The UK and Japan are responding to investor demand to boost short-term borrowing, a shift in strategy that offers governments lower interest payments but exposes them to potentially costly rates swings at the time of debt rollovers.

Britain has slashed sales of long-dated bonds — traditionally a bedrock of its debt issuance — to record lows this year, and is now mulling expanding its market for ultra-short dated bills. Japan is heeding calls to up its issuance of short-term debt after a rout in its long bonds.

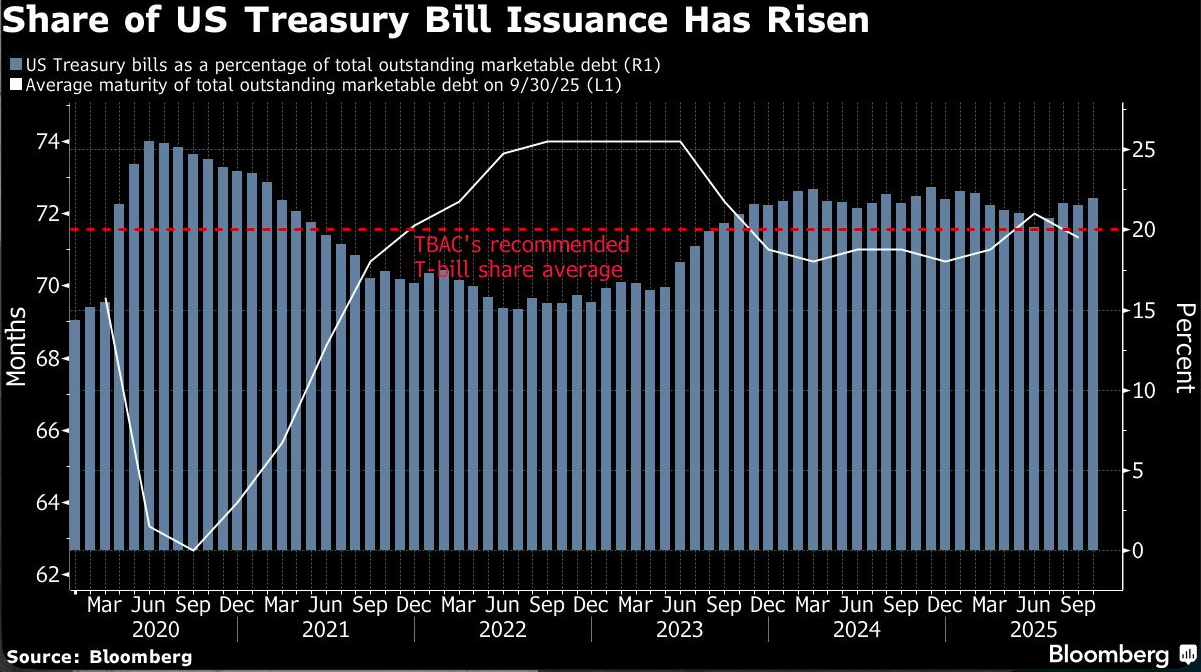

They’re not alone. The US is relying more on bills to fund its federal deficit, and countries such as Australia have floated similar policies. Globally, the average maturity of government bonds has fallen to the lowest since 2014, according to a Bloomberg Aggregate index. Yet it’s in Japan and the UK where long bonds have faced the steepest drop in demand, prompting the most radical policy overhauls.

In both countries, central banks that spent years buying up bonds to boost the economy are withdrawing their support, reducing demand for longer-term debt and hiking government borrowing costs. With debt levels already high, policymakers are turning to shorter-term notes that come with lower yields but need to be rolled over more frequently — possibly into the teeth of higher interest rates.

“The risk is if rates move higher and your interest bill suddenly increases a lot,” said Evelyne Gomez-Liechti, a strategist at Mizuho International Plc. in London.

The new strategies reflect a sea-change. For years, rich countries could borrow at near-zero — sometimes even sub-zero — rates. That allowed savvy finance ministries to lock in ultra-cheap financing costs, with the most ambitious issuing bonds that won’t mature until the next century.

Now, however, rates are higher and analysts don’t see a return to the days of almost free money. One market indicator that projects where benchmark yields will trade a decade from now has risen to 4.2% in Japan from 0.5% in 2020. The comparable rate for UK bonds has jumped to 6% from 1% five years ago.

The increases reflect inflationary pressures as well as waning demand for long-dated debt from traditional buyers. For decades, British defined-benefit pension funds bought long-dated bonds to match against their liabilities, allowing the UK to extend the average maturity of its issuance well beyond peers. Many of those programs are now winding down.

A similar story is playing out in Japan, where there’s less demand among banks and life insurers for super-long bonds, according to Takahiro Otsuka, senior fixed income strategist at Mitsubishi UFJ Morgan Stanley Securities Co. Investors are also worried about the supply of bonds as Prime Minister Sanae Takaichi prepares a stimulus package that is expected to be financed by a supplementary budget.

The market shifts are pushing yields on longer and shorter-term bonds further apart. The UK 30-year yield hit the highest since 1998 this year, while its premium over two-year notes rose to the most since 2017. In Japan, the gap widened to the most since at least 2006 this year.

That’s making short-term borrowing much more attractive to governments. Gilts with maturities of fewer than seven years are expected to make up 44% of new issuance in the current UK fiscal year, a nearly 20 percentage point increase compared to 2015-16. In Japan, around 60% of new issuance would come from bonds maturing in five years or less this fiscal year, compared to 56% in fiscal 2015.

However, an aggressive shortening of maturities is effectively a bet by the government that long-term bond yields are too high and will soon fall. The risk is they don’t, and costs skyrocket when debts need to be rolled over.

“If the maturity is just two years, that means refinancing will have to be done very frequently,” said Hiroshi Namioka, chief strategist at T&D Asset Management. “Continuously rolling over short-term loans raises questions about fiscal sustainability, and it’s important to be mindful of how that could make it harder to predict the future fiscal outlook.”

Still, analysts frame the changes as a natural response to evolving investor demand. Treasury Secretary Scott Bessent said last month that his department is “closely monitoring for potential long-term shifts in demand for particular US Treasury securities,” and will change in response. Bessent had said earlier this year it wouldn’t make sense given the level of long-term yields.

As a result, the share of shorter-term bills as a percentage of overall outstanding Treasury debt was about 22% as of the end of October, and could climb to 26% by the end of 2027, according to Citigroup Inc.

Unlike some other markets, however, the US has existing demand for such assets given that there’s more than $8 trillion parked in money-market funds, and strategists have surmised that the broader adoption of stablecoins could create billions of dollars of demand for T-bills.

This allows “Treasury to lean more heavily on bill issuance, taking some pressure off longer-dated yields as they can delay coupon auction size increases until late-2026,” said Gennadiy Goldberg, head of US interest rate strategy at TD Securities.

Meanwhile, the maturity of a gilt index has fallen from 17 years in 2021 to 12 years, while a Japanese benchmark has fallen from around 10.8 years to 9.6. The global government bond benchmark’s average maturity is below nine years.

For now, governments can rely on something of a trump card: key central banks are still in easing mode.

“The BOE and Fed still have room to cut. The BOJ could be seen as the higher risk, but I feel the hiking cycle goes at a different speed in Japan,” said Mizuho’s Gomez-Liechti.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Greg Ritchie, Momoka Yokoyama