The bad news just seemed to keep piling up for Pacific Investment Management Co.

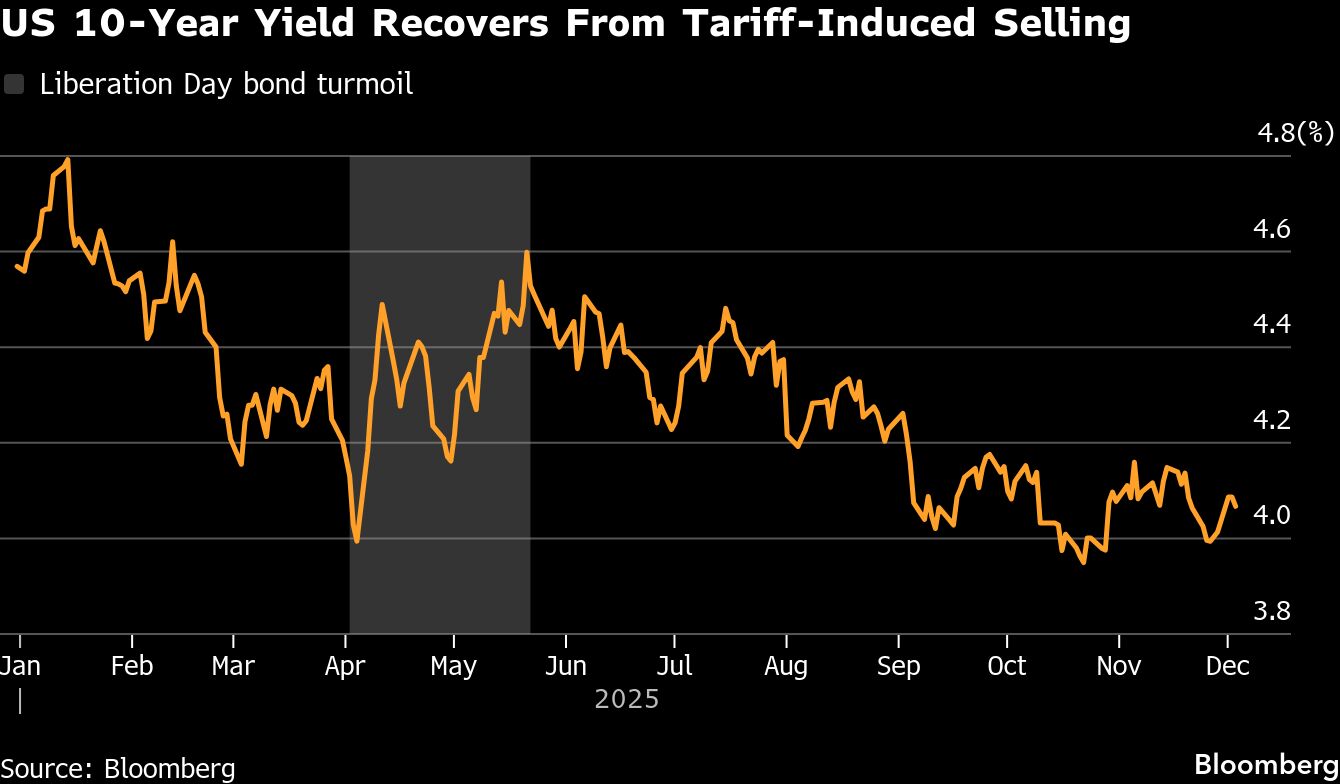

Across April and May, the bond giant’s positions in 5- to 10-year Treasuries and mortgages were getting hammered. First, after President Donald Trump’s punitive “Liberation Day” tariffs, and then amid the burst of “Sell America” calls that followed.

Pimco’s 14-member investment committee, entrusted with $2.2 trillion in customer assets, hunkered down in the firm’s headquarters in Newport Beach, California, and in London to assess the damage. For weeks, including Sundays, the brain trust, led by Group Chief Investment Officer Daniel Ivascyn, spent long hours gathering intel, checking in with clients and debating their response as yields shot higher.

After a run of less-than-sparkling returns, it was something of a make-or-break moment. In the end, Pimco not only held onto its stakes in Treasuries, but it bought more as they sold off, and mortgages as well. And in doing so, the firm catapulted itself to the forefront of US fixed-income fund managers this year.

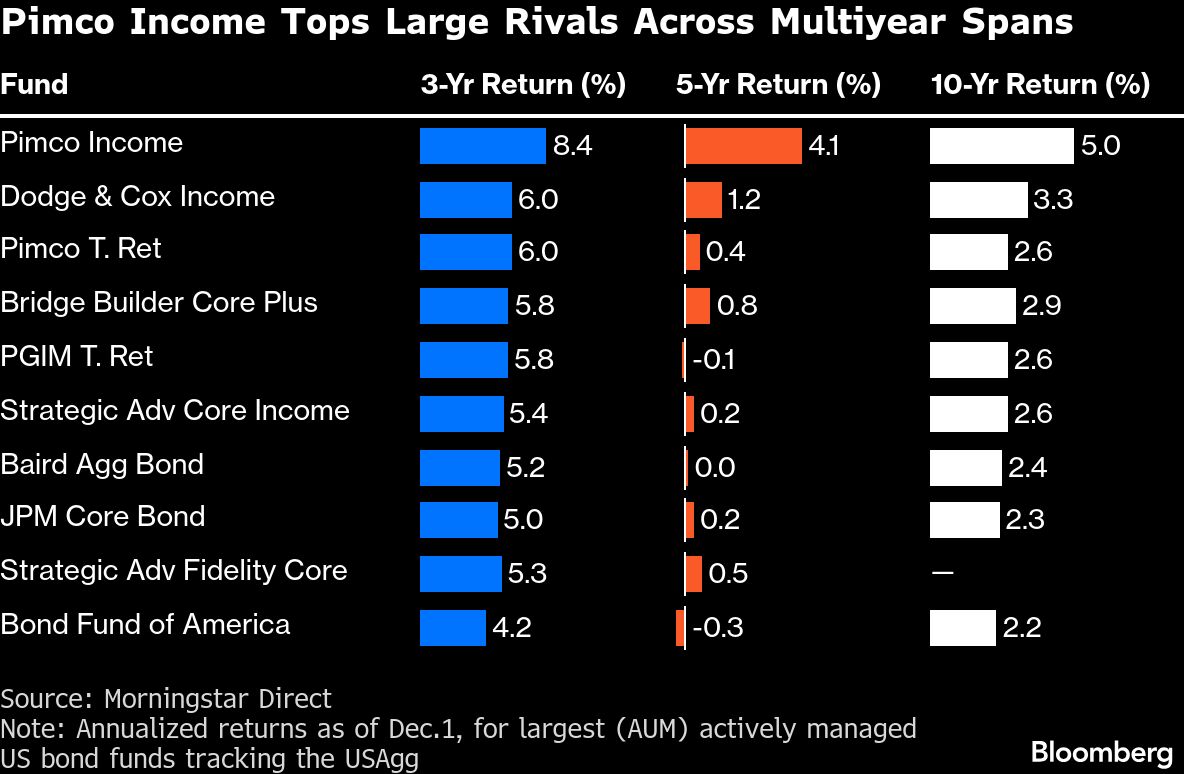

In the best year for US debt since 2020, the $213 billion Pimco Income Fund — the largest actively managed bond fund — has returned 10.4%. That’s better than all its biggest competitors benchmarked to the Bloomberg USAgg Index, and is its strongest return in at least a decade. The $47 billion Pimco Total Return Fund is a close second, gaining 9.1%. The Income Fund is among the top 3% this year of the roughly 300 funds in its category, after failing to make the top 10% since 2017, Morningstar Direct data show.

A key juncture, Pimco’s senior managers said, came after Trump rolled out his sweeping levies on Wednesday, April 2, triggering one of the most turbulent stretches for US Treasuries in the past few years.

That week, it just so happened, Ivascyn and other senior portfolio managers were meeting with clients in London, giving them an immediate read on how international investors were reacting. They huddled regularly there and held conference calls across time zones with colleagues around the world. By the weekend, the group decided to maintain their bullish stance on 5- to 10-year Treasuries, which they’d held since January in anticipation of some degree of economic headwinds from the tariffs Trump was pledging.

“The answer was pretty clear that this growth impact will be negative because it meaningfully increases the uncertainty both for the consumer as well as corporates,” said Mohit Mittal, CIO of core strategies, who joined the early April discussions from Newport Beach.

Things didn’t necessarily go their way straight off. The following week, yields surged, partly on worries that the trade war would spur foreign buyers, a critical source of demand for America’s bonds, to shun the nation’s debt.

Yields didn’t peak until May 22, as the benchmark 10-year Treasury yield eclipsed a multimonth high of 4.6% days after Moody’s Ratings stripped the US of its top credit grade, adding to concern around the nation’s obligations.

It was a rocky time for all markets, including bonds. Investors pulled a net $2 billion from the Pimco Income fund in April, the first outflow since October 2023, according to Morningstar Direct. Then in May the broad US bond market fell 0.7%, its worst month this year, Bloomberg index data show.

Through part of that period, the investment committee consulted daily — up from their typical three times a week. They also monitored clients to gauge whether there actually was a move by foreigners to dump US government debt.

“Our realization was that investors are not necessarily looking to blanket-sell Treasuries,” Mittal said. “What we were observing was that there was a little more interest in buying US assets on a hedged basis, meaning foreigners hedging their dollar exposure.”

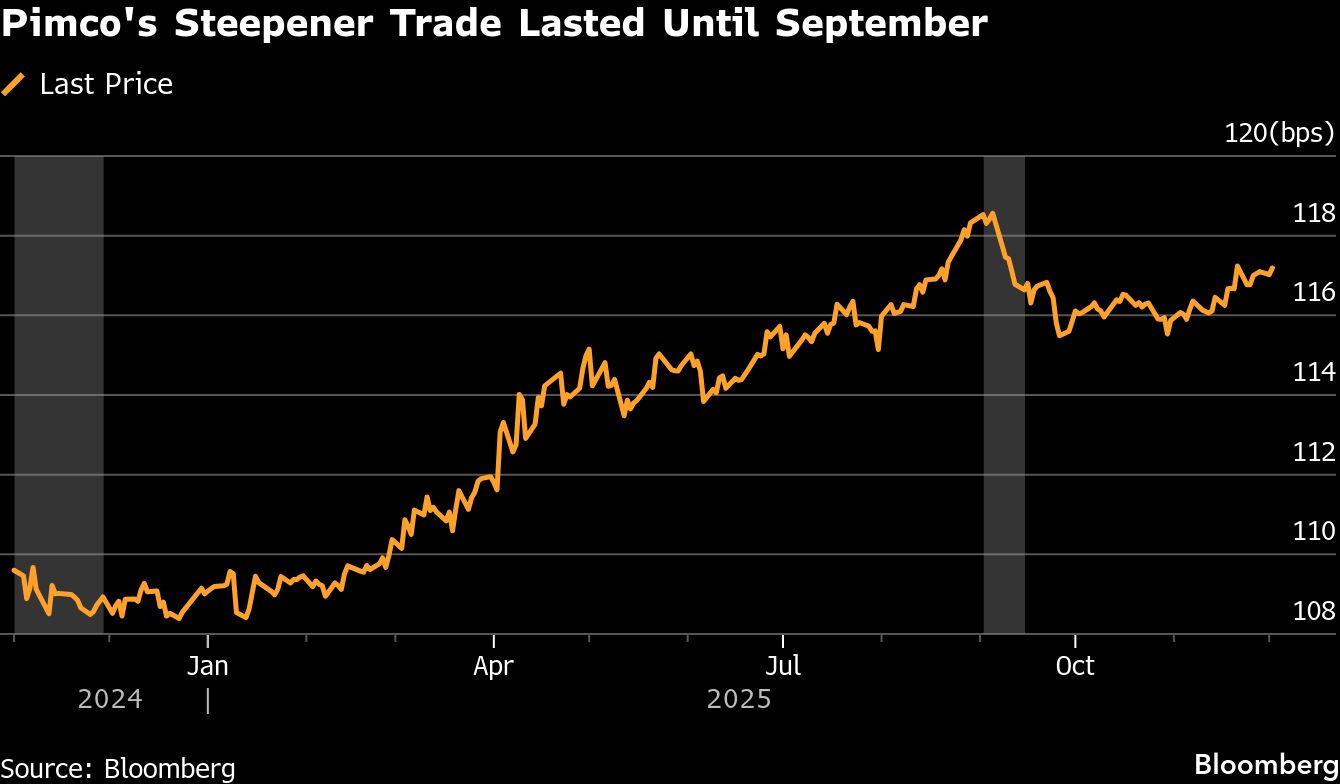

That insight gave them confidence to boost their 5- to 10-year Treasury holdings as yields swung. They also increased mortgage positions when those securities cheapened in the face of all the volatility. Through it all, they also stuck to a bearish view on the long bond, which paid off as that maturity underperformed.

Pimco has since scaled back some of these bets and shifted money to other global debt markets where they see better returns in 2026, but the positions formed the pillars of the firm’s outperformance this year.

Track Record

Pimco, co-founded by Bill Gross, who left the firm in 2014, has a history of getting important calls right in such pivotal moments. Notable examples came in 2007 when it foresaw the housing-market bubble popping, and then in the following years, when it bought mortgages being dumped at fire-sale prices.

The Income fund’s track record of beating its largest rivals on a 3-, 5- and 10-year basis speaks to that success. A Dodge & Cox fund ranked second for those periods.

The challenge of sustaining that performance has only grown for Pimco after Mark Kiesel, CIO for global credit and a member of the investment committee, announced his departure last month. He had been one of the managers of Total Return since 2014. Michael Cudzil has joined the team, which includes Mittal, Qi Wang and Ivascyn.

Surprising Rally

The strength in the US bond market was tough to envision coming into this year, when yields were climbing on bets that Trump’s plans to boost growth and cut taxes would expand the deficit and require more bond issuance. There was also concern that tariffs would increase consumer prices, and his attacks on the Federal Reserve weighed on sentiment as well.

A big reason for the reversal is that the softening job market and the risk of recession spurred the Fed to lower interest rates at its last two meetings — a bullish backdrop for fixed income. Traders expect another cut at the central bank’s next decision, on Dec. 10.

Pimco is hardly the only firm to deliver solid returns this year. Of the 175 active bond funds managing at least $1 billion and benchmarked to the Bloomberg USAgg Index, 90 have at least matched the broad market’s return of just above 7% this year, data compiled by Bloomberg through Dec. 2 show.

However, Pimco’s timing and mix of positioning proved superior among funds of its size.

Back in mid-January, when yields set their 2025 peak, the bond manager touted bonds’ stabilizing appeal given the view that the incoming administration would be a source of unpredictability.

They were also underweight the 30-year area, meaning both the Total Return and Income funds were betting on a steeper yield curve. They anticipated that wager would work because of central-bank easing and angst toward longer-dated bonds resulting from concerns around sovereign debt levels and deficits.

That proved to be a hot trade for much of 2025. In September, Ivascyn said they were taking profit on it by reducing their underweight on the 30-year, initially for the Total Return Fund, and then for Income.

Mittal said the firm now sees better opportunities in other parts of the world. Over the past one to two months they’ve reduced interest-rate exposure in the US and added it in Japan, Australia and the UK, he said.

The shift reflects how “relative to all these other countries, US Treasuries have been the strongest outperformer” this year, he said.

“You are seeing signs of growth slowdown, particularly in the UK and Australia, and hence it seems a little bit of a prudent approach to shift exposures there,” Mittal said. “And we can be patient.”

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.