President Donald Trump has promised to address housing-market dysfunction and a lack of affordability in 2026. While we don’t know what the White House has planned, previous talk has included a (much criticized) suggestion for 50-year mortgages and exhortations to builders to do their duty and build more housing.

It’s certainly time for the federal government to consider ways of improving market functioning after three years of low existing-home sales, fairly modest progress on affordability, and homebuilders accepting elevated levels of buyer incentives and, in many cases, low profit margins to sell homes. Fortunately, there’s targeted fiscal actions, available at a limited cost to taxpayers, that the White House can consider to speed up the normalization in conditions that’s sluggishly underway.

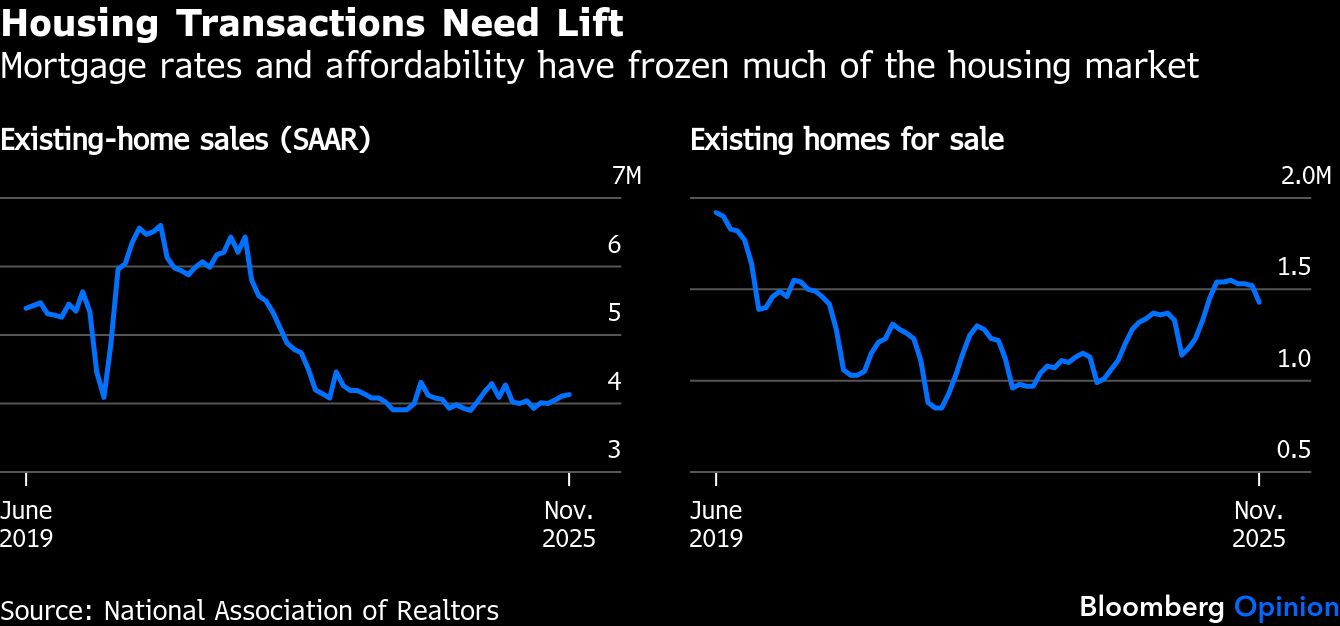

It starts by addressing the main bottleneck on the supply side in much of the country — homeowners who want to sell but can’t because they are unwilling or unable to give up a low mortgage rate, or because they can’t or won’t cut the asking price on a property that’s languishing on the market.

At a national level, there is no shortage of homes for sale. Active housing inventory in the US is projected to climb back to 2017 levels this year, according to Mike Simonsen, chief economist at Compass Inc., the largest residential real estate brokerage in the country. The challenge has been converting listings into transactions, which is where policy can help.

About half of owners with home loans have mortgage rates below 4%, down from 60% in early 2022, according to Logan Mohtashami of HousingWire. It’s difficult financially to give up that rate for a new mortgage with a rate above 6%.

The housing market last dealt with this dynamic in the early 1980s, when the Federal Reserve was rapidly raising interest rates to crush inflation. At the time, it was easier for homeowners to transfer their existing mortgages with low rates to buyers. Congress significantly narrowed the eligibility for such transfers in late 1982. Assuming a seller’s low-rate mortgage is pretty hard now even when it’s allowed.

Expanding the use of assumable mortgages to tackle today’s problems would be messy and fraught with challenges. Holders of mortgage-backed securities may protest, lenders would increase mortgage rates overall to account for the new risks, and questions would arise about how to treat buyers with lower credit scores than the original owners. Instead, the government could look to incent both sales and purchases.

For sellers, it could use tax credits to ease the pain of giving up a low mortgage rate. For example, homeowners could be offered a credit up to $20,000 for two years, based on the difference between the mortgage rate on their new home and the one they sold. A household whose mortgage payment jumps by $8,000 per year, for example, would receive a $16,000 credit over two years. After that, the homeowner would be on their own but maybe mortgage rates have fallen by then or their income risen enough to handle a higher rate.

To address affordability, the government could offer a time-limited mortgage rate buydown for first-time buyers of new and existing homes, similar to what homebuilders are already doing. Buyers would still have to qualify for a regular mortgage rate, but the government would buy down the year one rate by 2 percentage points and the year two rate by 1 percentage point. By year three, these homeowners too would be on their own.

The total cost of both programs would be limited. About $60 billion for the tax credits if four million sellers used them over 2026 and 2027 at an average take-up rate of $15,000. And $36 billion for the first-time homebuyer sop if these are again used by two million buyers a year over those years with an average mortgage balance of $300,000.

The boost to housing would likely come more on the transactions side than on pricing. Unlike in 2022 and 2023, there are plenty of homes to buy nationwide, and even in supply-constrained regions, inventory is likely to rise in 2026. For those who benefit from the program, the boost to their finances would be short term; when the subsidies roll off, they will have to cut consumption to account for the higher housing costs.

Policymakers mulling how to address challenges in the housing market are fortunate in that their efforts will get a tailwind from the continued rise in inventory, which is already putting some pressure on prices. But waiting for the market to adjust has costs including reduced mobility for buyers and sellers alike, and delayed family formation for those who’d like to buy but struggle to make the finances work.

We now have enough inventory and motivated sellers for the market to thaw in 2026. It would benefit all Americans if policymakers could help speed the process along.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Conor Sen