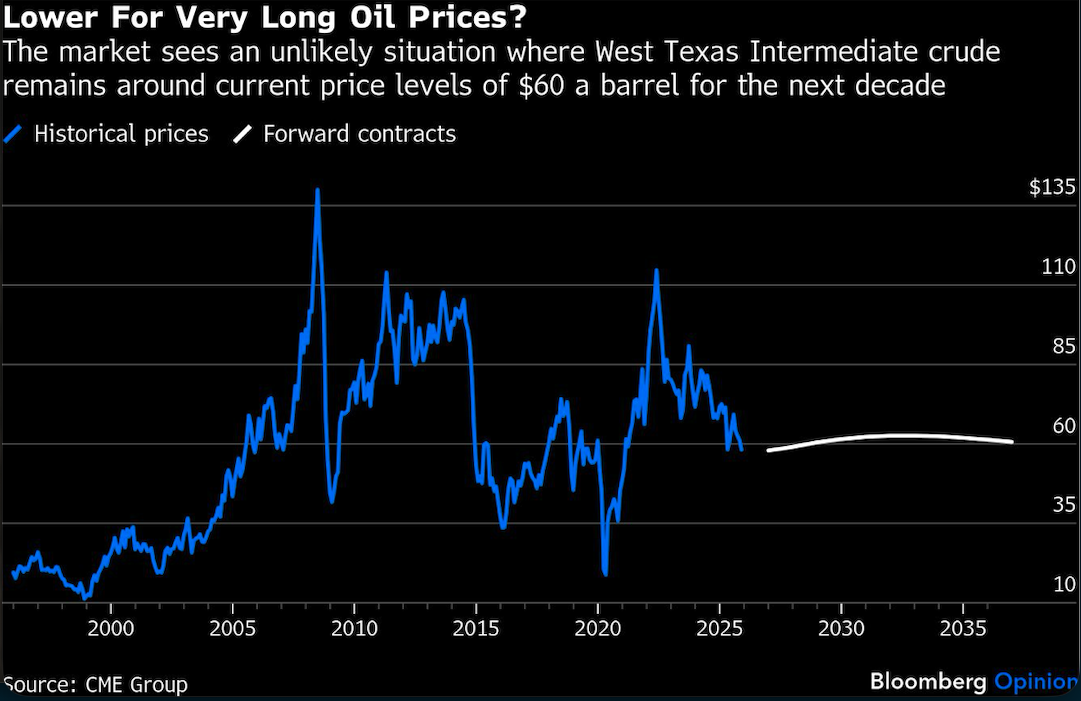

Let’s be honest: The oil market has always been wrong about long-term prices. Unsurprisingly, it’s currently wrong in anticipating that a barrel of crude will cost around $60 by 2030, close to current levels. Barring an economic cataclysm, oil will be more expensive five years from now.

Before the bulls celebrate, however, let me reaffirm that I remain short-term bearish, particularly for the first half of 2026. Little has changed since late 2024, when I warned the price level that mattered wasn’t $100-a-barrel anymore, but rather $50. Unless OPEC+ cuts production significantly, and quite soon, oil prices will weaken further in the next few months, probably overshooting to the downside. I’m not convinced that we won’t see prices starting with a 4 before the dollar sign, even if briefly, early next year.

But it increasingly feels like the energy market is way too sanguine about oil prices staying low. Look at the oil price curve, and it’s $50 to $60 a barrel from here to eternity. I’m not convinced. Neither is the equity market, where companies that depend on crude cash flows over the longer term — Exxon Mobil Corp. and Chevron Corp. spring to mind — are faring well.

For simplicity, let’s use the five-year forward contract as proxy for long-term oil prices. Admittedly, that contract, currently changing hands at just under $62 for a barrel of West Texas Intermediate crude, isn’t a forecast, but rather the level that buyers and sellers are today – today – willing to trade at for delivery in 2030.

Historically, the contract has been a poor predictor of future prices. But, as I said, that’s a feature, not a bug. In 2003, it said that oil would average $25 a barrel by 2008. The reality? Almost $150 a barrel. In 2020, during the pandemic, it said that five years later it would average $35 a barrel; the reality is closer to $60 a barrel.

Now, it says that by December 2030 the price of oil won’t stray from current levels of around $60. That doesn’t feel right: it would be too low to balance supply and demand then. What I’m less certain about is whether significantly higher prices are needed earlier, say in 2027, to balance the market.

Let’s start with demand. Despite constant nonsensical talk about the world shifting away from fossil fuels, oil consumption growth remains healthy. In both 2025 and 2026, demand is likely to increase at an annual rate of 800,000 to 900,000 barrels a day, not far from the 20-year average of about 1.1 million barrels a day. Barring a global recession, demand is likely to expand at a similar rate in 2027 and toward 2030, requiring quite a lot of new production. Current prices, cheap on a historical basis both in nominal and real terms, would do nothing but increase that appetite.

What about supply? That’s the problem. Today, the oil market is oversupplied due to a combination of unusual factors. First, several giant oil projects long in the making have come on stream almost simultaneously in 2025 after their construction was delayed during the Covid-19 pandemic. Second, 2022’s high prices, when WTI surged briefly above $120 a barrel as Russia invaded Ukraine, turbocharged the US shale industry. Third, Saudi Arabia pushed the OPEC+ cartel into a series of production hikes despite a growing glut, in part after several members, notably Kazakhstan, the United Arab Emirates and Iraq, cheated on their output quotas.

The supply tide will remain high in 2026 and even early 2027, but will recede quickly. By 2028, annual supply growth is likely to be trailing annual demand growth, requiring more OPEC+ crude. When that happens, oil prices would move higher to encourage increased investment.

Put all together, and a bet that oil will trade higher by 2030 — say above $75-$80 a barrel — has a decent chance of coming good, significantly higher than where the five-year forward contract currently trades. What about $100 a barrel? Highly unlikely, in my view: The oil market doesn’t face the same pressure as it did during the 2003-2008 rally when supply growth suddenly had to catch up with the runway train that was Chinese demand growth.

What could keep oil prices lower for longer? Above all, politics. Petroleum is abundant, but some resources remain beyond reach due to sanctions. Remove those limitations and supply will improve, not just in the short term but in the long run. The two countries to watch are Russia and Venezuela. Both are pumping below their historical capabilities. And both could be re-integrated into the global economy.

Even so, oil appears too cheap to balance the market in the long term. The balance of risk points to higher oil prices by 2030 — even if the journey has a bearish pause in 2026.

A message from Advisor Perspectives and VettaFi: Are you backed by institutional quality bond funds? Click here to learn more.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Javier Blas