The hottest corner of the stock market in 2025 remains scorching in the new year, but the relentless momentum has some Wall Street pros wondering if a reversal is coming.

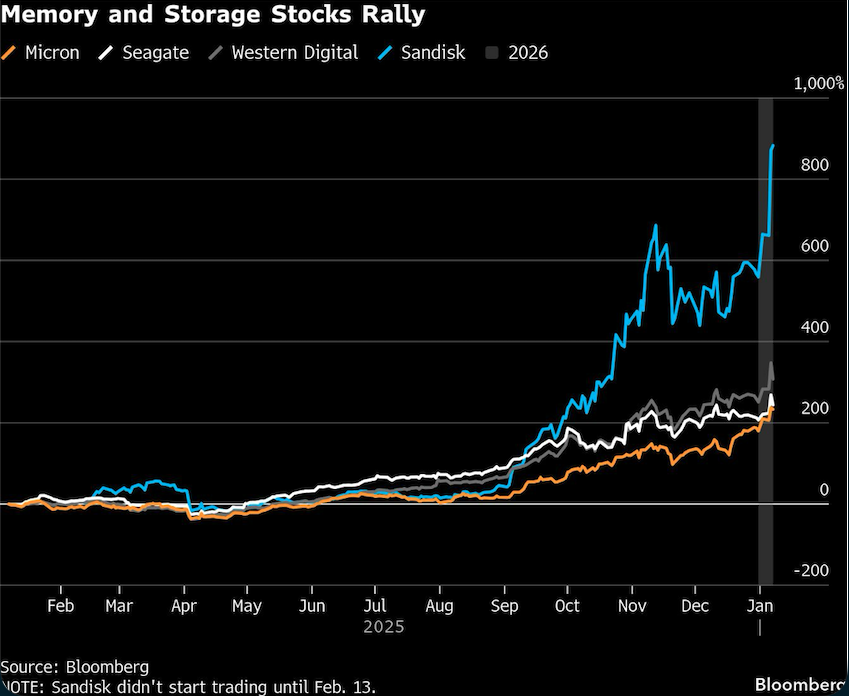

Memory and storage companies were the leading performers in the S&P 500 Index last year, as the massive amounts of cash being spent on building out AI infrastructure trickled down to some traditionally staid parts of the tech sector. The group, led by companies like Sandisk Corp., Western Digital Corp., Seagate Technology Holdings and Micron Technology Inc., remains at the top of the index in the early days of 2026.

Sandisk popped 16% on the first trading day of the year and then soared 28% on Tuesday after Nvidia Corp. Chief Executive Officer Jensen Huang highlighted the need for more memory and storage in the AI ecosystem. The stock rose 1.1% on Wednesday and is up 49% in the first trading sessions of this year. Meanwhile, Western Digital, Seagate and Micron have all posted double-digit percentage gains to start 2026, although all three stocks fell on Wednesday.

Just after the open Thursday, Sandisk shares were down 1.4%, while Seagate dropped 2.1%, Western Digital fell 2.6% and Micron retreated 1%.

Shares of Sandisk soared 559% in 2025 to lead the S&P 500, followed by Western Digital, Micron and Seagate to round out the index’s four leading gainers.

However, modeling the growth prospects for these companies “is very difficult to do when there’s a transformation technology evolving in real time,” said Jessica Noviskis, outsourced CIO portfolio strategist for Marquette Associates, which manages about $29 billion in OCIO assets. “There are probably retail investors who are desperate to not miss this rally, so they’re grasping at straws.”

The primary drivers behind the rallies in memory and storage stocks are the AI infrastructure spending boom and rising prices for components such as memory chips due to soaring demand. But many investors are wondering if the size of the gains is justified, especially amid growing questions about whether AI-related capital expenditures will continue at their current pace without signs of strong returns on the outlays.

“The recent strength makes sense optically given the AI data-center buildout narrative, but I’m increasingly concerned the market is extrapolating demand too far forward and underestimating the historical cyclicality and the risk of over-capacity and pricing pressure,” said Peter Andersen, who helps oversee $4.5 billion in assets as chief investment officer of Andersen Capital Management.

Such rallies may be difficult to sustain over the short term. The 14-day relative strength indexes for Sandisk and Micron, for example, are above the 70 level, which some technical strategists see as a sign that a stock is overbought.

Relative Bargains

The group tends to trade at lower valuations than other technology companies, and on the surface they still look like relative bargains. Micron trades at just 10 times estimated earnings, while Sandisk is around 20. Both Seagate and Western Digital are below 25, which is where the Nasdaq 100 Index sits. The Bloomberg Magnificent Seven Index trades at roughly 29 times expected earnings.

However, concerns about the durability of the factors driving the gains — AI spending and strong demand — has some professional investors shying away even if the stocks may seem inexpensive.

“If you agree with me that there’s an over-building of AI infrastructure, you should stay away,” Andersen said. “If one company comes out and says they’re slowing down their spending, that could open the floodgates for selling.”

Certainly, many Wall Street analysts remain optimistic that major AI spenders like Microsoft Corp., Amazon.com Inc., Alphabet Inc., and Meta Platforms Inc. will stick to their plans. The four tech giants outlined aggressive capex programs in their most recent results, suggesting the trend will persist at least through much of 2026. Micron’s earnings last month featured an upbeat outlook, sparking a sizable rally.

“As multi-modal AI becomes more prevalent, we expect significantly higher amounts of data to be created which should drive increased need for low-cost storage,” benefiting Seagate and Western Digital, Bank of America analyst Wamsi Mohan wrote in a Jan. 4 note. At the same time, “the need to store more data on edge devices and need to access data quickly can drive higher use of NAND storage,” which benefits Sandisk.

Similarly, Needham expects high-bandwidth memory — the kind of chip that Micron makes — will remain “the king of AI memory for another 5-10 years.” The firm upgraded Cohu Inc. as a related play, and is positive on Camtek Ltd, Onto Innovation Inc., and Kulicke & Soffa Industries Inc., all of which have charged out of the gate in 2026.

For investors, the question is which side of the risk fence you’re on, which is not a simple question. Marquette’s Noviskis, for instance, continues to be positive on the AI theme. But she’s also concerned that the size of the rallies is giving these companies a higher ledge to retreat from if the narrative starts to show cracks.

“It can be true that this story is real, and also true that some names have gotten ahead of their skis,” Noviskis said. “The problem is we don’t know which are which.”

Tech Chart of the Day

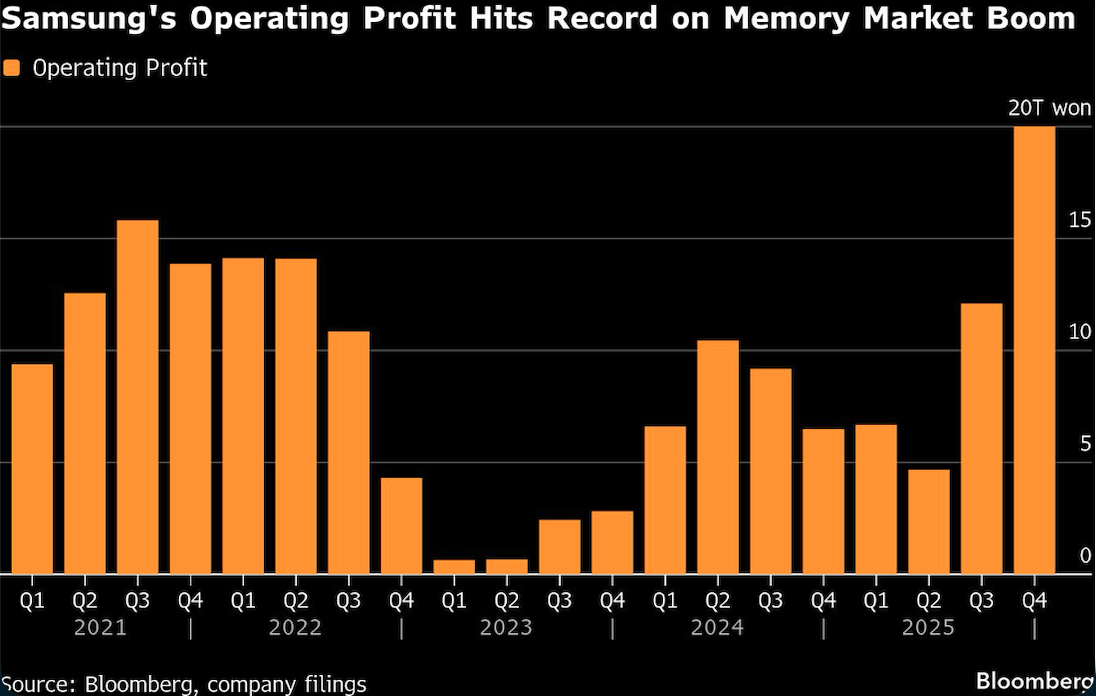

Samsung Electronics Co.’s quarterly profit more than tripled to a record high after global demand for AI servers sharply lifted memory chip prices. South Korea’s largest company reported a preliminary operating profit of 20 trillion won ($13.8 billion) in the three months through December, up 208% and beating the average analyst estimate.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Ryan Vlastelica