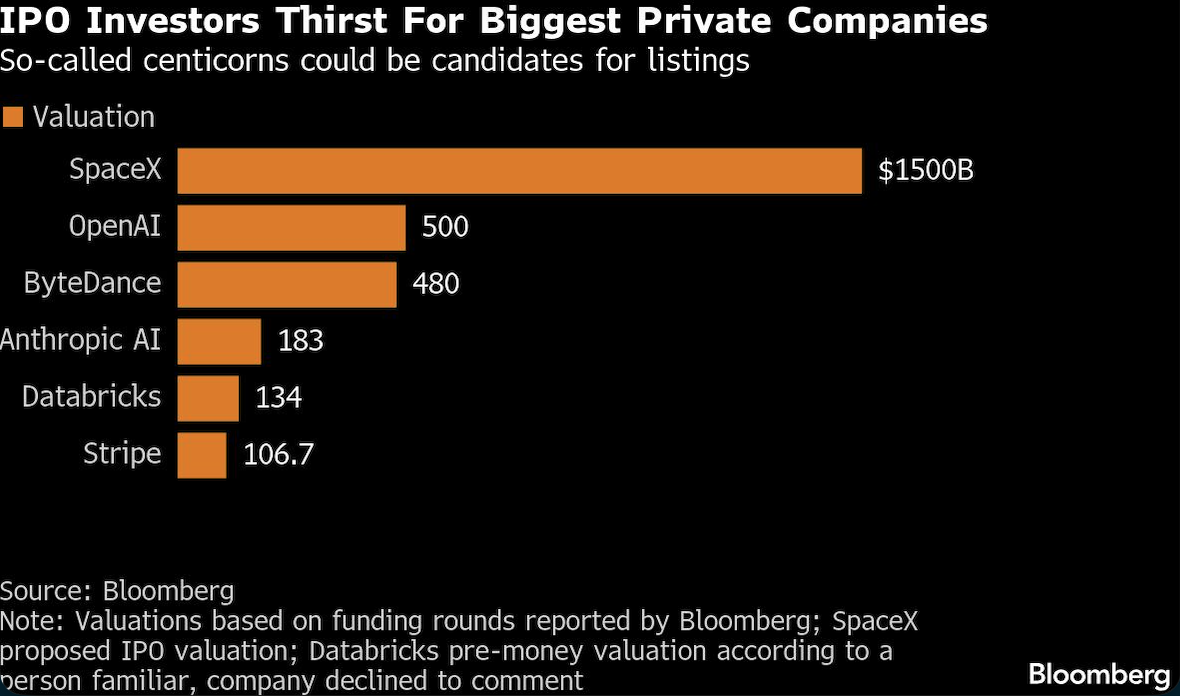

The floodgates could be poised to burst open on Wall Street for $2.9 trillion worth of private companies that have avoided going public for years.

The prospect of a SpaceX IPO, preparing the ground for so-called centicorns valued privately at $100 billion or more, raises a dangerous question for all involved: How eager will stock investors be to embrace companies with controversial leaders, little or no profits and private-market valuations so swollen that they’ll dwarf every company that has previously made its debut on a US exchange?

Short answer: Very.

“The median market cap of an S&P 500 company is close to $40 billion; this is a completely different stratosphere,” said Paul Abrahimzadeh, a partner at 1789 Capital and a former co-head of equity capital markets for North America at Citigroup Inc. “A company like SpaceX will clearly cater to a wide swath of institutional investors — as well as retail — and is a must-own name.”

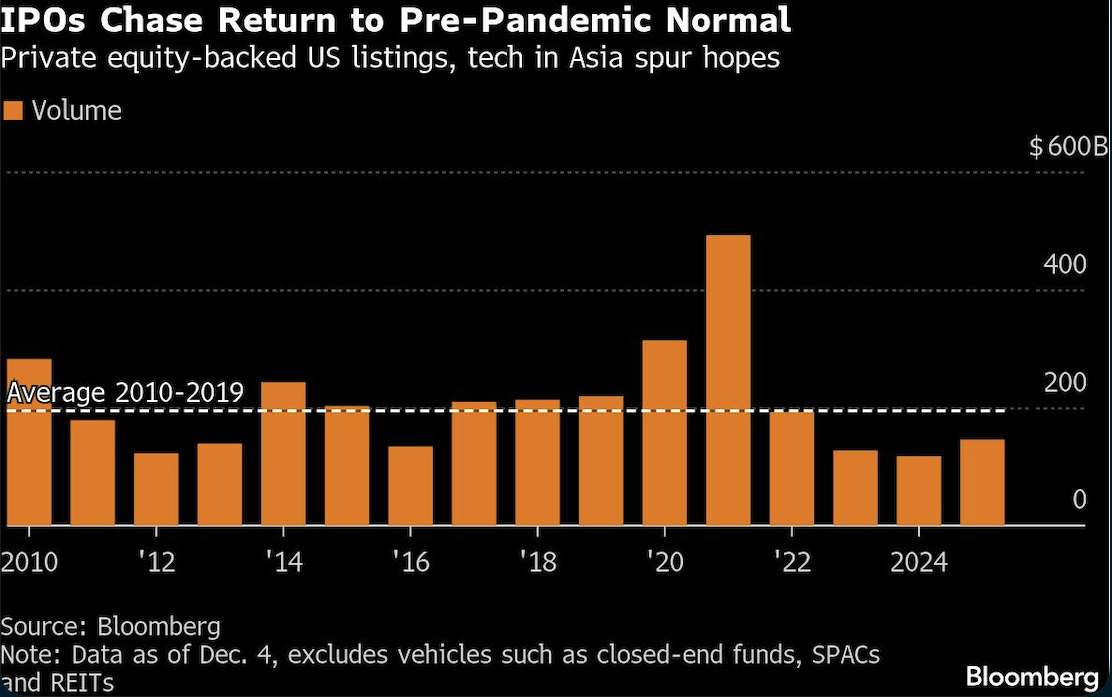

IPOs have been more or less stuck in a rut since a record $492 billion year in 2021, and companies like SpaceX, Stripe and ByteDance that once would have been candidates for listings have attracted valuations in private funding rounds that leave most public companies in the dust, all without being exposed to the scrutiny that quarterly financial reporting brings.

The wailing of investors denied access to the hottest big companies was just about drowned out by investment bankers bemoaning the chunky IPO fees they’ve been missing out on. If Elon Musk’s rocket giant goes public at a valuation even close to the $800 billion it’s been seeking in its latest private round — or for that matter the $1.5 trillion value it’s considering in a listing — it would be a powerful vote in favor of leaving the private sphere.

“A lot of people over the last few years have felt the super high-value private companies don’t need to go public and maybe they’d never go public,” said Steve Studnicky, UBS Group AG’s co-head of Americas ECM. “Now, these companies are coming forward saying there is a path to a public listing and that’s helpful for a lot of companies and investors who want to see them lead the way.”

A lot of these companies are too big to be sold, said 1789’s Abrahimzadeh, whose firm is an investor in SpaceX. “So this is going to kick off a massive trend of IPO activity — yes, we’ve been saying that for years — but there are no more excuses in 2026.”

Bankers say mega-listings are doable, even if the structure needs to be carefully considered. Still, some centicorns will have work ahead of them to justify their valuations to investors. SpaceX is expected to produce about $15 billion in revenue in 2025, increasing to between $22 billion and $24 billion in 2026, a person familiar with the matter has said.

“I’m not worried about the IPO market capacity if you can make the math work. But I’d be suspect if OpenAI or SpaceX are really worth $1 trillion or $800 billion just based on what I understand their revenues are and what their growth rates are,” said David Erickson, an adjunct associate professor of business at Columbia Business School and a former co-head of global equity capital markets at Barclays Plc.

“You have to make the math work for public investors to get behind them in a big way.”

Public Market Spotlight

SpaceX offers a case study for those who believe the public markets are the best place for a huge company, as well as those who question whether these firms can handle the public market spotlight.

Fans see an innovator pushing the boundaries of what’s possible in space exploration. SpaceX has pioneered partially reusable rockets, and is the only commercial US company capable of launching humans on its own to orbit. The company also currently operates the largest single satellite constellation ever created, which beams broadband internet coverage to more than 8 million customers, according to its website. And it’s slated to jump start its direct-to-cell business with the recent acquisition of EchoStar’s radio spectrum.

On the other hand, going public might complicate SpaceX’s capital-intensive plans, such as developing its behemoth Starship rocket — a fully reusable vehicle that it plans to use to launch future Starlink satellites and eventually fly humans to the moon and Mars. Musk and SpaceX would be beholden to shareholders who may be focused on shorter-term revenue and profits.

“So much of SpaceX’s identity and culture reflects independence,” Carissa Christensen, founder and chief executive officer of BryceTech, a space research and analysis firm, said. “It is hard to imagine SpaceX as a publicly traded company with the ground rules and guide rails and scrutiny that go with that.”

Musk has said before that SpaceX would not IPO before the company had achieved its ultimate goal of sending humans to the Red Planet, a point reiterated by President Gwynne Shotwell in 2018. “We can’t go public until we’re flying regularly to Mars,” Shotwell told CNBC in an interview.

Even if the company’s changed its mind on a listing, some investors may still be wary. If SpaceX offered 5% of the company at a $1.5 trillion valuation, it would have to sell $75 billion of stock, easily making it the biggest IPO of all time. While state-backed Saudi Aramco raised $29 billion in a listing in 2019 in favorable conditions — debuting in its home market and with no international offering — some question whether a company with a relatively short track record, and led by a figure like Musk, who already runs a $1.5 trillion dollar company, would have a similarly warm reception.

“The challenge I would have with SpaceX is not just the math, but from an investor perspective governance would be a concern,” Erickson said. “Elon Musk could be a CEO of two huge public companies and then he’s got xAI, I would think people would be concerned about things like that.”

Return of the Mega-IPO

A SpaceX listing as soon as mid-2026 could resolve the disconnect between public and private markets in a flood of mega-deals that some investors can’t afford to miss.

As Rob Stowe, Barclays’ head of Americas ECM, put it: “Large deals have their own gravity.”

A single IPO that brings in more than $50 billion would trump the listing volume on US exchanges annually in eight of the past 13 years, data compiled by Bloomberg show, when removing SPACs and closed-end funds.

If an investor sits out an IPO that raises $500 million or less and it does well, that won’t really impact their performance, Stowe said. However, “if you choose not to participate in a $30 or $50 billion IPO that does really well, that creates some significant challenges.”

Looming over the whole enterprise is the concern that IPOs of this size have never been attempted.

“These will be massive events,” said Morgan Stanley’s Colin Stewart, vice chairman of global technology M&A and capital markets. Among the potential challenges: “Making sure the infrastructure can handle it.”

Path to Public

For very large private companies that don’t really need to raise money, Stewart believes a direct listing – letting investors sell their shares on an exchange without an IPO preceding the trading — offers an appealing route to markets.

“There’s no direct listing on file but it’s got to be considered for some of these large companies,” said Stewart. “They’re not desirous of capital, they have shareholder bases that look similar to a public company in terms of the number of institutions. All they’re really missing is retail.”

Of course, the length of time these companies have stayed private, and the sheer amount of money raised, has resulted in shareholder bases that are not only larger than would be typical for an IPO candidate, they’re also more diversified. That could result in a direct listing being more actively discussed, according to Stewart.

Coinbase Global Inc.’s debut in 2021 is the largest direct listing to date. Other high-profile direct listings include Palantir Technologies Inc. and Roblox Corp., which took place during the market’s Covid boom when the threat of volatility prompted some dealmakers to try to de-risk their deals.

For portfolio managers that have billions of dollars tied up in private companies, the ability to return cash to their investors is top of mind. A McKinsey & Co. survey of these so-called limited partners in January showed that returns were rated among the most important metrics when evaluating managers — a figure that had climbed sharply from three years before.

The need for returns may be a driver that ultimately kicks some of the closely-held firms to public markets. Others have more options. The question Morgan Stanley’s Stewart often gets is, “Why even go public when private markets are so good?”

Counter-point: what happens if private fundraising freezes up? “A downturn happens every five to ten years — and it can flip on a dime,” he said.

“Liquidity right now seems great but it’s not a guarantee that liquidity will be there tomorrow,” he said. While companies have been able to let long-term investors and employees sell shares from time to time, there is likely a limit, according to Stewart.

“At some point it gets harder and harder for you to sell the next tranche to the next person at a higher valuation — it just does,” he said. “So just go public, and let the market sort it out.”

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.