Investors were rationally exuberant in 2025. US consumers remained remarkably resilient, keeping the world's largest economy out of recession. The tariff blizzard waxed and waned, eventually settling at levies still compatible with maintaining global growth, albeit at an anemic level. Central banks around the world eased monetary conditions, helping to slow an increase of government bond yields amid increased sovereign debt supply. The value of global equities set a fresh record. The coming year, though, looks less positive.

Artificial intelligence is the known unknown. It may spark a productivity revolution for its users; it could sink its creators under unsustainable debt loads, with the increasingly incestuous financial tangle between chip makers, data centers and AI model makers setting up a potentially disastrous domino effect in equities and credit. Cheerleaders argue it’s akin to building a transport network for ideas, but as historian Eric Hobsbawm wrote about the explosion of railway projects in The Age of Revolution, his study of 1789 to 1848: “Most yielded quite modest profits, and many none at all.” While we’re not ready to turn bearish on markets, bullishness is becoming an increasingly low-conviction stance.

A Tale of Two Kevins

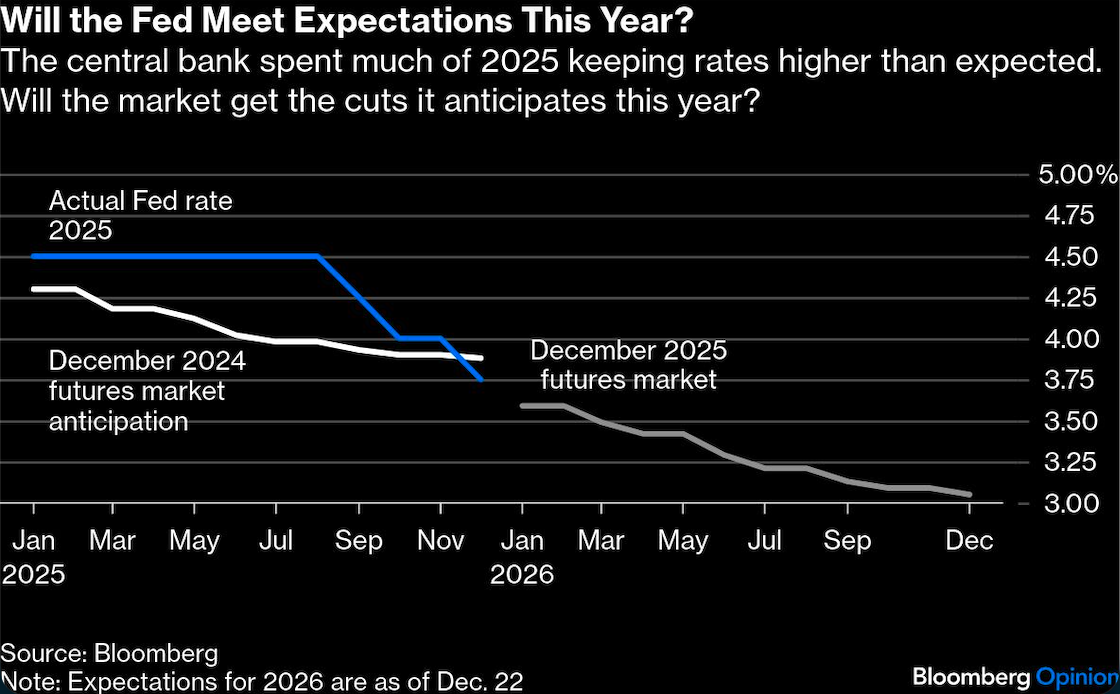

The smart money is betting that Donald Trump will choose either former Federal Reserve governor Kevin Warsh or Kevin Hassett, head of the president’s National Economic Council, to replace Jerome Powell as Fed chief. Either is expected to have a more, shall we say, accommodating response to Trump’s demands for lower borrowing costs. That doesn’t necessarily mean the rest of the voting members will agree that inflation is vanquished and the labor market needs more economic stimulus.

As the chart above shows, the futures market is anticipating at least two, possibly three, cuts to the Fed’s benchmark interest rate this year, which would take it to 3%. The Fed said last month it sees just one reduction. Data disruptions triggered by the US government shutdown mean traders and policymakers aren’t just looking in the rearview statistical mirror — it’s misted over. If further monetary easing in 2026 is deemed to be politically motivated rather than economically justified, looser conditions may spell trouble for markets.

Stocks Are Loved to the Tune of $151,418,820,254,310

At more than $150 trillion, the global stock market has increased by nearly 50% in the past five years. It’s tough to find anyone willing to bet against equities putting in another positive performance this year. It’s similarly hard to shrug off the uneasy feeling that market concentration poses a danger, especially if the AI bandwagon threatens to run out of road. The top seven US stocks, led by Nvidia Corp. with a market value of almost $4.6 trillion, make up a third of the S&P 500, compared with just 20% three years ago.

The consensus among Wall Street soothsayers is for the S&P 500 to add about 11% this year, which would mark a fourth consecutive annual double-digit gain for the benchmark index, with European stocks also expected to extend 2025’s 15% gains. JPMorgan Chase & Co. strategists are predicting earnings growth of 10% to 15% for US companies this year, which should help sustain equities. But if AI fails to deliver on its transformative promises — or investors start to balk at the cost of building the necessary infrastructure — we may see a repeat of the dotcom collapse of a quarter of a century ago, this time with trillions rather than mere billions at stake.

Consulting an Oracle About Hedging AI Risk

Oracle Corp.’s credit default swaps have become the barometer for how traders are hedging risk from the borrowing surge for AI projects. Oracle's creditworthiness is in the spotlight due to its central role in interconnected AI deals. Its borrowing rose more than 10 times last year, versus a mere tripling for its peers. Its long-term debt has risen 40% to $130 billion but it’s also disclosed $250 billion in off balance-sheet lease commitments, compared with a market capitalization of $570 billion. Its relatively low BBB credit rating compared with other hyperscalers such as Meta Platforms Inc., Amazon.com Inc. or Alphabet Inc. means Oracle would find it harder to weather a downturn.

More than $100 billion of AI-specific investment-grade bonds were sold in 2025, with even more expected this year. As much as $1.5 trillion of high-grade bonds for AI-related investments could be raised over the rest of this decade, according to figures compiled by JPMorgan, in addition to leveraged loans and high-yield debt. AI was funded initially through cash flow or equity capital, but its astronomically expensive future will clearly be underwritten in the debt markets. Gulp.

Japan Could Be The Big Worry For 2026

Are the wheels coming off the Bank of Japan’s yield-control experiment? This could have global repercussions if liquidity dries up across financial markets. The yen carry trade, where foreign investors borrow cheaply in the Japanese currency to leverage speculation elsewhere (e.g. US tech stocks), is a key cross-market lubricant.

For now, it’s just about manageable, as most foreign borrowing is in short-term yen tenors where yields are still below 1%. The BOJ raised official rates in December to 0.75%, but it’s moving very carefully. Its inflation-fighting work is helped to some degree by longer-term yields rising. It’s slowly closing the big gap to other foreign central banks’ rates, which should underpin the yen’s value. This is as much about Japanese investors not stepping up to the plate at home, despite 10-year yields nearly doubling last year, but maintaining their sizable foreign bond exposure. The air in the yen carry trade is being let out carefully. Still, Japanese government bonds are definitely a corner of the fixed-income universe to watch closely this year.

Credit Where It’s Due

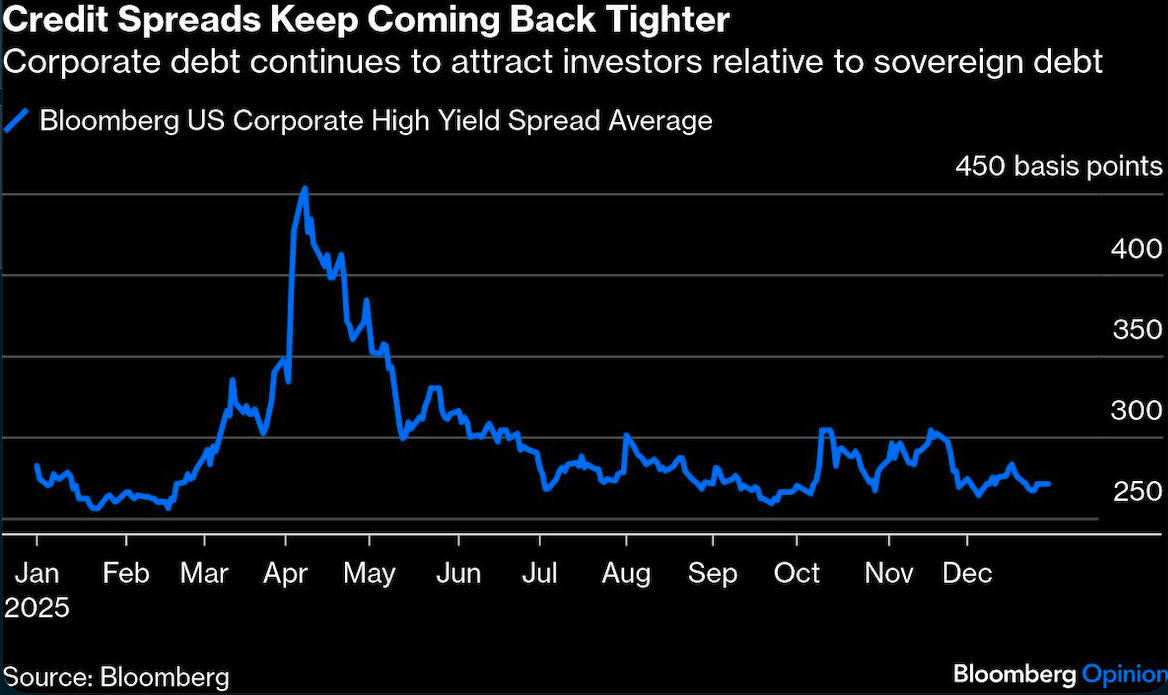

The story of 2025 was that whenever credit spreads blew out, it didn’t take long for fund managers to wade back in. So why are investors so keen to own corporate bonds at such narrow premiums?

Ever increasing sovereign borrowing means corporate debt is perceived to be relatively less risky. Rising stock prices imbue warm feelings that the debt of successful companies is also attractive. Fixed-income credit funds like to take only carefully controlled risk. It’s about return of capital rather than maximizing the return on capital. It explains why many bond managers are happily overweight credit, enjoying the (modest) yield premium over Treasuries. This helps them outperform their underlying benchmarks, while also benefiting if central bank rates are cut further and underlying government yields fall. As long as stocks stay strong, the tighter trend in credit spreads should persist, despite corporate bonds appearing expensive.

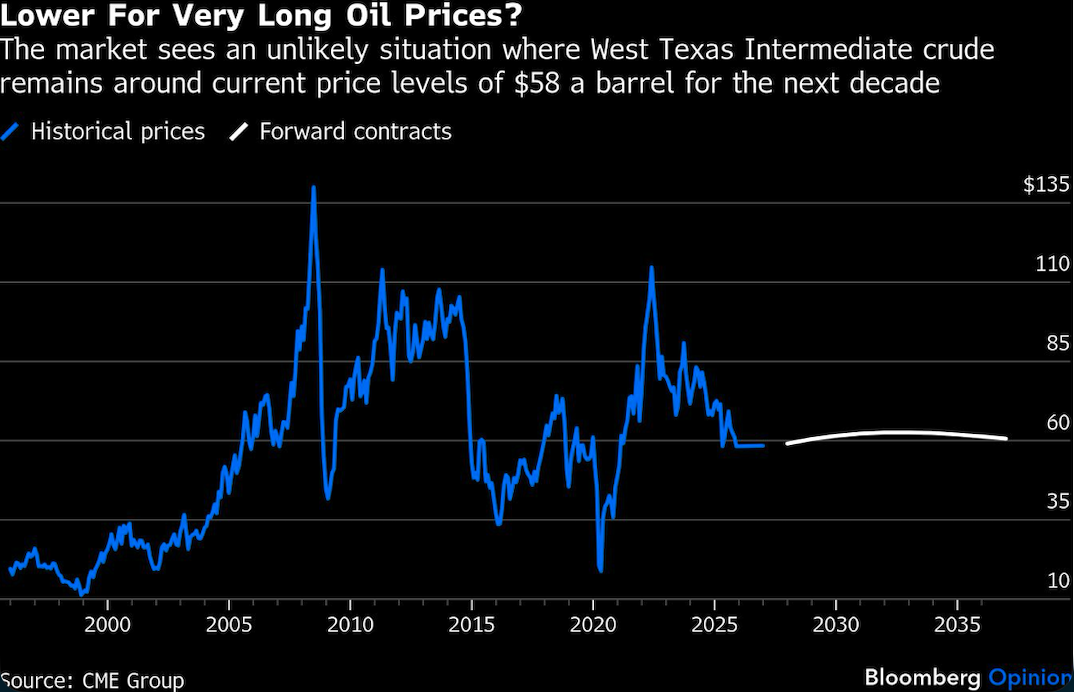

“The World Is Awash With Oil and Prices Are Poised to Keep Falling”

That’s the title of a Bloomberg News Big Take article published last month. There's a bit of a disconnect in oil prices, in that forward prices are so remarkably flat out to 2030, hugging closely to the current $58 West Texas Intermediate level. As our colleague Javier Blas has written, oil never stays in balance for this long.

Global economic growth is expected to slow this year to 2.9% from 3.2% in 2025, according to OECD forecasts. Nonetheless, oil demand is forecast to rise by nearly 1 million barrels a day. What’s keeping a lid on prices is that supply is growing even faster, with pandemic-delayed projects now coming onstream. After 2027 this could hit a plateau and alter the price dynamics — but until then, energy prices look like heading lower.

Bitcoin’s Wild Mood Swings Are Exhausting

Bitcoin is ending the year worth about the same as it was at the start: around $90,000. But the ride has been wild even by crypto’s exaggerated standards, with the flagship digital currency swinging by 70% between April’s low below $75,000 and October’s record high of $126,000.

So here’s our 100% conviction trade for what happens next to the token: ¯\_(ツ)_/¯

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.