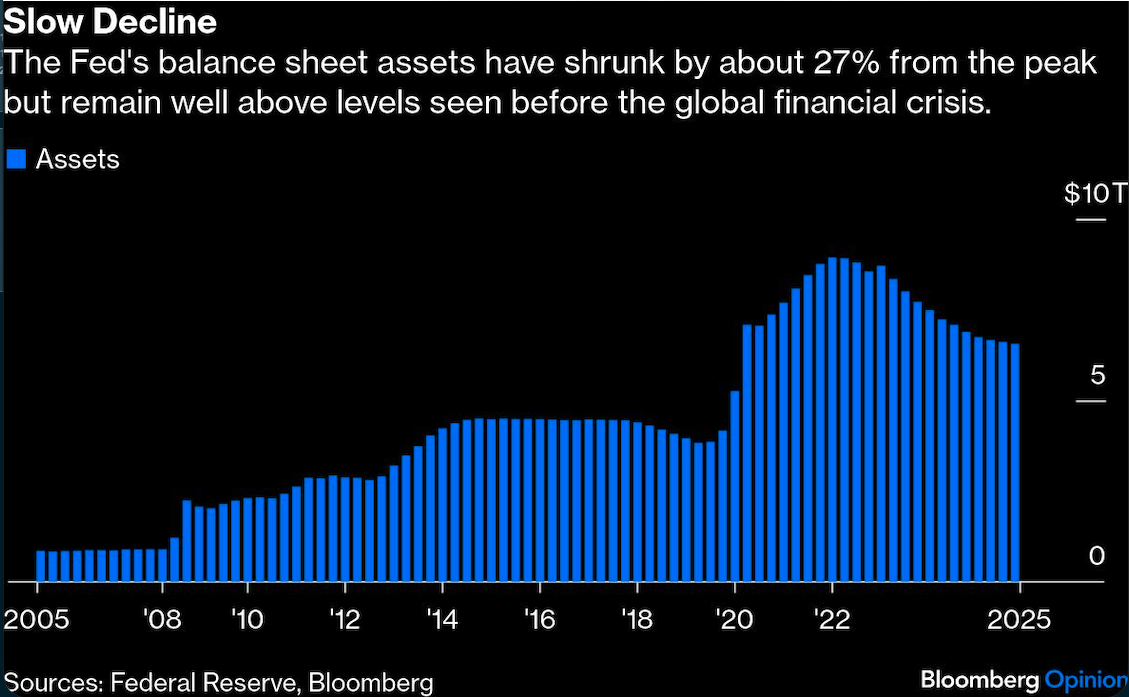

The Federal Reserve's balance sheet has shrunk from a peak of $8.97 trillion in April 2022 to $6.56 trillion as the central bank has unwound much of the Treasury and agency mortgage-backed security purchases undertaken to support the economy through the global pandemic. This has bought the demand and supply of reserves into much closer balance.

Some advocate shrinking the balance sheet further, for reasons ranging from reducing the Fed’s footprint in financial markets to allowing greater volatility in money market rates in order to better monitor incipient stresses in financial markets and enabling more rate cuts. These advocates miss two important points. First, reducing the balance sheet further would not be an easy task operationally. It would require a dramatic change in how the Fed conducts monetary policy. Second, because a smaller balance sheet would not exert much restraint, it would not open the door for much lower short-term rates.

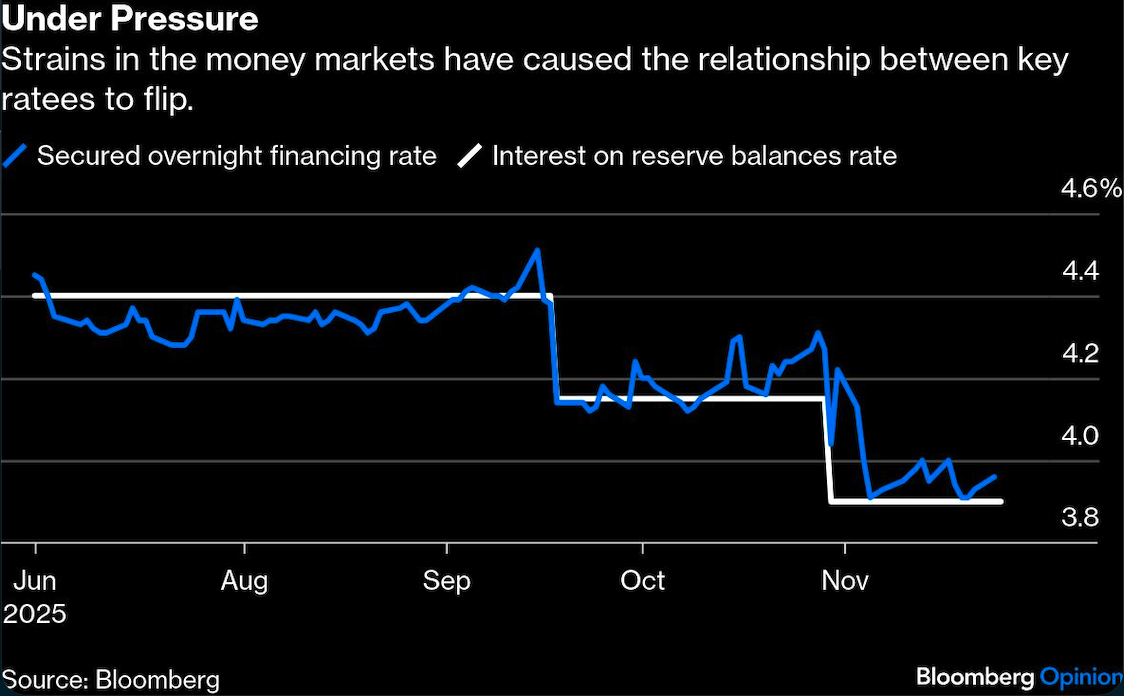

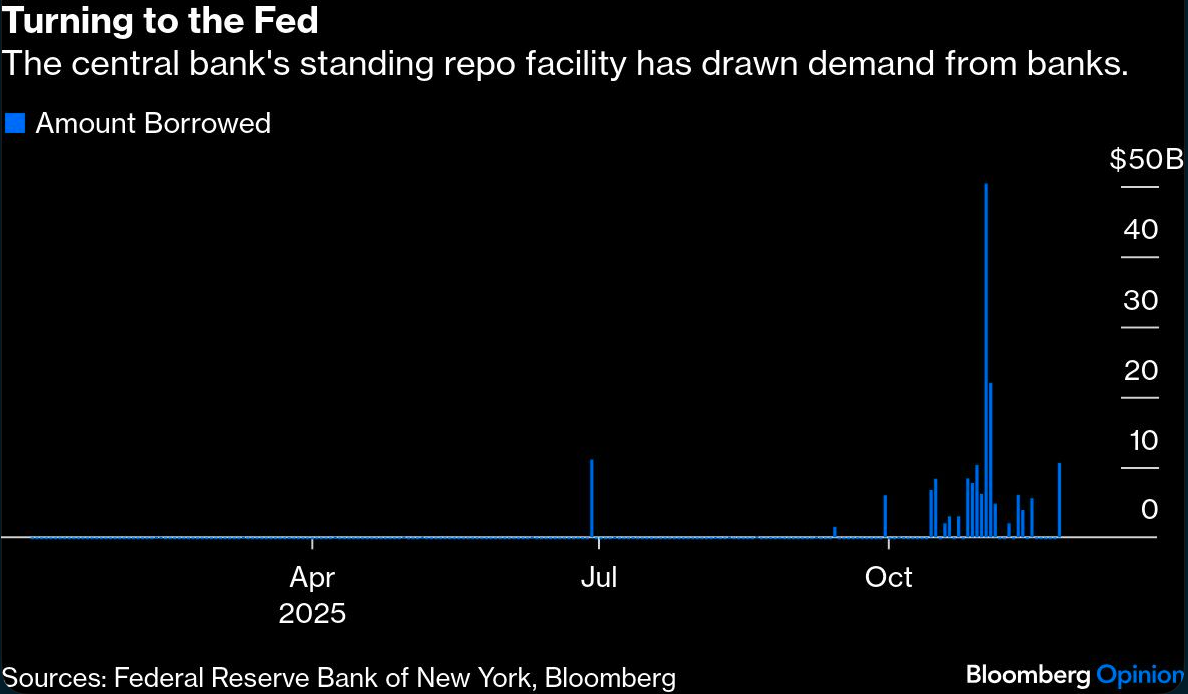

The amount of reserves on the Fed’s balance sheet has shrunken sufficiently to reduce the level from “abundant” — where supply always exceeds banks’ demand — to “ample”—where demand can occasionally exceed supply, causing money market rates to rise. As reserve conditions have tightened over the past two months, the federal funds rate has moved five basis points higher within its 25-basis-point target range. And repo rates have often risen above the rate available from the Fed’sstanding repo facility (SRF), encouraging banks to borrow from it.

With its journey from abundant to ample complete, the central bank will cease shrinking its balance sheet, ending its quantitative tightening program Dec. 1. Soon thereafter the Fed will begin to buy US Treasuries to ensure that the supply of reserves remains “ample” rather than “scarce.” The purchases will offset the drain in reserves caused by the growth in the demand for dollars and to accommodate the rise in demand for reserves by banks as the economy grows.

The amount of currency outstanding has increased about 3% over the past year, and if that trend were to continue, it would require about $70 billion in Treasury purchases in 2026. If bank demand were to rise at a rate equal to nominal growth in gross domestic product — perhaps 4% - about $115 billion of purchases would be required.

Together, the Fed’s total Treasury purchases to ensure reserves are ample would be less than $200 billion per year — a pittance relative to a $2 trillion annual budget deficit and outstanding Treasury debt held by the public of more than $30 trillion. In addition, the Fed would continue to roll over about $200 billion of mortgage-backed securities pre-payments into Treasury bills.

To shrink the balance sheet significantly further, the Fed would have to reduce the demand for reserves by banks. To do this, the Fed would need to make those reserves less attractive relative to other money market instruments. In the current regime, this is not straight-forward. When reserves shrink, repo rates rise and banks tap the SRF, which pushes the supply of reserves back up — negating any shrinkage in the Fed’s balance sheet.

To push banks out of reserves, the Fed would either have to raise the rate on the SRF or eliminate it altogether. As reserves shrink, money market rates, including Treasury bill rates, would rise. And once these rates climb sufficiently, banks would be induced to hold higher yielding Treasury bills and other money market instruments rather than reserves. In the end, banks would hold less reserves and more Treasury bills and other money market instruments and the Fed would hold fewer Treasury securities.

One could surely engineer this outcome, but the transition would be difficult and the benefits modest, which is why Chair Jerome Powell endorsed the current ample reserves regime in a speech last month. Banks would hold assets with less favorable attributes relative to reserves in terms of liquidity, ease of settlement, and maturity. Money market rates would be more volatile and, with reserves scarce, banks would trade reserves among themselves, thereby increasing bank counterparty risk.

The only meaningful benefit would be that banks would no longer get a preferential rate on reserves relative to the rate available on Treasury bills and repos, and the Fed would no longer hold Treasury bills at rates slightly below the rate it paid on its reserves. This subsidy currently is quite modest, with interest rate paid on reserves at 4% and the four-week Treasury bill rate at 3.95%. Yet this overstates the size of the subsidy because the current four-week bill yield incorporates about a 80% probability that the Fed will cut rates by 25 basis points when the Federal Open Market Committee announces its monetary policy decision on Dec. 10. Pushing banks out of reserves into Treasury bills would save the Fed and, by extension the US government, only about four to five basis points in my estimation.

After all these gymnastics, the smaller Fed balance sheet would exert little monetary policy restraint. That’s because the stance of monetary policy would still be determined by the level of short-term rates not the size of the Fed’s balance sheet. In other words, the shrinkage of the Fed’s balance sheet would not enable much lower short-term rates.

A message from Advisor Perspectives and VettaFi: Are you backed by institutional quality bond funds? Click here to learn more.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.