Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Starting in the aftermath of the 2008 financial crisis, a profound change to the Fed’s liquidity-providing role in the capital markets was underway. We can sum up the Fed regime change with a popular quip: The Fed has shifted from lender of last resort to the lender of only resort.

In our articles, "QE Is Coming" and its follow-up, "How The Fed Deals Liquidity," we discuss why the Fed has become the primary liquidity provider since 2008 and the tools it uses to maintain ample liquidity in the markets. While that Fed regime change has had an incredible impact on the financial markets, there is a growing possibility of another meaningful regime change that could prove equally consequential.

Admittedly, this article, like the two linked above, is dry. However, investors today must understand that monetary policy has become a primary driver of liquidity, which in turn significantly influences asset prices. Without a clear understanding of the Fed’s operations, your investment ideas — no matter how solid — can be flawed.

Groupthink Has Been the Fed Norm

The Fed’s monetary policy-setting group, the Federal Open Market Committee (FOMC), meets every six weeks to discuss the economy, financial markets, and liquidity. These discussions guide the Fed in setting monetary policy to meet its inflation and employment objectives.

After two days of data analysis, conversation, and debate, the FOMC’s voting members vote on whether to adjust monetary policy. Most often, the policy changes involve the federal funds rate and/or the monthly pace of quantitative easing (QE) or quantitative tightening (QT).

The committee is composed of the following members:

- Seven members of the Board of Governors, including the Chair

- The president of the New York Fed

- Four rotating regional Fed Presidents

While there are debates and diverging views expressed at the FOMC meetings, the published results always give the impression of agreement. This is evident in the meeting statement, which lists the members who voted for the monetary policy actions and those who dissented. The example below, from the October 29, 2025, meeting, shows that two of the twelve members dissented, or voted against, the prescribed policy actions.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michael S. Barr; Michelle W. Bowman; Susan M. Collins; Lisa D. Cook; Austan D. Goolsbee; Philip N. Jefferson; Alberto G. Musalem; and Christopher J. Waller. Voting against this action were Stephen I. Miran, who preferred to lower the target range for the federal funds rate by 1/2 percentage point at this meeting, and Jeffrey R. Schmid, who preferred no change to the target range for the federal funds rate at this meeting.

Historical Dissents

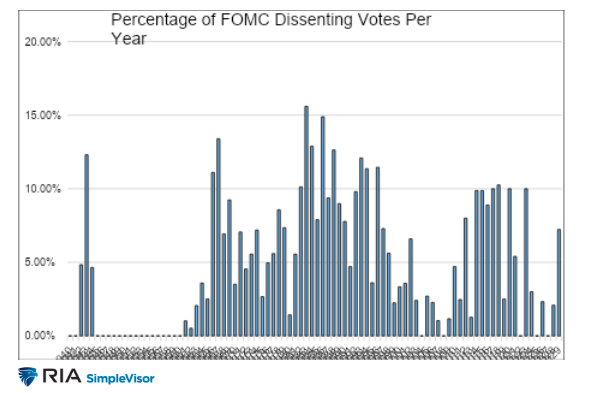

On average, 5% of FOMC members have cast dissenting votes per meeting since 1936. Since 2000, the maximum number of dissenting votes at a single meeting was three. Over the last 25 years, there has been a roughly 50% chance that at least one member would dissent at any given meeting.

The bottom line is that while dissents occur with some regularity, the votes for or against policy action are always a strong consensus.

Consensus At the Fed

We can gain a better understanding of the debates that took place in the FOMC minutes that are released three weeks after the meeting. It's clear from these minutes that there are many diverging opinions. This should not be surprising, as the members come from different regions across the country and have diverse economic views. This has been the case since 1936, when the Fed began sharing the minutes.

While there may be many views on the economy and the right course for monetary policy, the graph above clearly shows that almost all Fed members coalesce around a single policy action. Additionally, the Fed Chair often steers the FOMC toward presenting a consensus view.

Politics at the Fed

Despite its supposed independence from the executive branch, we argue the Fed has always been political to some degree. Furthermore, we must assume that every Presidential nomination of a Fed member is primarily based on the nominee's alignment with the President's views.

Thus, it's not shocking that Stephen Miran, appointed by Trump, is arguing for aggressive rate cuts. Furthermore, Trump’s appointee to replace Chairman Powell when his term ends in May, and potential appointee to replace Lisa Cook, will most likely also hold dovish views.

Despite the inflow of likely dovish FOMC voters, there also remains a camp of hawkish voters. It appears that most of the dovish-hawkish standoff is a function of whether members are more concerned about keeping a lid on inflation (hawkish) or about preventing a worsening of the labor market (dovish).

However, the debate may be becoming political as well. Is the Fed morphing into entities like the Supreme Court or Congress, which are politically motivated?

In other words, are some dovish members not as concerned about the labor markets as they appear, and instead pushing for a more accommodative policy to help Trump achieve his economic goals? Conversely, might some hold hawkish opinions, not because they fear inflation, but because they disagree with the President’s policies?

Is Consensus Dead?

If the Fed is becoming more politically divided, could the Fed Chair lose the ability to present a group consensus? Interestingly, the odds of a rate cut at the next Fed meeting have been floating between 25% and 85%. Those odds have been shifting as various Fed members have weighed in on whether they may cut rates at the next meeting. Currently, there is a split between those wanting to cut rates in December and those dissenting. A few members also appear undecided. If the Chair is unable to get the members to reach a consensus, it's quite possible there could be four, five, or even six dissenters at the next meeting.

Our Take on Dissents

Historically, as we noted earlier, the Chair gets the FOMC to form a strong publicly facing consensus. Doing so gives investors, consumers, and business leaders a false sense of confidence that the Fed is fully aware of what is happening in the economy and that it has the right policy prescription.

Groupthink, as managed by the Chair, has led to significant policy errors. The Fed will still make errors in the future; however, investors, business leaders, and consumers will at least be better versed in other policy opinions. For instance, multiple dissenting votes signals that the Fed is not confident in its views or policies. While that may make some people uneasy, it's better to recognize their stance than to believe something that isn't true. Conversely, in an era of multiple dissenting votes being the norm, a complete consensus should lead investors to think the Fed has strong confidence in its views and policies.

Summary

As we said earlier, we welcome change. We want 12 autonomous FOMC members deliberating and voting on Fed policy. We don’t like the opinion of one person, the Chair, dictating the views and policies of the Fed.

A new Fed regime consisting of 12 voting Fed members, voicing their own opinions and casting votes on what they think — not what the Chair wants — would be a welcome change — although it might introduce short-term volatility in the financial markets.

Michael Lebowitz is a portfolio manager with RIA Advisors and author for Real Investment Advice. For more information, contact him at [email protected] or 301.466.1204.

Join RIA Advisors and elevate your career within a deeply experienced team focused on innovation. Our collaborative environment is built on a foundation of advanced technology and effective investment models, designed to enhance your ability to serve clients and grow your practice. Benefit from a supportive culture that encourages professional development and fosters a forward-thinking approach. By joining our team, you’ll be part of a group dedicated to excellence and continuous improvement, empowering you to focus on building meaningful client relationships and pursuing your business ambitions. Discover the advantages of working with our accomplished advisory team by starting your conversation today.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more articles by Michael Lebowitz

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.