From an AI-fueled stock rally to China shaking off US tariff threats and earning a record trade surplus, 2025 was full of economic marvels. Don’t expect debates over innovation and economic disruptions to disappear in 2026. There are four surprising-but-not-improbable developments on my watch list that you might want to consider.

OpenAI Bonds

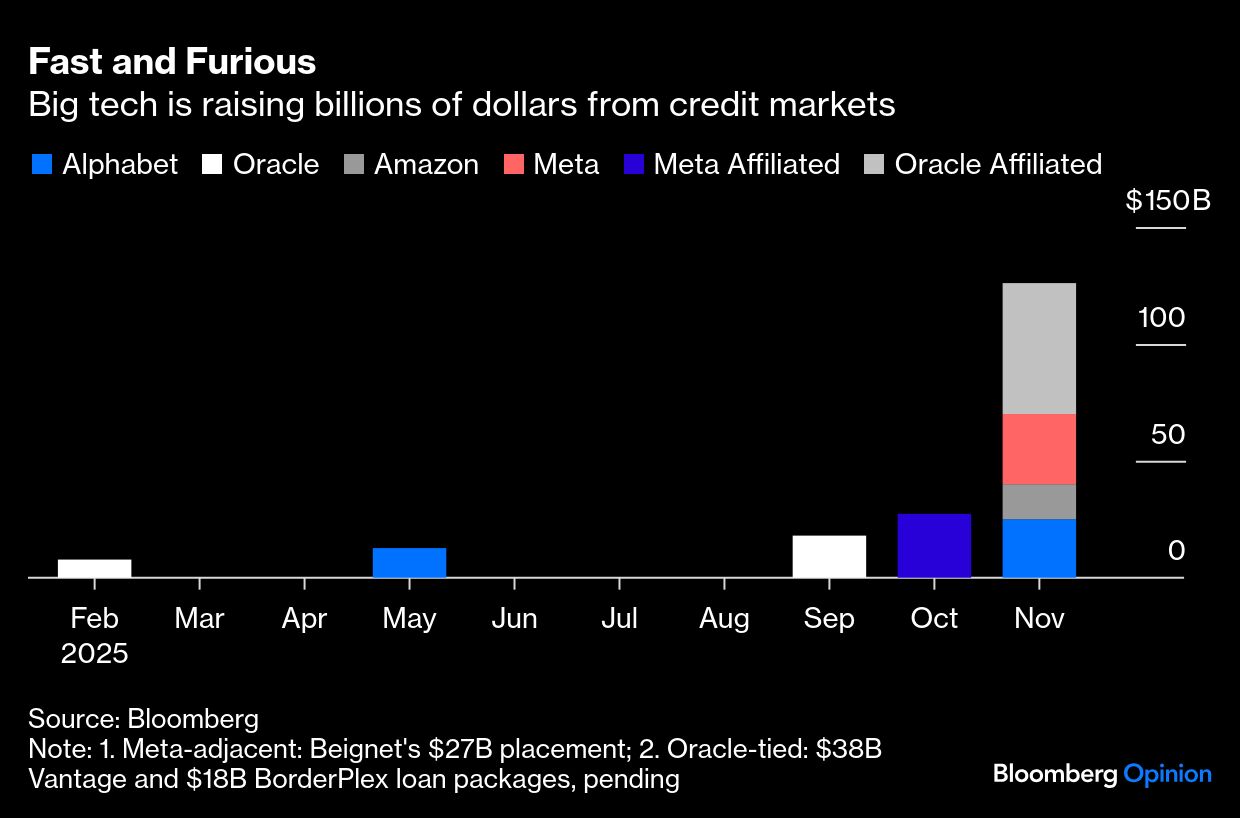

If WeWork Cos. was able to issue corporate bonds before going public, why can’t OpenAI Inc., a unicorn behemoth valued at $500 billion?

Not planning to go public until 2026 at the earliest, Sam Altman’s startup nonetheless has a lot of financing needs. It’s expected to burn through $17 billion of cash, followed by $35 billion and $45 billion, respectively, in the two years after.

To no one’s surprise, OpenAI is in fundraising mode again. It’s reportedly seeking to raise $100 billion, at as much as $830 billion valuation. The company plans to complete this round by the first quarter at the earliest.

Japan’s SoftBank Group Corp. has been bankrolling OpenAI, investing $30 billion in 2025. But will cash-strapped founder Masayoshi Son find the money to lead future funding rounds, or accept a lower valuation if another more value-oriented anchor investor comes in? Markets have grown concerned with OpenAI’s earnings potential.

If venture capital is running out, OpenAI might have to turn to the bond market, following in the footsteps of other hyperscalers. After all, Altman can’t indefinitely rely on his partners (yes, I am looking at you, Oracle Corp.!) to raise debt. It’s time OpenAI levers up its balance sheet as well.

Labubu Unchained

No more scalpers! Imagine walking into any Pop Mart International Group Ltd. store and being able to buy a toothy Labubu toy whenever you feel like it. That would be great news for fans and a real test for the Chinese toymaker’s brand resilience.

Hong Kong-listed Pop Mart is one of the hottest and most debated stocks. Advocates see it as a major beneficiary of a lasting consumer trend, whereby young people are willing to go over their budgets and buy little treats. Meanwhile, Pop Mart has done a good job churning out eye-catching series on a regular basis. Critics, however, complain that the company is relying on scarcity to sell its products. Now that online interest in Labubu has peaked, the best days are over, they argue.

To prove naysayers wrong, stock up the shelves and show your true worth, Pop Mart! Let’s find out whether Labubu is a phase or a permanent fixation.

Hong Kong Tycoons’ New Deal

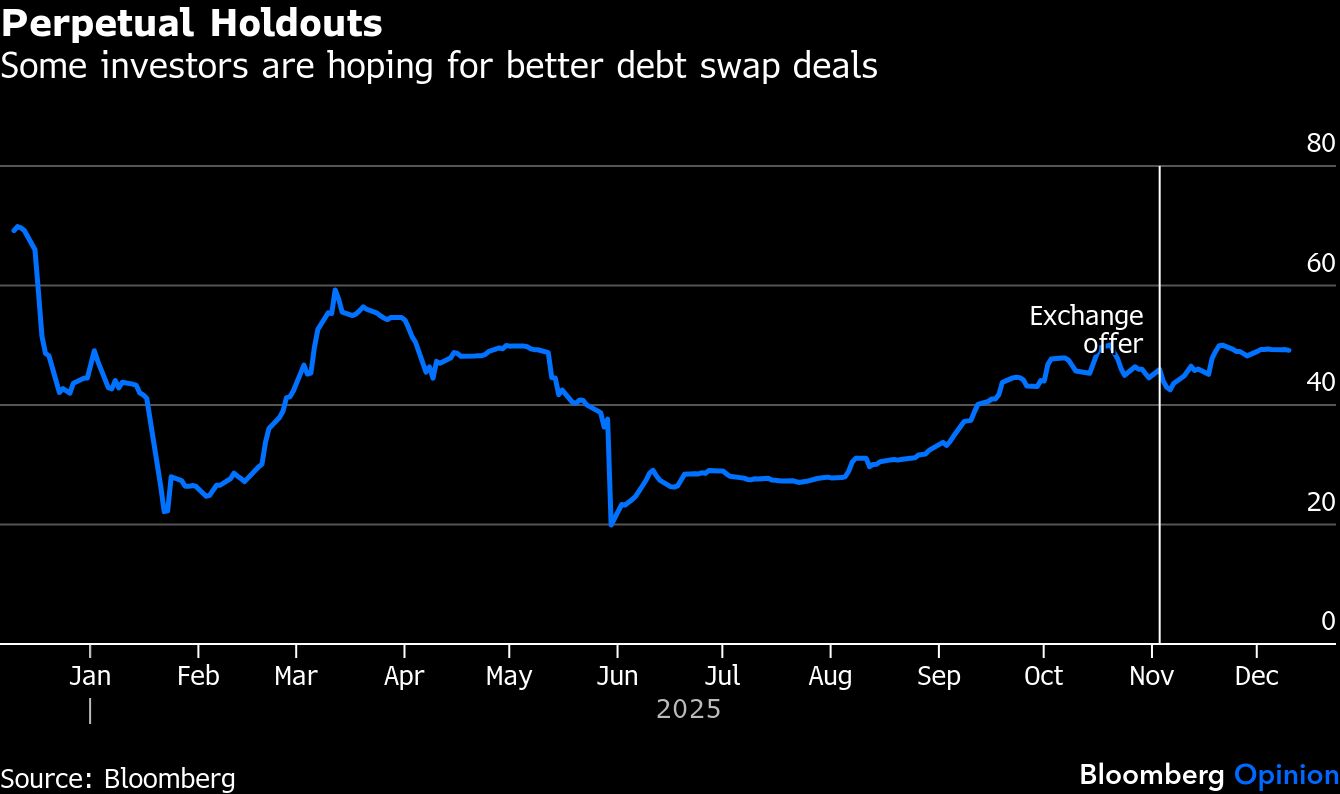

Some of New World Development Co.’s perpetual bondholders are hoping for an equity injection led by Henry Cheng, its billionaire chairman and family patriarch. The real estate developer, one of Hong Kong’s most iconic companies, got itself into financial distress after a debt-fueled expansion into luxury retail.

The tycoon’s flagship property firm launched a debt swap that included haircuts of as much as 50% in November, mostly targeted at the perpetual bond investors. But it has received only 72% of the maximum proposed, a sign that some are hoping for better offers.

For months, there have been market rumors that the Chengs would bring in new equity partners to revive New World, now that Hong Kong’s real estate market is starting to see green shoots. The developer can’t hand out dividends to new shareholders unless it has paid all accrued interest on its perpetuals. This dynamic gives creditors some bargaining power if the family wants to close an equity deal, the thinking goes.

Not so fast. Take a look at the Chengs’ track record — they don’t throw good money after bad. They have not offered any shareholder loans, as the billionaire Lee family did for its listed property firm Henderson Land Development Co., or Shenzhen Metro Group for China Vanke Co. Granted, in 2023, the family bought New World’s 61% equity interest in NWS Holdings Ltd., a separately listed subsidiary, for HK$18 billion. But that was a sweet transaction for the family office in that the construction firm pays handsome dividends.

Remember, Hong Kong tycoons are wealthy for a reason. They are world-class financial engineers and play their cards well. Don’t be too naive.

Private Credit Goes Dark

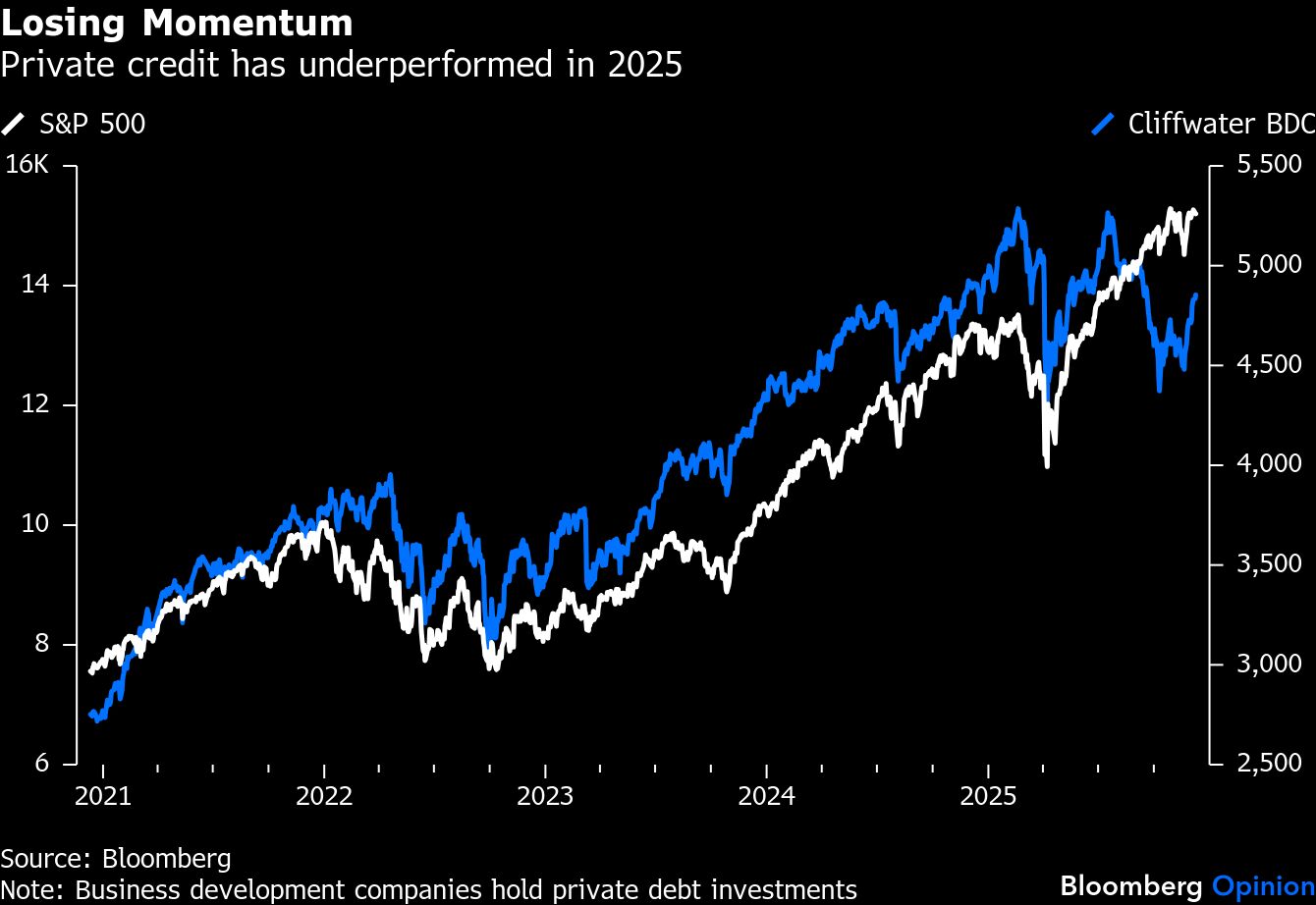

There have been a lot of discussions over whether private credit poses systemic risks and may balloon to trigger the next financial crisis. Before going alarmist, it’s possible that the industry has seen its best days and may shrink on its own.

First, what’s the point of raising trillions of dollars if fund managers struggle to deploy capital? Public credit markets are now competing aggressively for deals: The syndicated loan market has reopened for junk-rated borrowers, and banks are once again arranging financing for the biggest leveraged buyouts as well as mega AI data-center projects.

Second, investors are starting to realize that private credit is nothing like private equity or venture capital. On the one hand, risk-taking is not rewarded with equity gains, where the sky is the limit. On the other, there’s little room for error as loan margins have fallen. One bad investment can sour the performance of an entire fund, as the bankruptcy from First Brands Corp., an auto-parts supplier, has shown. So why bother?

That’s all, folks! As always, thank you for your support and I love to hear from you. Happy trading and investing.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Shuli Ren