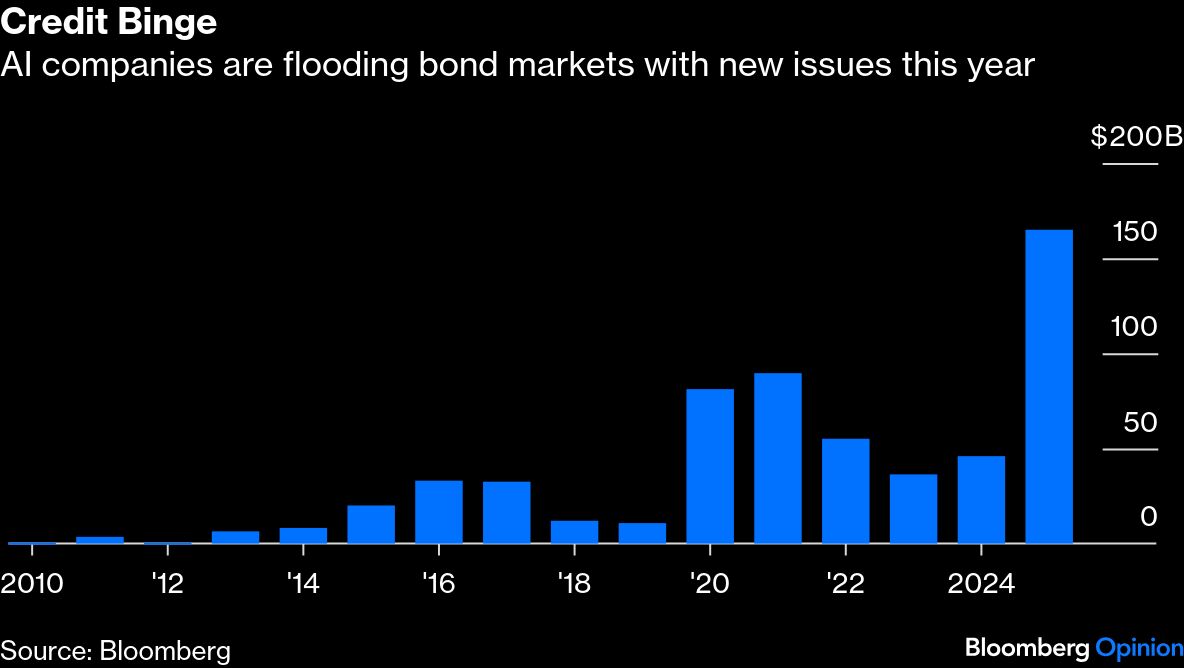

With corporate bond spreads widening and Oracle Corp.’s credit default swap spiking to a multi-year high, Wall Street is getting worried that a flood of debt sales from Big Tech is overwhelming buyers and could blow up credit markets. Globally, firms up and down the AI supply chain have done $165 billion worth of bond deals this year — 40% of which were raised this month.

Two questions are on people’s mind. First, do credit markets have room to host these modern-day cowboys? Second, will those competing to win the AI race heed investors’ advice on the appropriate pace and magnitude of new debt issues? Going forward, tech companies will certainly do more business with Wall Street, because they won’t be able to generate enough profit to pay for their AI ambitions. By 2028, they will have to seek as much as $1.5 trillion external financing, according to Morgan Stanley.

The latest monthly fund managers’ survey from Bank of America Corp. offers a glimpse of the investment community’s thinking. For the first time in two decades, asset managers say companies are over-investing, even though more than half concede that artificial intelligence is already increasing economic productivity, and most are not worried about the corporate sector’s financial health. When asked what firms should do with their cash, the opinions are about equally divided among improving balance sheets, returning it to shareholders, and increasing capital spending.

In other words, professionals are telling tech firms to continue spending billions of dollars on AI infrastructure, but at a more measured pace.

After all, the bond market has a proven history of absorbing deluges of new debt. JPMorgan Chase & Co. looked at three episodes in the investment-grade space, namely the shale gas boom in 2014 and 2015, the telecom M&A wave in 2017, and in recent years, debt-financed acquisitions in the healthcare sector. The bank concluded that only the energy example ended badly. After oil prices cratered in 2015, there were many fallen angels, companies whose debt was downgraded to junk, thus causing a spike in credit spreads.

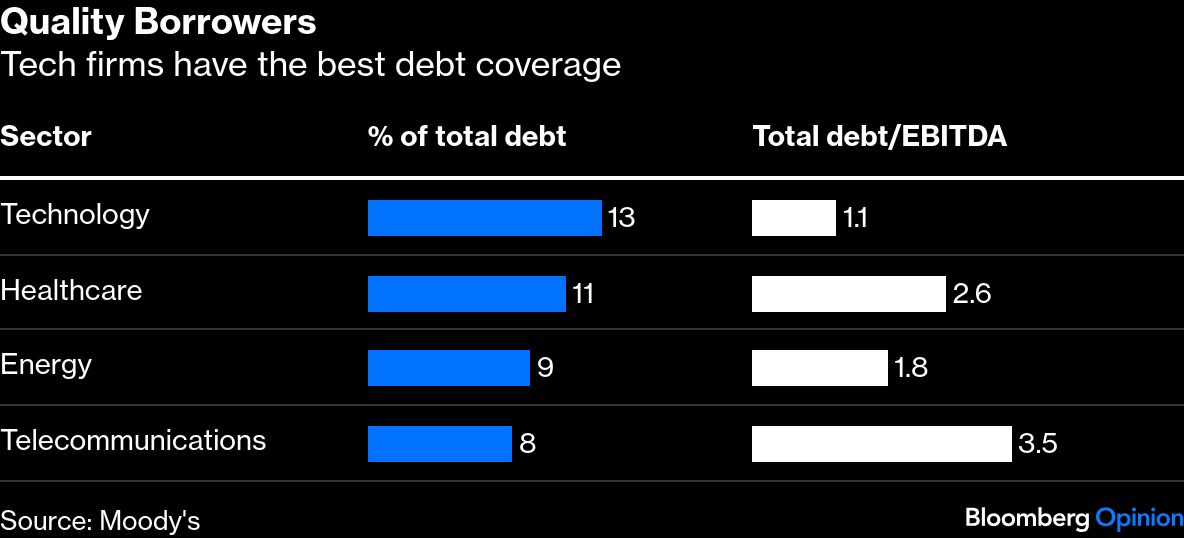

In addition, while the tech sector holds the top spot for total debt outstanding, it has the lion’s share of cash and remains the least leveraged. So when companies do issue bonds, they improve the credit outlook of the entire pool. Amazon.com Inc., for instance, had not come to market in nearly three years before this month’s $15 billion sale.

The second question is trickier to answer. Credit markets’ usual mechanism is still working, in that bond investors have been quick to demand tech firms cough up before placing their orders. In theory, higher borrowing costs should serve as natural deterrents to slow down companies’ credit binge.