The views presented here do not necessarily represent those of Advisor Perspectives.

The views presented here do not necessarily represent those of Advisor Perspectives.

I often tell clients to get real in their thinking. I advise them to stop thinking in nominal terms and to quit kidding themselves by including return of principal as income.

Spending power is the only thing that matters. We save and invest so we can consume later in life to support the lifestyle we want. Thus, they need to think in real, inflation adjusted terms.

As an example, a client will sometimes tell me they miss the good old days in the late ‘70s when they could earn 12% on a money market. The problem was that inflation was nearly 14% so, even before taxes, their spending power was being diminished. I assure them those weren’t the good old days at all.

Yet the good old days aren’t so old. In fact, I think they are today, given that real Treasury Inflation Protected Securities (TIPS) are yielding as high as 2.6% above inflation. Ironically, I’m often asked if I can translate that real return into a nominal return to compare to nominal bonds. I decline to do so, as the real return is the only thing that matters. It’s much better to convert the nominal return of a Treasury bond to a range of real returns. It must be a range because no one knows future inflation.

The Problem With Nominal Thinking

Nominal thinking in investing, a form of the "money illusion" bias, is the failure to account for inflation's erosion of purchasing power. The primary problems with this approach are overestimating real returns, misjudging true wealth, and making poor long-term investment decisions based on misleading nominal figures.

Focusing on nominal values without considering inflation leads to a gradual, "silent" decrease in the amount of goods and services one's money can buy over time. Cash savings and nominal bonds are particularly vulnerable to losing real value during periods of high inflation.

As an example, a man recently came to me bragging about the fact that he had been withdrawing from his portfolio for a decade and the account still hadn’t declined. He enjoyed the fact that he was living off of the portfolio returns. The problem with that is inflation was 35.7% over the past decade. In real terms, his account had declined by 26.3%. He was actually living off of his principal, and — I suspect — was in danger of outliving his money.

The Problem With Income That Isn’t

The vast majority of municipal bonds are issued at a premium. They will mature or be called at par as the premium is amortized over time. Naturally, the SEC, which regulates municipal bond mutual funds and ETFs, excludes this amortization of principal. But the bonds themselves are regulated by the Municipal Securities Rule Making Board (MSRB), a self-regulatory organization.

The MSRB allows the inclusion of the return of principal from this amortization of premium as income. I’ve seen this muni bond illusion hundreds of times when clients come to me noting their muni bonds in their separately managed account yield so much more than a low-cost muni bond fund like the iShares National Muni Bond ETF (MUB). When the client says it generates far more income than a bond fund, I have to explain the muni bond fund illusion.

The Extreme Danger in Putting Both Illusions Together

Vanguard’s web site notes that “retirement income is top of mind for most plan participants.” They state that 86% of participants want their employers to offer retirement income. Vanguard is partnering with TIAA to offer a target-date retirement series that incorporates the TIAA Secure Income Account as the lifetime income annuity option. This follows BlackRock’s “LifePath paycheck” offering in 2024.

It’s quite intuitive to want income that will never run out. Unfortunately, it’s a dangerous double illusion. Not only does it include return of principal (the trickery in why annuity income pays more than a bond or CD), it’s all but guaranteed to lose spending power.

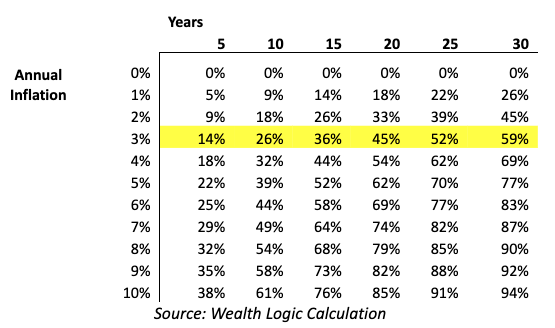

In the chart below, you can see the reduction in spending power. Even if inflation comes in at 3% annually (lower than the historic average), 59% of the spending power is gone after 30 years. Higher inflation results in a catastrophic collapse in spending. While the risk-pooling provides longevity protection, that protection may not be worth much.

Annuity Spending Power Reduction & Inflation Over Time

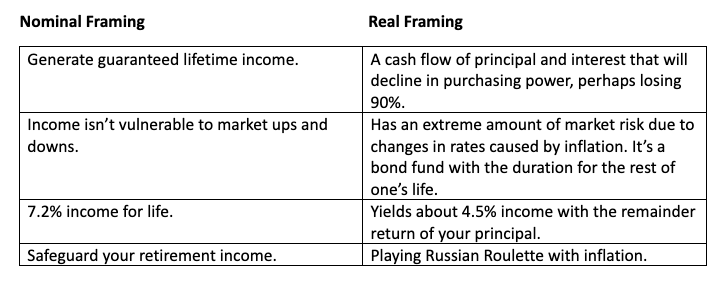

Framing such an annuity in terms of nominal thinking vs. real thinking would likely lead to very different behavior.

Illustrative Example of Annuity Framing From 2 Perspectives

You can see that nominal framing leads one to buy this money illusion of guaranteed income for life with no market risk that pays so much more than equivalent bonds. It’s a paycheck for life that secures purchasing power. But when you frame in real terms, the annuity doesn’t look so good. Both Vanguard and BlackRock recommend supplementing the annuity with inflation hedging assets such as equities, and TIAA has increased payouts to annuitants in the past.

Conclusion

Money is emotional. It represents freedom to do what we want with our lives. That leads us to frame decisions that are not economically optimal. Multiple Nobel Prizes have been awarded in this field of behavioral economics.

Help clients to get real in their thinking, taking into account both expected inflation as well as the risk around that expected inflation. And do not include return of principal as income.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multibillion-dollar companies and has consulted with many others while at McKinsey & Company.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more articles by Allan Roth

The views presented here do not necessarily represent those of Advisor Perspectives.

The views presented here do not necessarily represent those of Advisor Perspectives.