There’s no such thing as a sure thing in markets, but some things come pretty close. One of them is the proposition that there will be more interest-rate cuts next year — and another is that these reductions will have little to no effect on long-term rates.

First, about the cuts. Federal Reserve Chair Jay Powell may have presided over his last announcement of a decrease, but odds are his successor will reduce rates further next year. It’s not just that President Donald Trump wants lower interest rates, which boost the stock market and consumer borrowing, and make servicing the national debt cheaper. It’s that there are financial risks in the current environment, in which rates are high after a long period of being exceptionally low: Getting rates back down may help the US avoid a credit crisis.

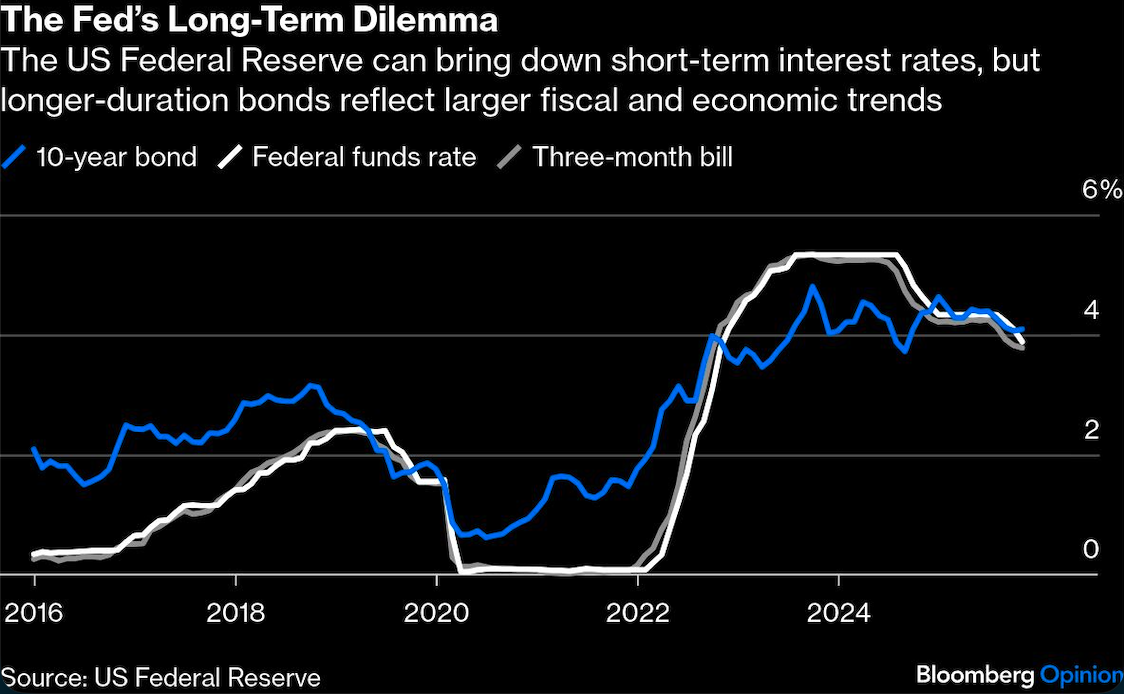

But the government and financial markets may be in for a rude awakening. Even if (when?) the Fed brings down short-term rates, the 10-year US Treasury bond yield will almost certainly not go down very much — at least not without significant financial repression.

It is as predictable as it is inexplicable: The Fed cuts rates and long-term yields go up. It could be that the market is skeptical that the likely next Fed chair, Kevin Hassett, will be serious about inflation. But even if Trump nominated the next incarnation of Paul Volcker, the Fed won’t be able to lower the 10-year yield.

This may seem strange — in theory, the 10-year bond is supposed to reflect what people expect the future short-term yield to be. If the Fed is committed to easing in the future, rates should go down. And often the 10-year rate does follow the Fed policy rate.

But not always. Longer-term interest rates reflect more than future expected short-term rates. This is why the market for bonds of different durations is segmented. The Fed’s influence is greatest on any bonds of less than five years duration; as bonds get longer-term, it has less influence. Longer-term bonds are more affected by market forces. Their yields reflect expected future inflation, inflation risk, and a risk premium for holding an asset with more price variability than a short-term bond.

Lately, all these factors are keeping rates high. Inflation appears to be holding steady at 3%, yet the Fed has already started easing by cutting rates and ending quantitative tightening. There is anxiety about inflation staying high because the full impact of tariffs has yet to be felt, and the Fed has not indicated (short of some wish-casting in its summary of economic projections) that it is committed to bringing inflation down further. There is even less commitment in Congress to reducing the debt, which means more bonds will be issued in the future, which means a drop in bond prices. This makes holding longer-term bonds riskier, and investors want a bigger premium to compensate for that.

It all adds up to upward pressure on long-duration bond yields — no matter what the Fed does with short-term rates.

Even if the Fed found religion on inflation and Congress suddenly cared about the debt, there would still be reason to expect long-term bonds to be higher. Historically, bond yields revert to the mean: Unlike stocks, they rise and fall around a long-term average that is higher than it was in the 2010s. Over time, the 10-year yield has declined simply because world got less risky and sovereign defaults became less common.

But that long-term average still exists. The reason is that, current macro factors aside, long-term yields reflect things that don’t change much over time, such as how productive capital is and how much society values the future compared to the present. Economists have also long thought an aging population would bring down yields because older societies are less productive and buy more debt, but we are less sure of this than we used to be.

A stubbornly high 10-year rate will no doubt frustrate many politicians, not to mention central bankers. It means mortgage rates won’t go down, makes servicing the national debt more expensive, and raises the likelihood of a “credit event” as firms’ debt comes due and they can’t afford to refinance. Alternatively, the economy might just slow down, exposing the ineffectiveness of the Fed’s monetary policy.

So expect the government to try to do more to lower longer-term rates. The Fed could begin large debt purchases again, despite the dismal record of so-called quantitative easing, while the Treasury could use regulations to essentially force banks to buy more debt, part of a strategy called financial repression that has an equally bad reputation. They should be wary. Messing with the price of risk — which is what bonds represent — tends to create more problems than it solves.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.