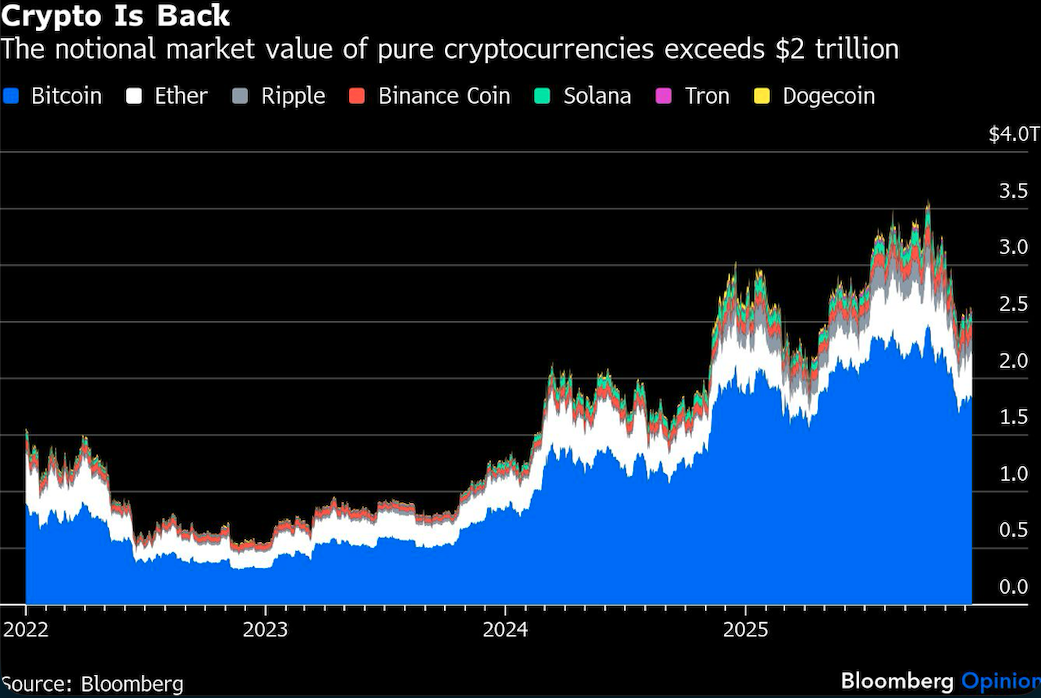

Dogecoin isn’t an asset in any reasonable sense. It represents no investment in, or claim upon, real economic activity. The speculation that has pushed its notional market capitalization beyond $20 billion — and that of all pure cryptocurrencies, including Bitcoin, to more than $2 trillion — is a social phenomenon that could end as suddenly as it arose.

Lending actual dollars against such things would be hazardous at best — and at worst provide the leverage needed to turn the next market crash into a full-blown crisis. Yet if new proposals from the finance industry are adopted, that’s exactly what the world’s largest banks will soon be able to do.

No doubt, crypto holds promise. Applied to government-issued currencies or other assets, the underlying distributed-ledger technology has the potential to vastly improve cross-border payments and reduce the risk of all kinds of financial transactions. Yet this bears little relation to trading in digital tokens, including myriad “memecoins” dedicated to the likes of Pepe the Frog or the fart. These serve mostly as venues for gambling, or worse.

Until recently, regulators sought to strike a sensible balance, making room for the useful stuff while warning banks away from the rest. This was reflected in a standard they set at their global forum, the Basel Committee on Banking Supervision. It established a separate category for tokens representing genuine assets such as dollars or stocks: If they were reliably redeemable and recorded on ledgers run by accountable companies, they’d be treated the same as the assets. Beyond that, any crypto exposure had to be funded completely with loss-absorbing equity and limited to a tiny percentage of a bank’s total capital.

The approach proved to be a great success. In 2022, when crypto prices crashed and multiple intermediaries including the FTX exchange collapsed, banks had almost no exposure. Losses from an event that could’ve destabilized the financial system were contained to the people who had chosen to be involved.

Times have changed. Crypto is back. The US president has his own memecoin. Regulators are much more sympathetic to the industry, which wants to tap the trillions of dollars in largely taxpayer-subsidized funding that the banking system has to offer. Sensing the zeitgeist, finance and crypto trade groups have joined forces, pushing the Basel committee to revise a standard that some of its largest members, notably the US, find unduly restrictive. Its chairman has suggested he’s amenable.

Some reforms might make sense. Tokenized assets — such as stablecoins representing government-issued currencies — often reside on public ledgers that allow anyone with the necessary resources to validate transactions. The Basel standard views such “permissionless” platforms as universally too vulnerable to attacks and money laundering to qualify for preferential treatment. As these assets evolve, a more nuanced approach might be appropriate.

The trade groups’ proposals, however, go much further. They would eliminate limits and reduce capital requirements on lending against a broad range of pure cryptocurrencies. These, they argue, should be treated more like major stocks or currency pairs, to the extent that they have similar liquidity and volatility profiles. Yet this ignores the crucial difference between assets associated with real-world cash flows and digital markers backed by nothing. In practice, it would mean that your deposits could be loaned to a hedge fund making a leveraged bet on, say, Dogecoin — a token created as a joke, whose price is completely divorced from any notion of fundamental value.

In no way would bank leverage further crypto’s best and highest uses. On the contrary, it would needlessly introduce a new threat to the stability of the entire financial system — and thus to millions of people who have nothing to do with crypto. Why let that happen?

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by The Editors