Big banks’ share traders are raking it in right now. Sure, stock market indexes have been flying high, but it’s been far from certain in recent years that traditional Wall Street firms would reap the benefits with electronic market makers storming the zone.

Despite the blistering growth of these rivals, the equities desks at Goldman Sachs Group Inc. and Morgan Stanley made record revenue last year, the banks reported Thursday. The question now is whether the industry is at a peak.

Investors would be forgiven a touch of vertigo, but there are areas still due a recovery, including new listings, that should help buoy trading this year. Beyond 2026, however, a return to earth looks likely.

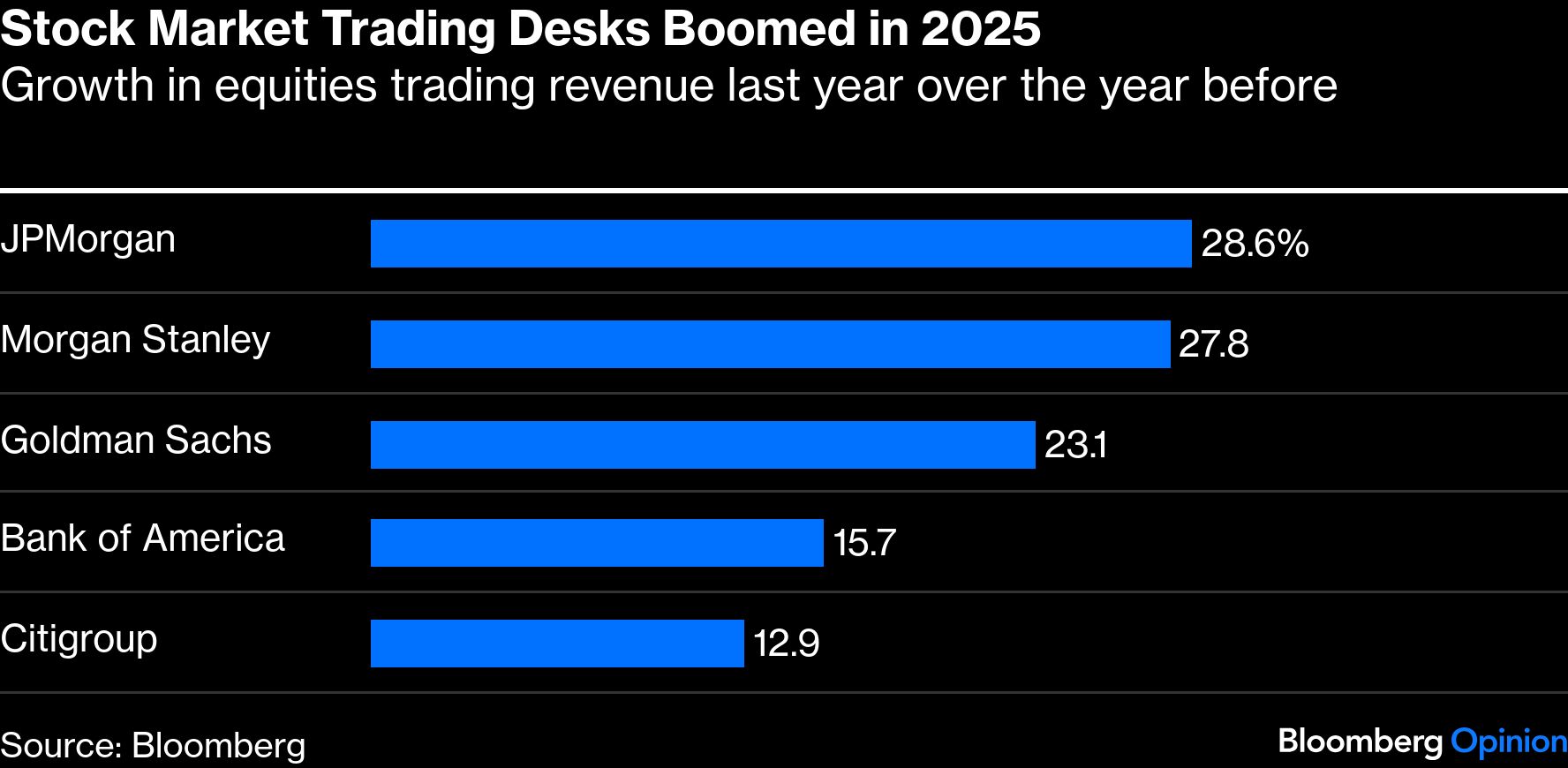

The sheer amount of money banks are making in stock markets is remarkable. Goldman’s $16.5 billion of revenue from equities alone was $3 billion greater than in 2024. It is also only marginally lower than the $17.1 billion combined haul of the four biggest European banks in 2024.

Morgan Stanley’s equities business grew 28% to $15.6 billion last year, also a record. JPMorgan Chase & Co. reported the strongest percentage revenue rise, up 29% versus 2024, while Bank of America Corp. and Citigroup Inc. also saw healthy growth.

The fact that these businesses are so strong even as electronic upstarts such as Jane Street LLC and Citadel Securities enjoy a boom illustrates a point I’ve made before: These two groups don’t compete directly in much of their business. Investment banks are increasingly focused on lending to hedge funds and other proprietary traders as well as selling more complex and higher margin derivatives.

At Goldman, the only bank to disclose what it makes from financing other traders, the lending side of the equities business was 44% of total revenue in 2025, up from 41% in 2024. On Wednesday, Citigroup flagged the greater share of revenue it now gets from financing in markets, although it doesn’t report specific numbers.

Prime brokerage, as this business is known, has become popular with the rise of very large multi-strategy hedge funds and because it’s meant to be a more durable source of revenue than matching buyers and sellers. Also, the fast-growing non-banks are more likely to be borrowers, they don’t make loans themselves.

But funding hedge funds is still a cyclical business. Fees are directly linked to stock market valuations because when share prices rise, the size of loans and the interest on them grows, too. Also, in buoyant markets, leveraged funds will take more risk, borrowing more relative to their capital. A big drop in markets can lead to both elements unwinding — sometimes dramatically.

Traditional Wall Street has also leaned heavily into structuring derivatives for big clients — another service electronic market makers don’t offer. Some of this activity is essentially like running a fund management business on trading desks. So-called quantitative investment strategies have become a huge business where traders use derivatives to create cheap versions of hedge fund offerings and sell them to clients. Globally, banks were forecast to make about $8.5 billion in revenue from this business in 2025, according to International Financing Review, the trade magazine.

But just like traditional asset management, QIS fees will rise and fall with stock prices; fees are linked to the value of the trades and investors tend to pull money out of markets when they’re heading in the wrong direction.

These desks build defensive strategies for clients, too, so some of this business should survive or even grow if technology and AI-related stocks do turn out to be in a bubble and markets suffer a big drop. But bankers don’t see that happening in 2026. In fact, there are reasons to expect another boost in the short term.

Initial public offerings from companies wanting to list on stock markets have yet to fully recover, and and there is a big crowd of private equity funds waiting to sell their portfolio businesses this year. That promises fees to investment bankers first, but traders should still benefit as investors reshuffle portfolios to buy into new stocks. Similarly, Morgan Stanley and Goldman executives predicted another rush of mergers and acquisitions in 2026 after last year produced the second biggest year for deals on record. This too could help stock traders to the extent that public companies are involved.

Big banks have arrested the long, slow decline in equities trading they experienced before the Covid pandemic and they have found new ways to make money where upstart competitors don’t operate. But the exuberance of stock markets right now can’t be ignored. If the records set by Goldman and Morgan Stanley in 2025 aren’t the peak, we are surely getting pretty close to it.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Paul J. Davies