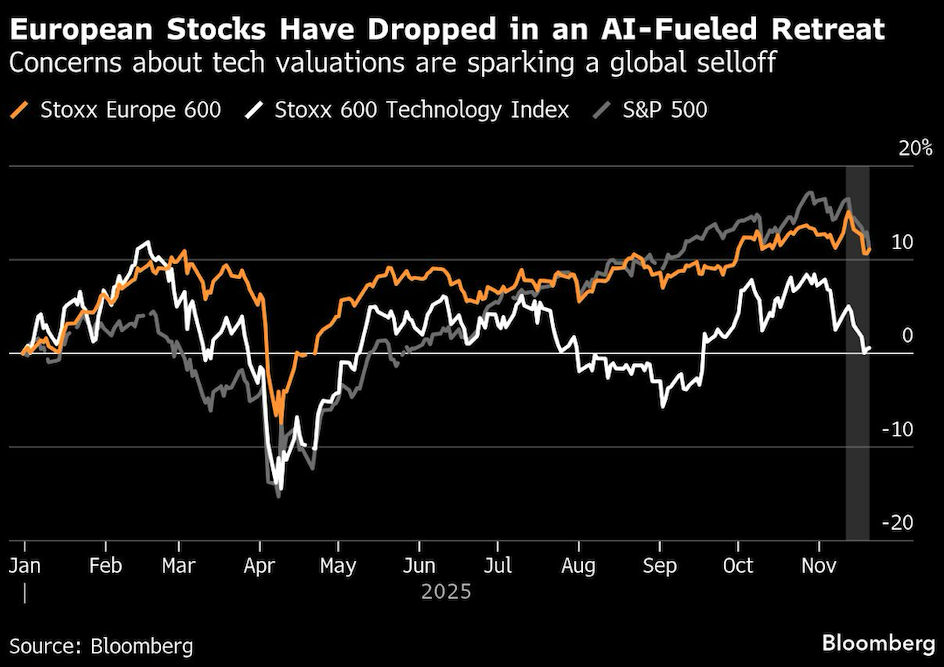

European stocks fell as a risk-off mood hit some of this year’s biggest winners on concerns about lofty technology valuations and an uncertain US monetary policy outlook.

The Stoxx Europe 600 Index dropped 0.4% at 2:53 p.m. in London. The index came off session lows after Federal Reserve Bank of New York President John Williams said he sees room for the US central bank to cut interest rates again in the near term.

Energy and technology stocks tumbled the most, while defensive sectors including food and beverage as well as personal care outperformed. Autos were also among the biggest gainers. The defensive Swiss Market Index also rose 0.5%, benefitting from demand for assets that are perceived to be safer.

Siemens Energy AG dropped 6.7% even after the company announced its largest share buyback, as investors booked profits in some of this year’s strongest winners. ASML Holding NA, the biggest gainer on the index by points this year, fell 5.7%.

The Stoxx 600 is tracking its deepest weekly decline since August, as the mood turns cautious into the year end. Investors are awaiting further evidence that hefty spending on artificial intelligence is paying off, while there are growing doubts about the Fed’s next rate cut.

Investors are also monitoring negotiations to end the war in Ukraine. Kyiv’s key European allies lined up with President Volodymyr Zelenskiy to reject key elements of the plan on Friday.

“I’m wondering how much of it is really healthy de-risking rather than, ‘we’re in an AI bubble and it’s going to implode,’” said Sophie Huynh, a portfolio manager at BNP Paribas Asset Management. “Heading into year-end, you’re wondering how much new economic data you’re going to receive. After a spectacular year, do you really want to risk your year-end performance? So you take chips off the table.”

On Thursday, the S&P 500 logged its sharpest intraday reversal since the height of the tariff turmoil in April following a mixed jobs report. Still, the benchmark was up 0.5% in early trading on Friday, suggesting appetite for dip-buying.

Other market participants also said the pullback was expected after a strong rally in both European and US stocks this year. Last week, the Stoxx 600 was approaching overbought levels — a precursor for potential declines. The benchmark is now about 4.5% below an all-time peak.

“This is a healthy correction which could continue into the beginning of next week as many systematic funds have to de-risk,” said Ulrich Urbahn, head of multi-asset strategy and research at Berenberg. “However, we also believe that markets will rebound into year-end.”

For Guillermo Hernandez Sampere, head of trading at asset manager MPPM, the market reaction showed that skepticism about the US labor market stems from insufficient data after a government shutdown delayed publication.

“The expectation of a swift response from the Federal Reserve could further fuel volatility,” he said.

Meanwhile, latest data added to confidence in the health of the regional economy as private-sector activity in the euro area stayed strong in November. However, in the UK, businesses recorded hardly any growth in the weeks ahead of the Labour government’s upcoming budget.

Ubisoft Entertainment SA advanced 8.4%, reversing initial declines, as news that the company was found by auditors to be in breach of a loan agreement was outweighed by better-than-expected net bookings.

You want more news on this market? Click here for a curated First Word channel of actionable news from Bloomberg and select sources. It can be customized to your preferences by clicking into Actions on the toolbar or hitting the HELP key for assistance. To subscribe to a daily list of European analyst rating changes, click here.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.