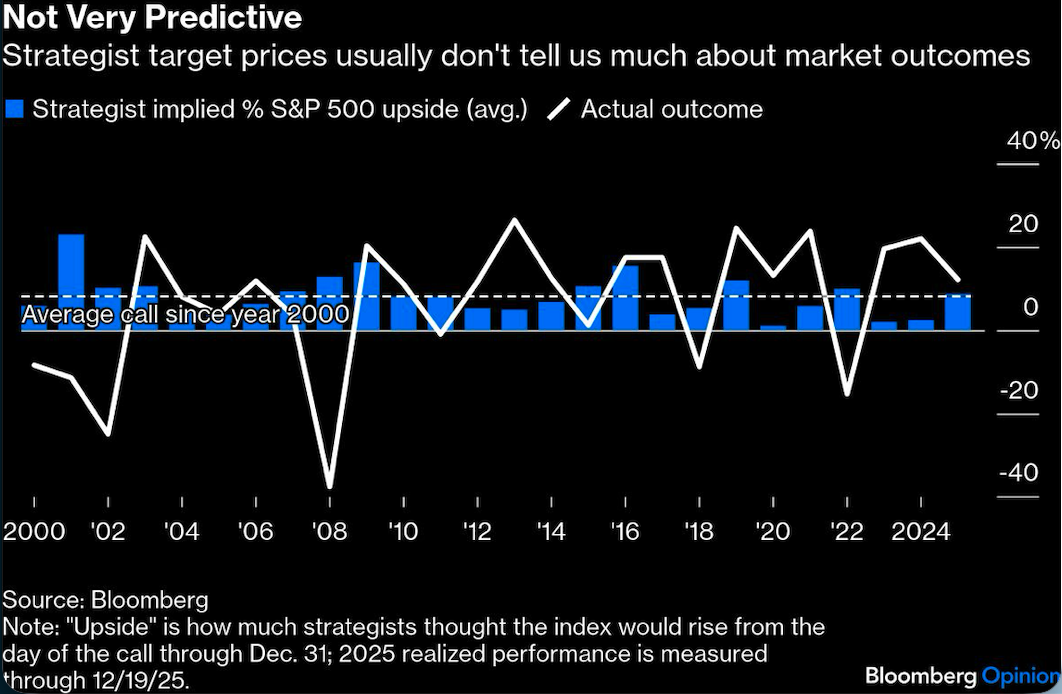

It’s crystal ball season again on Wall Street — the time when strategists attempt the impossible task of divining where the S&P 500 Index will end the next calendar year. This time around, strategists are projecting a relatively bullish 11% gain over the next 12 months, but basing one’s investment strategy on that assessment is roughly as helpful as consulting a fortune cookie, as my annual update of the strategist scorecard shows.

With valuations already elevated, it’s imperative that investors avoid hubris and complacency.

To be fair, strategists are coming off a year that was decidedly less terrible than usual. At this time last year, the average strategist projected the S&P 500 would end 2025 at 6,614 (a gain of 9% from the forecast date). In reality, the index is poised to best that mark by about 3 percentage points — a very acceptable margin in the grand scheme of things. Prior to that, the strategist consensus had been off by double digits for eight straight years. It’s possible that the crystal balls are getting clearer in the third year of a bull market, but the more likely explanation is that strategists were simply due for a lucky break.

The abysmal track record points to two hard realities about this bizarre Wall Street tradition. First, we’re asking strategists to do the impossible. In a market shaped by unknowable global forces (wars, trade conflicts, etc.) and great innovations (artificial intelligence, miracle weight loss drugs, etc.), it’s simply not credible for anyone to know where the index will land in 12 months to the exact index point. It would take tremendous skill and a great deal of luck to even guess where earnings are going in that period, but the mercurial nature of market sentiment complicates the exercise even further.

Second, today’s market has become so top heavy that some five stocks now drive around half of the index’s returns. Building a viable model demands clear assumptions about the particular earnings trajectories of companies such as Nvidia Corp., Apple Inc., Alphabet Inc., Microsoft Corp. and Broadcom Inc. That kind of analysis is not the core competency of macro-level market strategists.

So what can we make of the setup for 2026?

It’s a year with an extraordinary range of potential outcomes, and the upside implied by strategists doesn’t come close to doing justice to the nuance and uncertainty. Even the roughly 16% difference between the low (7,000) and high (8,100) estimates in Bloomberg’s main strategist survey seems far too narrow and reflective of dangerous complacency. The high-low gap was the narrowest in data reviewed since at least 2018, though the survey doesn’t include BCA Research Chief Global Strategist Peter Berezin, who is — as best I can tell — this year’s biggest bear.

The bearish outlook starts with the simple observation that the S&P 500 Shiller P/E multiple is at its highest level since the dot-com bubble, sustained by widespread enthusiasm for AI.

BCA’s Berezin, who has an S&P target of 5,280, projects that an “AI reality check” could send stocks tumbling and subsequently tip the US into a recession. After all, this economy has been buoyed by AI capital expenditures, on the one hand, and the “wealth effect” from a hot stock market on the other. Adding to the economy’s inherent vulnerabilities, Berezin notes that the labor market is already showing cracks, and the whole edifice could come tumbling down if economic actors begin to question the AI narrative.

Berezin, one of our most writerly strategists, penned this year’s outlook (once again) as a dispatch from a year in the future. Here’s how he put it (emphasis mine):

The 2001 recession was more the result of a stock market crash than the cause of one. The economic downturn that began towards the end of 2026 followed the same script. Falling stock prices caused the wealth effect to go into reverse...

To be clear, Berezin was also the market’s most bearish prognosticator in 2025, and it didn’t work out for him. He incorrectly thought that the US would enter a recession sparked perhaps by Donald Trump’s trade policies or, perhaps, a “bond market riot” driven by fiscal deficit concerns. And while those were important drivers of short-term market volatility, they failed to knock the market or the economy off course. Still, I admire Berezin’s chutzpah and am glad someone’s out there highlighting the downside risks.

At the other extreme, the bullish path for the market depends on continuity. The S&P 500 is on pace for about 12% growth in earnings per share this year, and it would only take an extension of the existing trend for the index to deliver double-digit returns in 2026 as well. Fiscal stimulus from Republicans’ tax bill could lead to a slight reacceleration in economic growth next year, and the profits from the AI data center boom could spread further into non-tech sectors such as industrials.

Here’s how Oppenheimer Asset Management Chief Investment Strategist John Stoltzfus justifies his S&P 500 target of 8,100, the highest in Bloomberg’s survey (emphasis mine):

At the core of what lies ahead for our 2026 target price to be achieved lies monetary policy, fiscal policy and the continuing progress of innovation and corporate earnings growth all of which have been supportive of stock prices and are key to growing earnings and revenues in the year ahead.

Stoltzfus has been correctly bullish for the past three years, and it would be easy to lean on him as a strategist with a “hot hand.” But then again, his 2022 target price ended up being 39% too optimistic when stocks slid into a bear market — the worst miss of that particular year.

In any case, the bullish Wall Street consensus belies an outlook with a great number of potential landmines, and complacency is the single greatest risk. Being in the consensus is easy: When you’re right, you can take all the credit; when you’re wrong, you can argue that everyone else was wrong as well. Sticking your neck out can get you fired in this business.

If the consensus is right, 2026 would be a boring year, and this simply doesn’t feel like a setup for boredom. And that’s why I wouldn’t rule out the possibility that this may end up being a Berezin kind of year.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin