Of all the eye-popping numbers that Oracle Corp. published last week on the costs of its artificial-intelligence data center buildout, the most striking didn’t appear until the day after its earnings press release and analyst call.

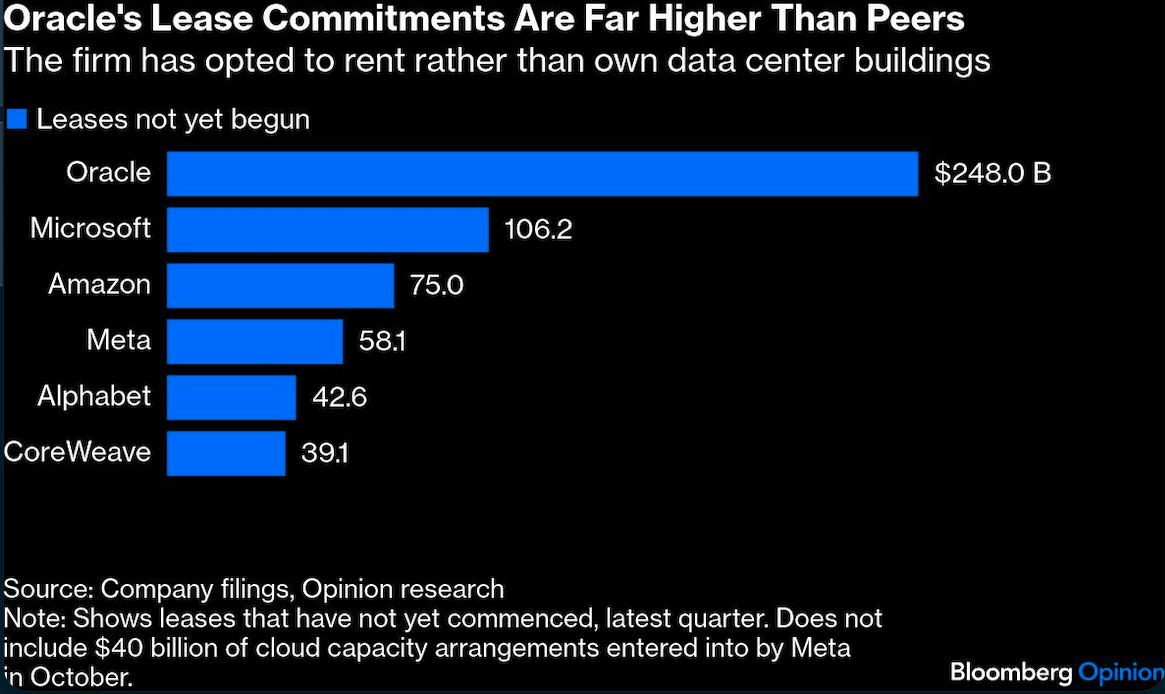

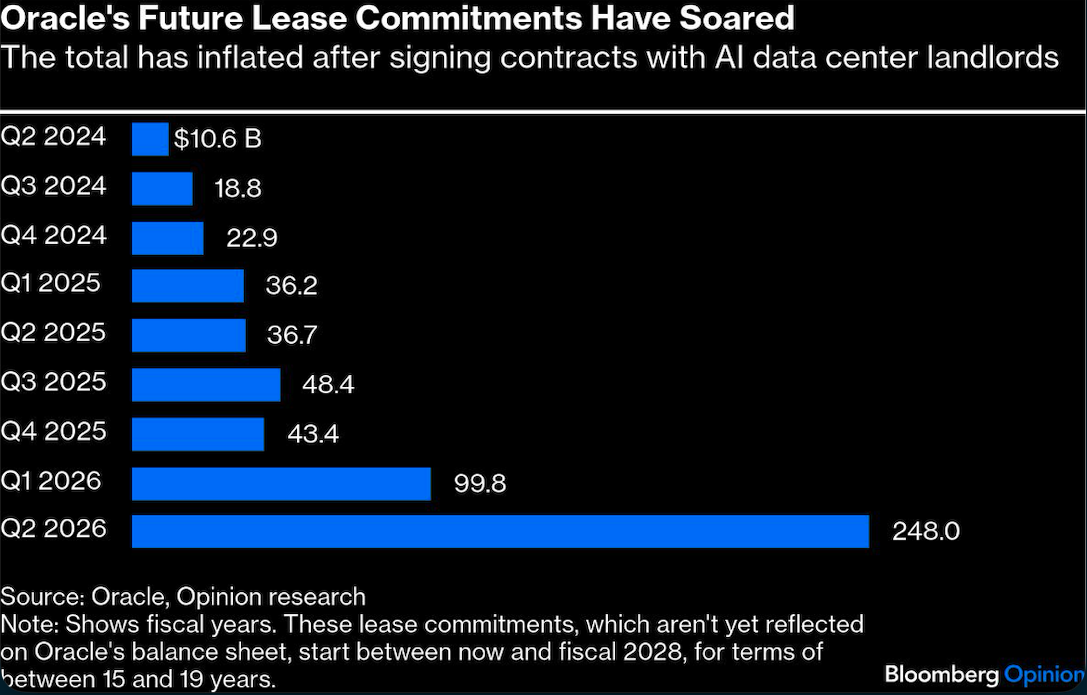

The more comprehensive 10-Q earnings report that appeared on Thursday detailed $248 billion of lease-payment commitments, “substantially all” related to data centers and cloud capacity arrangements, the business-software firm said. These are due to commence between now and its 2028 financial year but they’re not yet included on its balance sheet. That’s almost $150 billion more than was disclosed in the footnotes of September’s earnings update. CreditSights analysts Jordan Chalfin and Michael Pugh called the lease disclosure a “bombshell.”

Although tech investors are becoming wearily accustomed to firms opening the spending taps for AI infrastructure, Oracle’s future lease exposure far exceeds similar commitments by peers.

It could make investors even more skittish about Oracle’s AI infrastructure plans, because of the mismatch between the long duration of the property leases and much shorter contracts with key customers such as OpenAI. The company will kit out and run the data centers for its clients, but it usually won’t own the buildings.

While Oracle doesn’t have to start paying rent until the sites are finished, leases lock in massive annual payments far into the future. And yet AI demand and technology requirements remain uncertain. Analysts and rating companies tend to include an element of the rent obligations when making their own debt calculations.

To recap, this belated convert to cloud computing is mounting a hugely capital intensive effort to compete with the likes of Amazon.com Inc., Microsoft Inc. and Alphabet Inc. in supplying AI infrastructure. Oracle expects capital spending to more than double to $50 billion in its current fiscal year to May. That’s close to 75% of the revenue it’s forecasting over the same period. Analysts expect its cumulative capex bill over the next five years to exceed $300 billion, while free cash flow will probably stay negative for four years.

However, this spending will mainly go on equipment, particularly Nvidia Corp.’s vastly expensive AI chips. It has said that owning the buildings where its servers and networking gear are being installed is “not really our specialty”. It might have added that Oracle’s balance sheet and cash reserves are far less ironclad than other so-called hyperscalers who can afford to own both the shell and what’s inside.

Oracle has a BBB credit rating, toward the lower end of the investment-grade designation that Oracle says it’s committed to keep. It has around $105 billion of net indebtedness, according to data compiled by Bloomberg, including lease obligations that have already begun.

Renting space in a data center lets it spend less money upfront, reducing near-term cash burn. For example, Oracle is relying on a startup called Crusoe Energy Systems to construct the first of its Stargate data centers in Abilene, Texas, with funding coming from Blue Owl Capital Inc.

Oracle’s future lease commitments extend between 15 and 19 years, equating to an average of $14.6 billion in annual lease payments at the mid-point. For context, that’s about two-thirds of the $22.3 billion operating cash flow it generated in the past 12 months. If all goes to plan, these outlays should be manageable because Oracle predicts its cloud-infrastructure division will make yearly sales of $166 billion by 2030, or more than 16 times last year’s total. Its clients are AI leaders such as OpenAI, Meta Platforms Inc. and Chinese tech giant ByteDance Ltd.

During an investor event in October, management said renting AI computing capacity would deliver gross margins of between 30 and 40% — lower than what Oracle got from selling business software, but still pretty handy.

Nevertheless, the company’s own annual report spells out what could go wrong: “If we overestimate customer demand or our data center capacity needs, we could be locked into multi-year commitments for excess data center space, resulting in lower profitability and cash flows because our third-party data center vendors generally require us to pay significant contract termination fees to early exit such obligations.”

Customers renting AI chips from Oracle generally sign up for much shorter contract terms than those leases. Roughly 75% of its $523 billion contracted revenue backlog is expected to be booked in the next 60 months. “Oracle is effectively being paid for taking on lease-duration risk,” Rothschild & Co. Redburn analyst Alex Haissl told the Financial Times last week.

The firm’s $300 billion OpenAI deal is reportedly spread over five years or so but there is growing anxiety about whether Sam Altman’s cash-burning startup will manage to honor its massive spending obligations. If he’s forced to scale back his ambitions or elects not to renew the deal, Oracle would need to find someone else to take that capacity.

Even the boss of Microsoft Corp., which owns a big chunk of OpenAI, is dubious about such customer concentration risks. Satya Nadella told a podcast last month it didn’t make sense for Microsoft to “go be a hoster for one model company with limited time horizon RPO,” referring to remaining performance obligations — another way of saying contracted future revenue. “The thing that you have to think through is not what you do in the next five years, but what you do for the next 50.”

Today, there’s far more demand for AI computing capacity than hyperscalers can deliver and Oracle would doubtless have no problem repurposing its AI chips for another customer. “Whenever we find ourselves with capacity that's not being used, it very quickly gets allocated and provisioned,” Co-Chief Executive Officer Clay Magouyrk said last week.

Nevertheless, some experts fear a future glut. There’s also a danger of technological obsolescence. Oracle depreciates its servers and networking equipment over six years, similar to hyperscaler peers. Even assuming that’s realistic, it faces some very big depreciation expenses and may have to do costly upgrades of the tech in its data centers midway through a lease.

Oracle’s share price has declined 44% since peak AI euphoria in September. Meanwhile, the increase in its borrowing costs threatens to make the buildout even more expensive. It must be frustrating that its boldness is no longer being rewarded by the market. But if it keeps springing surprises like this giant leasing number, investors are bound to be jumpy.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.