The billionaire Ellison family said this week that it will try to overhaul the board of Warner Bros Discovery Inc. unless the Hollywood studio engages with their $108 billion takeover bid. But winning support in a corporate fight won’t be easy as long as their offer contains holes.

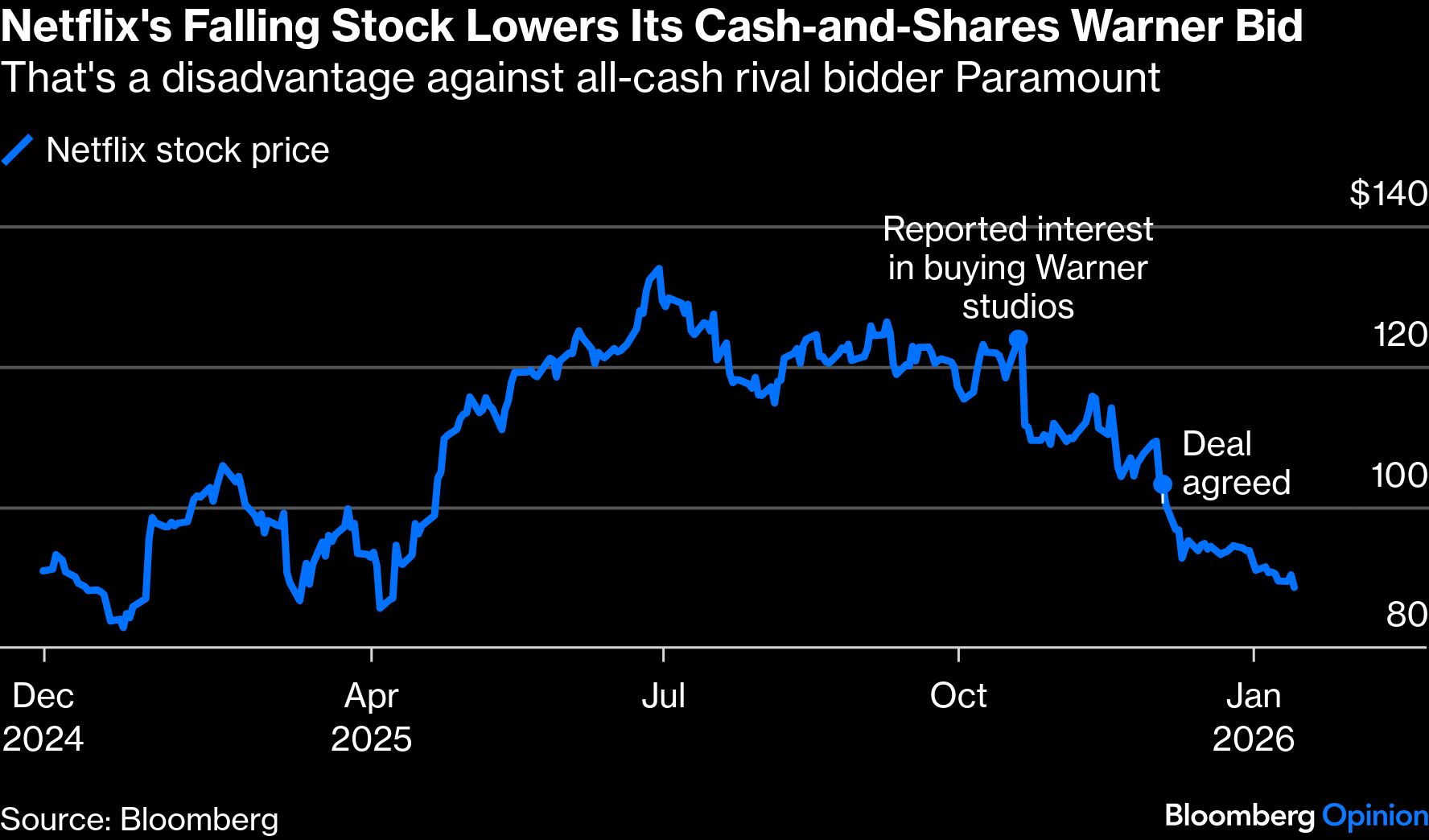

Sure, the Ellisons are leading rival suitor Netflix Inc. on price. Paramount Skydance Corp., the studio backed by tech luminary Larry Ellison and led by his son David, is dangling $30 per share for the whole of Warner. That’s attractive compared with Warner’s December deal with Netflix, where the studio and streaming arms get sold for a targeted $27.75 in cash and stock, and shareholders keep a cable-TV business whose value may not cover the shortfall versus Paramount’s pitch.

But there’s a snag with Paramount. What happens if a deal is agreed which ultimately doesn’t close? Warner worries that the financing could collapse, resulting in a lot of wasted time and money. The reasoning is that a Paramount takeover would rely on such a vast debt package that it wouldn’t take much to spook lenders Bank of America Corp., Citigroup Inc. and Apollo Global Management Inc. into pulling out — assuming the small print offers an escape hatch. Gross debt, on Warner’s assessment, would be around seven times the two companies’ combined profit as measured by expected earnings before interest, tax, depreciation and amortization.

It’s unclear whether this uncertainty is worse than the main doubt about the Netflix bid: the risk of a successful antitrust challenge to the creation of an even more powerful streaming giant. The ratio of debt to profit in a combined Paramount-Warner looks less scary if you boost the profit side of the equation with cost savings expected from a tie-up. Factor in these, plus cash at hand, and Paramount says net debt would fall below four times Ebitda on completion, and would drop further over the subsequent two-and-a-half years.

Giving full credit for the these savings from day one would be overoptimistic, but it seems fair to allow for some benefit. Plus there’s $41 billion of Ellison-backed equity in this proposal. That’s a huge cushion.

Warner is, however, more convincing when assessing how bad the fallout would be from either deal failing. If the Netflix transaction gets blocked, Warner just reverts to its pre-deal strategy of becoming a focused studio and streaming business having spun off its cable TV arm, Global Networks. Netflix doesn’t want cable, so the carve-out is set to proceed as planned while the takeover grinds through regulatory scrutiny.