It’s been three years since OpenAI set off euphoria over artificial intelligence with the release of ChatGPT. And while the money is still pouring in, so are the doubts about whether the good times can last.

From a recent selloff in the shares of Nvidia Corp., to Oracle Corp.’s plunge after reporting mounting spending on AI, to souring sentiment around a network of companies exposed to OpenAI, signs of skepticism are increasing. Looking to 2026, the debate among investors is whether to rein in AI exposure ahead of a potential bubble popping or double down to capitalize on the game-changing technology.

“We’re in the phase of the cycle where the rubber meets the road,” said Jim Morrow, chief executive officer of Callodine Capital Management. “It’s been a good story, but we’re sort of anteing up at this point to see whether the returns on investment are going to be good.”

“The credit people are smarter than the equity people, or at least they’re worried about the right thing — getting their money back,” said Kim Forrest, chief investment officer at Bokeh Capital Partners.

Big Tech Spending

Alphabet, Microsoft, Amazon.com Inc. and Meta Platforms Inc. are projected to spend more than $400 billion on capital expenditures in the next 12 months, most of it for data centers. While those companies are seeing AI-related revenue growth from cloud-computing and advertising businesses, it’s nowhere near the costs they’re incurring.

“Any plateauing of growth projections or decelerations, we’re going to wind up in a situation where the market says, ‘Ok, there’s an issue here,’” said Michael O’Rourke, chief market strategist at Jonestrading.

Earnings growth for the Magnificent Seven tech giants, which also includes Apple Inc., Nvidia and Tesla Inc., is projected to be 18% in 2026, the slowest in four years and slightly better than the S&P 500, according to data compiled by Bloomberg Intelligence.

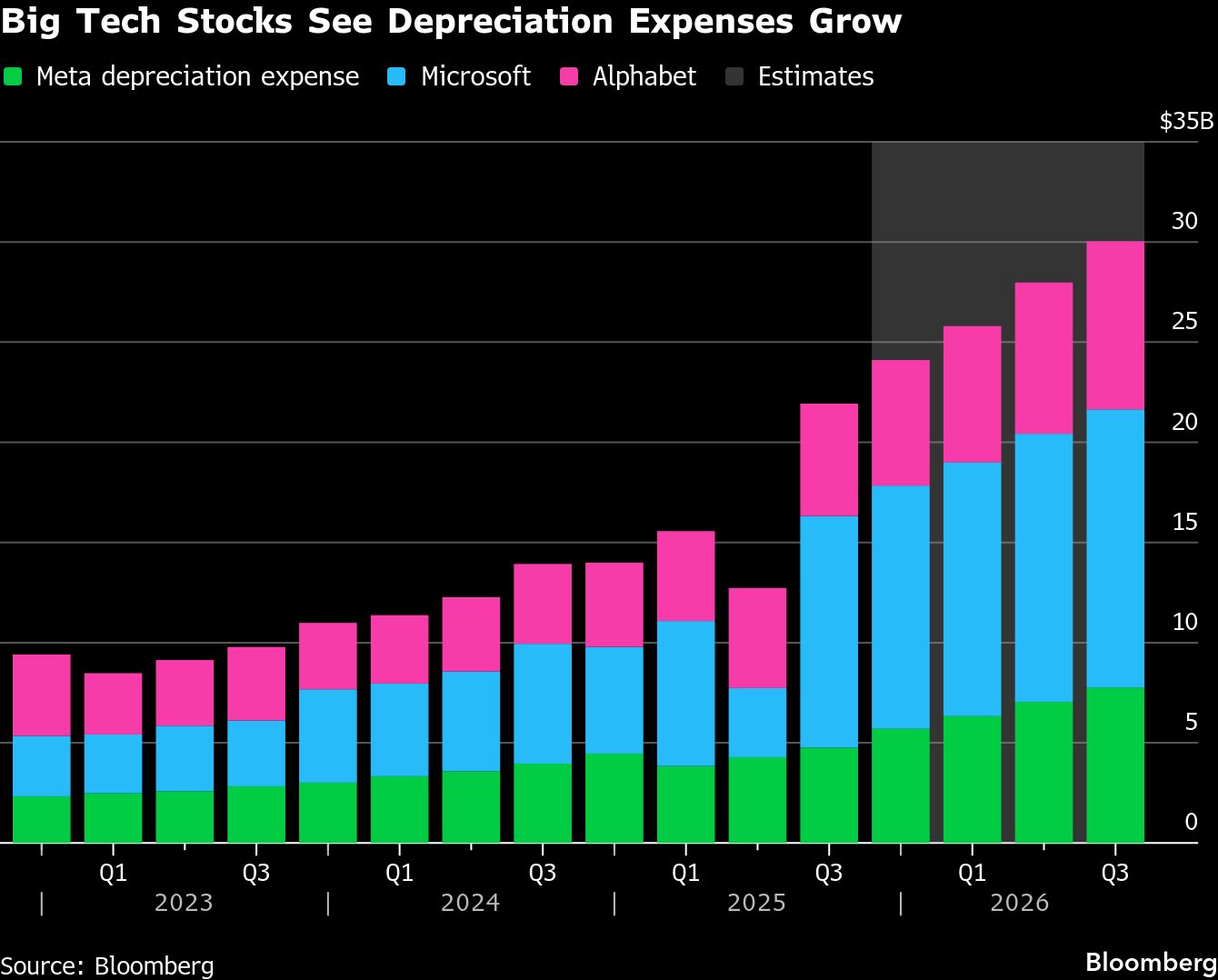

Rising depreciation expenses from the data center binge is a major worry. Alphabet, Microsoft and Meta combined for about $10 billion in depreciation costs in the final quarter of 2023. The figure rose to nearly $22 billion in the quarter that just ended in September. And it’s expected to be about $30 billion by this time next year.

x

All of this could put pressure on buybacks and dividends, which return cash to stockholders. In 2026, Meta and Microsoft are expected to have negative free cash flow after accounting for shareholder returns, while Alphabet is seen roughly breaking even, according to data compiled by Bloomberg Intelligence.

Perhaps the biggest concern about all the spending is the strategy shift it represents. Big Tech’s value has long been premised on the companies’ ability to generate rapid revenue growth at low costs, which resulted in immense free cash flows. But their plans for AI have turned that upside down.

“If we continue down the track of lever up our company to build out for the hopes that we can monetize this, multiples are going to contract,” said Jonestrading’s O’Rourke. “If things don’t come together for you, this whole pivot would have been a drastic mistake.”

Rational Exuberance

While Big Tech’s valuations are high, they’re nowhere near excessive compared to past periods of market euphoria. Comparisons to the dot-com bust are common, but the magnitude of the gains from AI are nothing like what happened during the development of the internet. For example, the tech-heavy Nasdaq 100 Index is priced at 26 times projected profits, according to data compiled by Bloomberg. That figure exceeded 80 times at the height of the dot-com bubble.

Valuations during the dot-com era were far in excess of where they are now partly because of how far the stocks had run, but also because the companies were younger and less profitable — if they had profits at all.

“These aren’t dot-com multiples,” said Tony DeSpirito, global chief investment officer and portfolio manager of fundamental equities at BlackRock. “This isn’t to say there aren’t pockets of speculation or irrational exuberance, because there are, but I don’t think that exuberance is in the AI-related names of the Mag 7.”

Palantir Technologies Inc., which trades at a multiple of more than 180 times estimated profits, is among the AI stocks with nosebleed valuations. Snowflake Inc. is another, with a multiple of almost 140 times projected earnings. But Nvidia, Alphabet and Microsoft are all below 30 times, which is relatively tame considering all the euphoria surrounding them.

All of which leaves investors in a quandary. Yes, the risks are right on the surface even as investors keep pouring into AI stocks. But for now, most companies aren’t priced at panic-inducing levels. The question is which direction the AI trade goes from here.

“This kind of group thinking is going to crack,” Value Point’s Bhasin said. “It probably won’t crash like it did in 2000. But we’ll see a rotation.”

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jeran Wittenstein

x

x