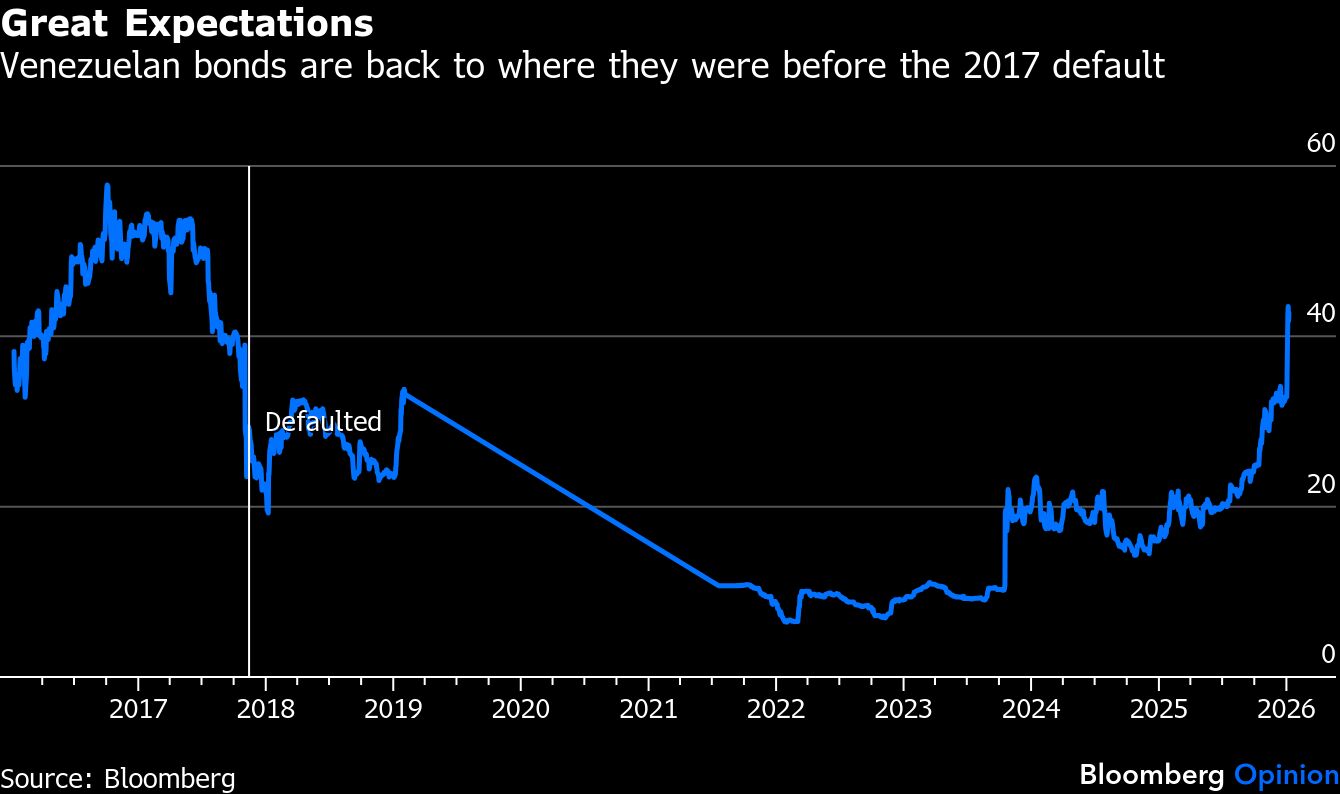

It’s been eight years since Venezuela stopped paying its debt. But traders are making a wager that the ouster of Nicolas Maduro will deliver windfalls to holders of the country’s $59 billion of bonds. Notes due in 2027 jumped as much as 29% this week, putting them back to where they were before the 2017 default.

The sharp price moves reflect investor optimism of a debt restructuring — not on the table till recently because of ongoing US sanctions that began during President Donald Trump’s first term. Recovery rates can also be decent, since Venezuela has the world’s largest proven crude oil reserves. Some commentators are seeing an energy super-cycle, and that crude will sooner or later join the rally of industrial metals such as uranium and copper, given the chronic underinvestment it shares with the others.

Despite its underground riches, however, Venezuela is not for the impatient or faint-hearted. Unless asset managers believe they are as tenacious as the legendary hedge fund manager Paul Singer, it’s better that they stay away. The billionaire has over the years relentlessly sued developing nations for sovereign debt repayments, including famously Argentina.

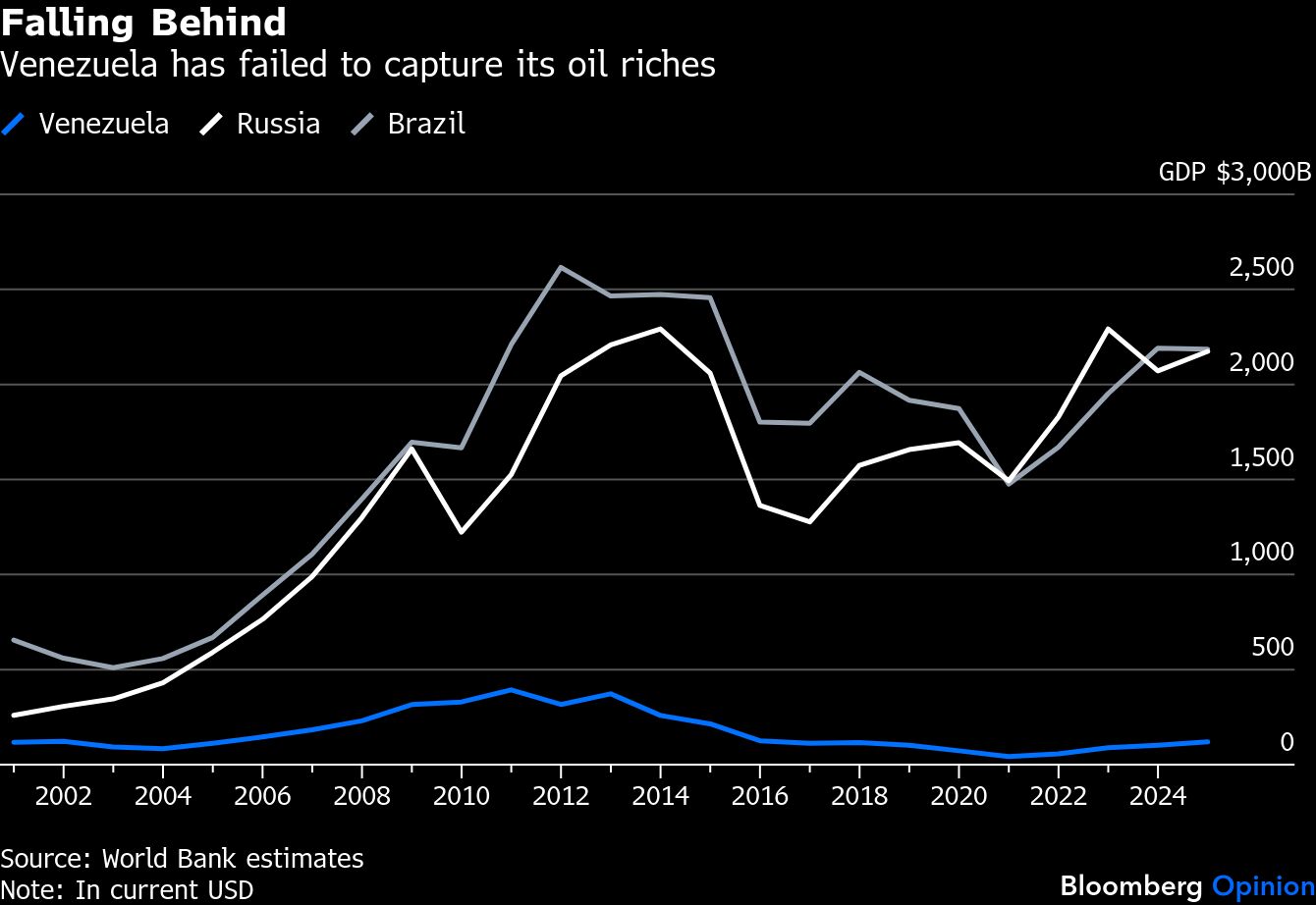

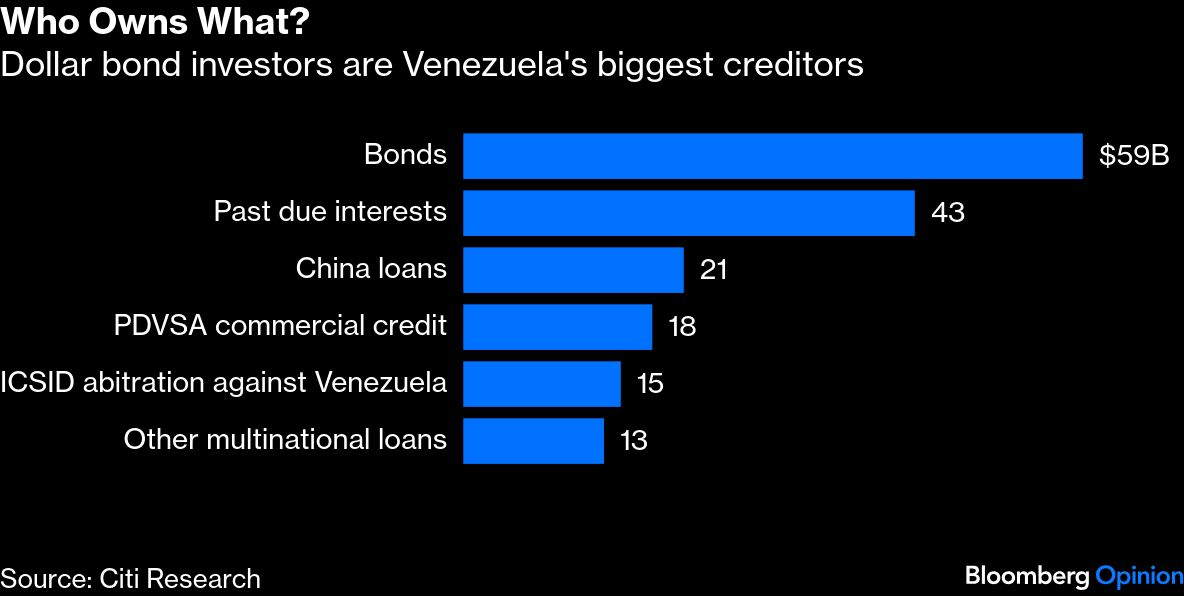

Dollar bond investors are Venezuela’s biggest creditors, data from Citi Research shows. The government and state-owned oil company Petroleos de Venezuela SA owe about $169 billion of external debt, including $59 billion unsecured notes outstanding and $43 billion past due interest payments. This pegs the country’s debt-to-GDP ratio at 173%, or roughly twice as much as the average 86% for sovereign states that have gone through meaningful debt cleanups. As a result, if Venezuela follows a similar exercise, its international creditors collectively will almost inevitably have to accept a 50% haircut.

But recovery rates can vary greatly, depending on who you are. Are creditors truly pari passu, a Latin word meaning “on equal footing” and used in finance to describe when creditors are treated equally? It was made famous by Singer’s legal tussle with Argentina, after the country defaulted in 2001. NML Capital, a unit of Elliott Management subsequently sued for enforcement of the pari passu clause with a novel argument that Argentina can’t service new bonds without paying the old first. Elliott won the case but the entire process spanned 15 years.