Anyone wanting reassurance that building the infrastructure for artificial intelligence isn’t going to break the bank, won’t have enjoyed Oracle Corp.’s latest earnings report. Wall Street’s de facto barometer of AI fears served up several unwelcome surprises, including $10 billion of quarterly cash burn and a massive increase in capital spending.

More worrying, it failed to satisfactorily answer two simple questions: Just how much is all of this going to cost, and what happens if its cornerstone customer, OpenAI, can’t pay?

Having been slow at first to embrace cloud computing, the near 50-year-old database and enterprise-software firm is pursuing a breakneck expansion to catch-up with the likes of Amazon.com Inc. and Microsoft Inc. by kitting out gargantuan AI data centers (it doesn’t own the buildings.)

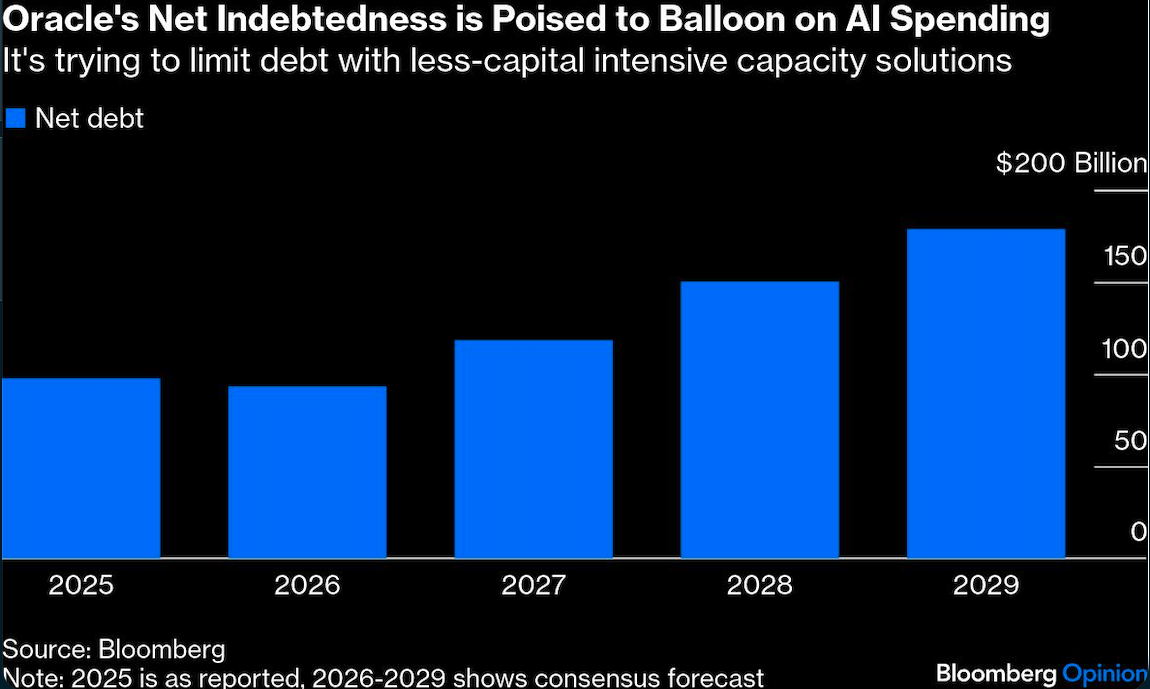

It will then rent out computing capacity, a lower-margin business than most of its other activities in part because it uses Nvidia Corp.’s expensive AI chips and they incur heavy depreciation costs. At the same time, its balance sheet and cash flows are far less ironclad than the so-called hyperscalers such as Amazon, Microsoft and Google. It will probably need to borrow tens of billions of dollars to compete — a level of capital intensity Oracle shareholders aren’t accustomed to.

The company already has about $105 billion of net debt including lease obligations, according to data compiled by Bloomberg, pushing it toward the more indebted end of investment-grade borrowers.

Set against this, Oracle’s $523 billion of contracted future revenue sounds impressive — it’s roughly five times higher than a year ago. But more than half of that relates to its work for Sam Altman’s OpenAI, a heavily loss-making startup whose early AI lead no longer looks unassailable. With the vastly richer Google gaining ground, and its new Gemini model winning rave reviews, Altman has declared “code red.” If I were Oracle, I’d be worried too.

These sobering realizations mean the cost of insuring Oracle’s large debts against default — a barometer for how credit investors view its prospects — has spiked, albeit to levels that still aren’t too prohibitive. And its stock price has unwound the massive gains made in September after it reported a surge in AI bookings. The shares fell another 11% in premarket trading on Thursday.

So I didn’t envy the new co-chief executive officers, Clay Magouyrk and Mike Sicilia, hosting their first earnings call since taking over from longtime Oracle boss Safra Catz. Cofounder and chairman Larry Ellison, who’s busy backstopping his son’s $108 billion hostile bid for Warner Bros. Discovery Inc., made only brief remarks.

Magouyrk wasn’t being evasive when he said it’s “hard to answer” exactly how much money Oracle must raise to fund its AI ambitions: It depends on whether the company has to buy its chips from Nvidia Corp. and Advanced Micro Devices Inc., or whether it can find cheaper methods such as renting them or getting customers to provide their own equipment. Presumably these other options might require Oracle to sacrifice some profitability.

Oracle will need less, “if not substantially less,” than the more than $100 billion some analysts reckon it will have to find for its AI build-out, Magouryrk contended. The company is committed to keeping its investment-grade debt rating. It had $19 billion of cash at the end of November, having raised $18 billion via a jumbo bond sale a couple of months ago.

But if analysts’ financial models are out of kilter, Oracle is partly at fault. Until it provides more clarity about the capital needed to support its extraordinary growth ambitions, the suspicion will remain that it has effectively allowed OpenAI to lean on its balance sheet. By getting Oracle to do the hard and costly legwork of setting up and running the data centers that it will use, Sam Altman’s startup doesn’t have to raise as much cash.

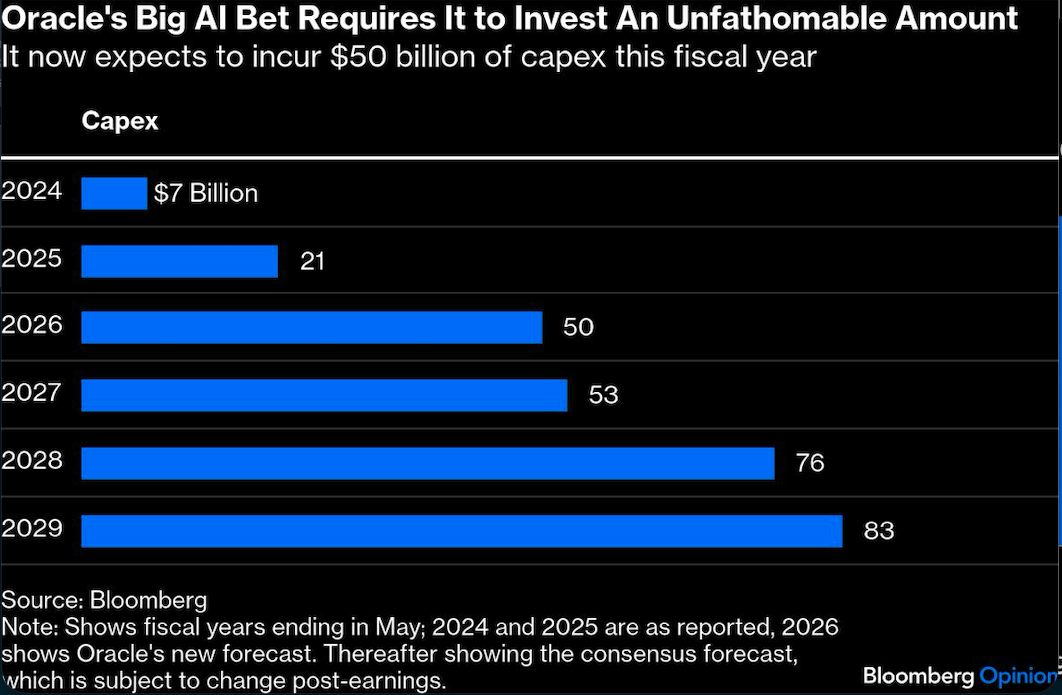

A 40% hike in expected capital spending to $50 billion for the fiscal year to May hasn’t eased investor anxiety — even if it reflects its success in winning new business. The sum is equivalent to three-quarters of projected revenue. Alphabet’s capex bill is worth about 27% of this calendar year’s sales.

AI data-center deals are designed to recoup the capital spending over the contract’s lifespan, and lease payments don’t start until the site is finished. Encouragingly, Oracle plans to remain flexible about which chips to deploy (lessening the risk of obsolescence); and it doesn’t pay for equipment until late in the construction process, minimizing the period when it’s not making money. Apparently, it’s also straightforward to repurpose unused capacity. Computing power gets reallocated “very quickly,” Magouyrk said.

Still, this doesn’t soothe investor fears about the OpenAI exposure. The $300 billion contract between the two companies is reportedly spread over only five years, whereas Oracle’s property leases are typically at least twice that long.

Should OpenAI back out, Oracle might be left with costly rent payments to the data-center building owners — and a big hole to fill depending on how many sites it had equipped and how much demand for AI services there is at that juncture. Oracle has more than $16 billion of operating lease liabilities on its balance sheet, plus almost $250 billion of lease commitments that have yet to begin. That implies several billion dollars of future annual lease expenses that it will need to honor.

“There’s a clear possibility that OpenAI will not be able to live up to its contractual obligations,” Gil Luria, head of tech research at DA Davidson, told me before the earnings. He called the OpenAI contract “fantasy” and said the likelihood it will have $300 billion to spend with Oracle is “negligible at this point.”

If that’s the case then Oracle might end up having to revise its ambitions to roughly quadruple revenue by 2030, further denting investor confidence.

A tech company that’s been around for five decades has successfully navigated tech upheaval before, of course, and it can still be an AI winner. Being custodian of the world’s corporate data is very handy when businesses are trying to glean insights from all of that information using large language models. Investors must be frustrated that its consistent double-digit sales growth is no longer being rewarded by the stock market.

Still, there’s a reason for the jitters. To justify the earlier hype, Oracle will have to execute its AI build-out perfectly while finding other customers. Booking $68 billion in contracted revenue in the third quarter from deals with Meta Platforms Inc., Nvidia and others helps. It’s the codependent OpenAI relationship that’s the troubling specter in Oracle’s AI data room.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.