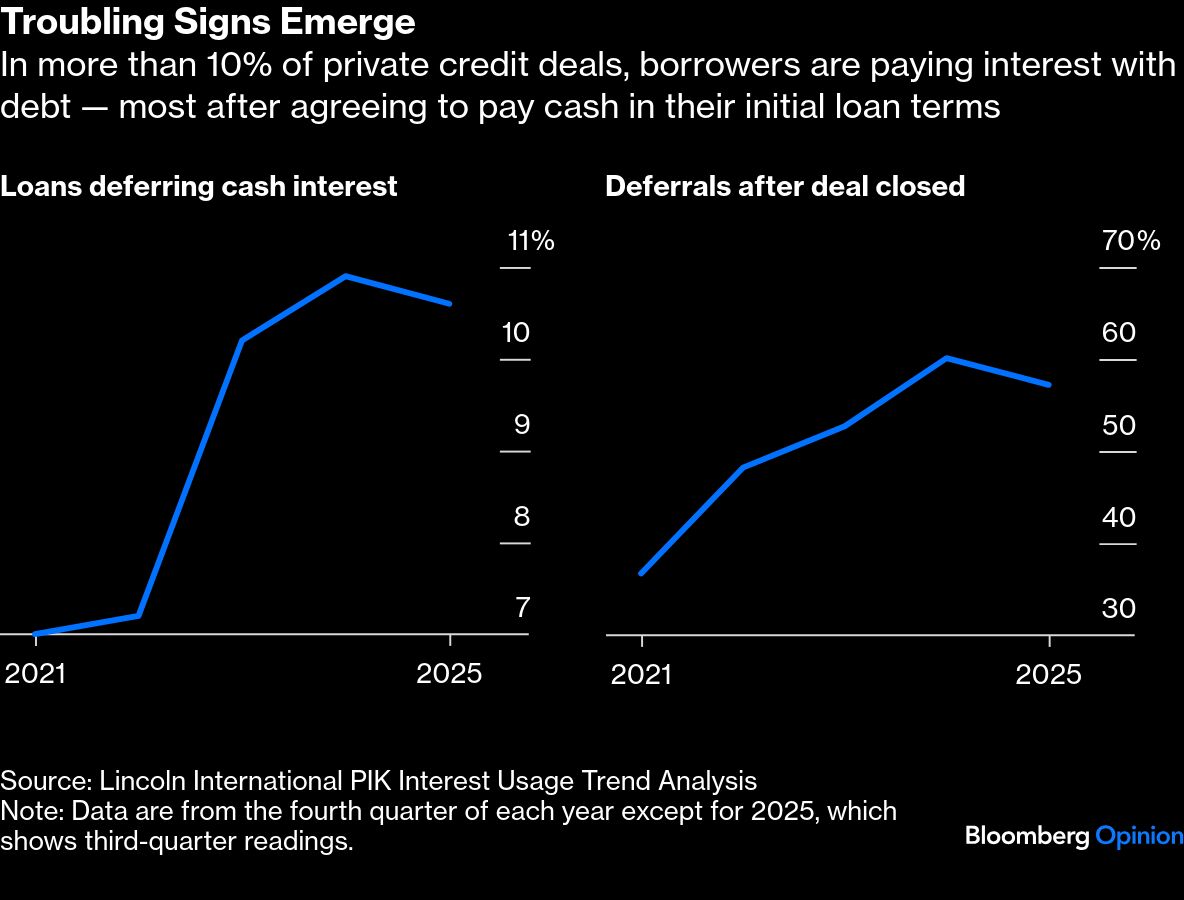

How worried should the US be about private credit? Already this year, more than 1 in 10 private credit borrowers are deferring cash interest payments and at least 45 firms have been taken over by their lenders, the most in six years. Pools of private credit loans managed by BlackRock Inc. and Blue Owl Capital Inc. are showing signs of distress.

The essential question is whether banks are sufficiently insulated from these risks.

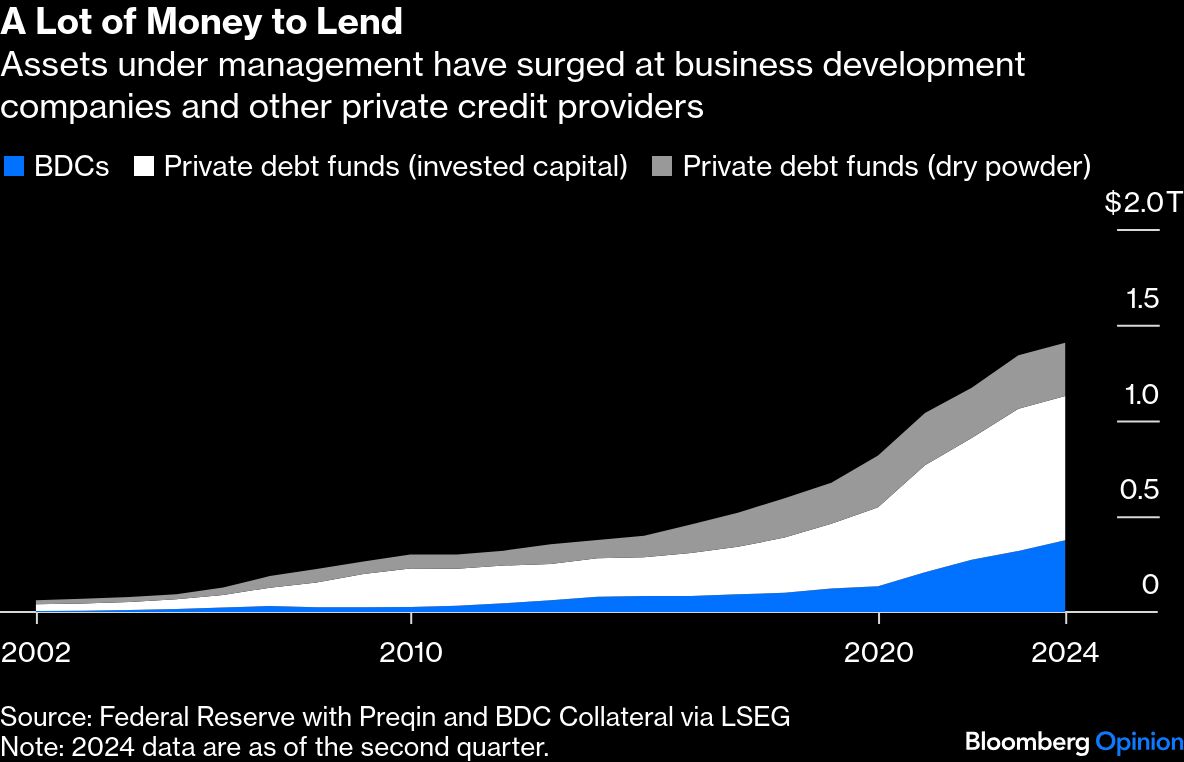

The last credit crisis swamped many of the biggest banks, forcing them to reinforce their balance sheets. As they scaled back lending, fund managers saw a chance to provide “private credit” to companies. The new business grew rapidly: Today, US private credit totals some $1.3 trillion, nearly half the $2.7 trillion in commercial and industrial loans made by commercial banks.

In theory, this should make the banking system safer. After all, most of the money for these loans comes from pensions, insurance companies and other long-term investors. Banks, by contrast, borrow much of their money from depositors and repo lenders who can — and occasionally do — withdraw their funds if they fear they won’t be fully repaid. That’s why banks must have enough ready cash to ride out any panic and sufficient shareholder equity to absorb losses.

Yet problems have lately become apparent. The new ecosystem is now veined with leverage: The underlying borrowers, the private credit funds and the funds’ investors have all taken out loans, often from banks. Moody’s Ratings estimates that US banks have lent $585 billion to private credit and private equity funds and have extended a further $340 billion in commitments to both.

Lending to lenders — on average, 9% of US and European bank loans are now made to nonbank financial institutions, including private credit — is considered less risky than having more direct exposure to borrowers. That reduces the equity cushion that regulators require banks to hold against potential losses. But it can also obscure underlying hazards.

Private credit exposures are opaque and increasingly convoluted, with funds making loans backed by a wide range of esoteric collateral, even repackaging fund stakes into assets. A lack of public trading leads to loan values that are subjective and disputed. It can also lead to shocking markdowns: Within weeks, BlackRock revised one loan’s value to zero from 100 cents on the dollar.

Those features create extra risk if things go wrong. US banks with the most exposure to nonbank financial institutions are also those most dependent on markets for their funding, according to the International Monetary Fund. One lesson of 2008: If investors aren’t sure how exposed a bank might be to losses, best not to wait around to find out. That’s a recipe for a financial crisis.

Ideally, regulators would have a clear, real-time picture of every institution’s exposure to losses from private loans, credit funds and the entire interconnected ecosystem of related companies (insurers, for instance, but also banks that have depended on trades with credit funds to offload some of their own credit risk).

Failing that, the best defense is capital and liquidity. Although requirements for loss-absorbing equity have been raised since the last credit meltdown, banks’ levels were still inadequate even before the administration decided to loosen leverage-ratio rules at big banks and small community lenders. To fend off runs, banks should pre-position enough collateral at the Federal Reserve to ensure they can cover all their short-term liabilities.

Banks might be better shielded from the worst outcomes this time around. But the first signs of danger are nonetheless visible on the horizon. It’s a good time to batten down the hatches.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by The Editors