The health-care corner of the US equity market has traditionally been viewed as defensive, thanks to steady growth and healthy dividend yields among the industry’s stalwarts. That narrative is changing.

Following years of underperformance relative to the broader market, health care staged a turnaround last quarter, posting the best performance among the 11 major industry groups in the S&P 500 Index.

The sharp about face followed tariff deals with the Trump administration, a flurry of acquisitions and prospects for next-generation obesity drugs. Meanwhile, concerns over high-flying tech stocks made downtrodden sectors like health care look more attractive for those looking for growth opportunities elsewhere. With this backdrop still in place, many investment pros are banking on the momentum to continue into 2026.

“There are many investors right now that are looking at technology and saying, ‘how much longer, how much further is it gonna go?’,” said Bob Lang, chief options analyst at Explosive Options.

Instead, Lang views health care as a “more offensive” play, as investors pile into names where they see value and better returns. “I think people are looking for yield, they’re looking for better-performing stocks and the health-care sector is being one of them,” he added.

But despite the new growth potential for the sector, the year 2026 is set to be — yet again — a stock picker’s year for health-care stocks.

“There are certain segments inside of health care you want to be very careful about, but there’s also some really good bright spots,” said Brian Mulberry, client portfolio manager at Zacks Investment Management. “Knowing how to pick and choose those particular companies that will be benefiting from new waves of regulations, that’s gonna be an important part of investing going into the new year.”

Here are the key themes to watch in 2026:

Obesity

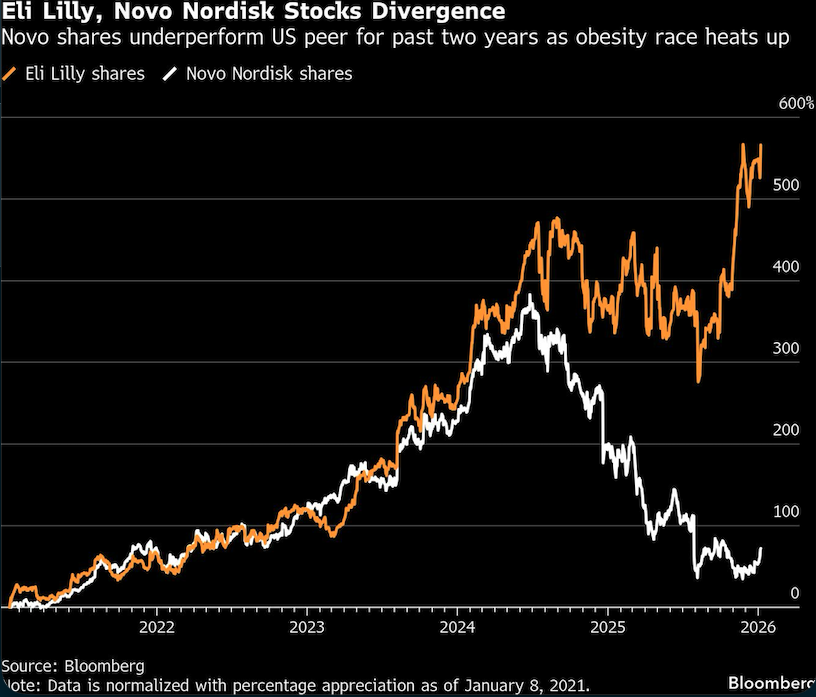

For the last three years, obesity has been one of the biggest themes in health care, and that trend is set to continue — this time with obesity pills acting as a major catalyst.

A US Food and Drug Administration decision on whether to approve Eli Lilly & Co.’s oral obesity medication is expected in early 2026. The decision will follow regulators’ approval of a rival obesity pill from Novo Nordisk A/S in late December. Overall, these approvals will open a new front in a weight-loss market that’s projected to reach $95 billion by the end of the decade, according to Goldman Sachs Group Inc.

In the meantime, obesity shots are expected to gain wider Medicare coverage starting in 2026 as part of a deal with the Trump administration.

“With the combination of continued supply growth, tremendous innovation, particularly with oral drugs and tapping into key markets such as Medicare and Medicaid, I think we will continue to see that excellent growth,” said Kevin Gade, portfolio manager at Bahl & Gaynor.

Drugmakers, including Lilly and Denmark’s Novo, are also developing new generations of GLP1s, a class of weight-loss drugs, seeking improvements in dosing frequency, efficacy, side effects and ease of use.

“GLP1s allows us to look at some of these pharma companies more like tech companies and get the type of growth estimates that we typically could not have in pharma companies,” said Mark Malek, chief investment officer at Sibert Financial.

Still, the pricing war between the two frontrunners of the obesity race remains an overhang. Both are seeking to gain an edge through deals with drug benefit managers, the firms that control drug benefits for Americans, discounts for cash-pay patients and direct-to-employer plans.

The race to offer cheaper weight-loss drugs could make the obesity trade “murky” in 2026, according to David Miller, co-founder and CIO at Catalyst Funds. “There’s certainly opportunities there, but it’s a much more difficult game to play.”

Mergers & Acquisitions

The burst of mergers in health care in the latter half of 2025, combined with expectations for lower borrowing costs from the Federal Reserve’s interest rate cuts, is fueling optimism about a sustained industry recovery.

Twenty-eight acquisitions of $1 billion or more were announced or completed in the year through Dec. 1 compared to 25 in all of 2024, according to data compiled by Bloomberg Intelligence analysts Michael Shah and Andrew Galler. Deal activity as measured by the value of transactions in the health-care sector for 2025 topped $103 billion versus $63 billion the previous year.

“For the first time, we can say we are realistically optimistic about 2026 and not just hopeful or cautious,” said Arda Ural, head of EY Americas life sciences.

With large pharmaceutical companies holding about $200 billion in cash and balance-sheet flexibility as of mid-December, deal momentum should persist as drugmakers look to plug revenue holes from top-selling drugs facing patent expiration.

A marquee event for the sector begins next week when investors convene in San Francisco for the annual JPMorgan Healthcare Conference — an occasion where industry deals are typically announced.

“Large cap pharma companies have the need to replace their pipelines,” said Terence McManus, a health-care portfolio manager at Bellevue Asset Management. “They have the capital to do it, and they now have a more stable regulatory environment, so I think that will continue to be a theme.”

Another form of deal making, initial public offerings, also showed a resurgence, notably in biotech firms. These new entrants on US exchanges raised $11 billion in 2025, a 61% increase from 2024, according to data compiled by Bloomberg.

Investor appetite for this riskier segment of the health-care market was evident as the Nasdaq Biotechnology Index climbed more than 50% from a low in April to hit a record high in December.

Managed Care

Growth prospects are less certain for health insurers.

Insurers focused on the private Medicare market initially anticipated benefiting from President Donald Trump’s re-election on the view that his administration would boost government payments to firms offering private versions of the health program for seniors.

Instead, insurers faced rising costs across Medicare and plans offered through the Affordable Care Act, also known as Obamacare. Names including Molina Healthcare Inc., UnitedHealth Group Inc. and Centene Corp. were particularly big losers, dropping more than 30% in 2025.

On one hand, managed care is a short-cycle business, meaning the firms can reprice plans annually, after margins are squeezed. Some investors believe the worst may be over and that valuations already reflect the risks.

On the other hand, the expiration of Obamacare subsidies could prompt millions of Americans to drop coverage. That will hit revenue at the same time as younger, healthier people are seen opting out, leaving insurers with older, sicker patient pools and higher costs.

“Managed care still exhibits a deep value opportunity,” said Christopher Hart, a portfolio manager at Boston Partners, who remains cautious on the sector. “What’s going to get me interested in the managed-care side is better visibility of stabilization of profitability.”

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Angel Adegbesan, Avalon Pernell