Bitcoin and other digital tokens, once touted as the uncontrolled and decentralized future of money, have proved to be lucrative tools for fraudsters, terrorists and rogue regimes. In response, Congress is now attempting to create an effective legal framework that will enable promising innovations to flourish while curtailing bad behavior.

It’s the right goal. Unfortunately, this effort is likely doomed unless federal market regulators are empowered and equipped to do the job well.

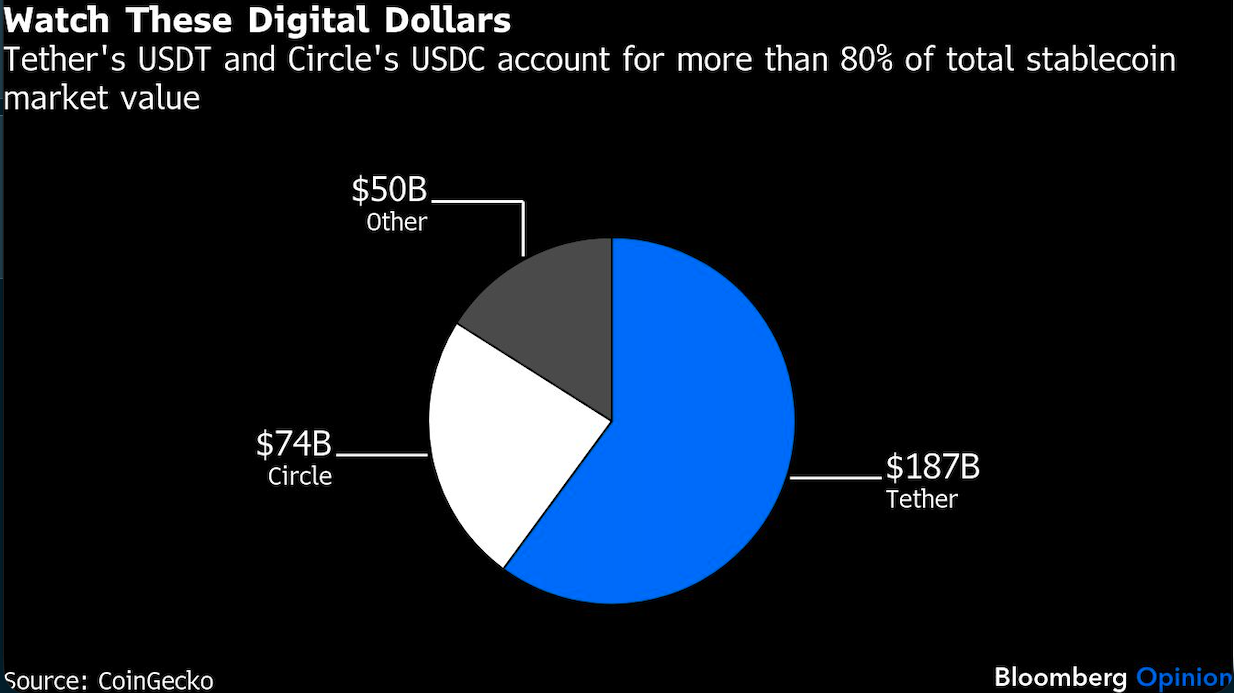

Last year, Congress passed a law called the Genius Act, which aims to govern so-called stablecoins, or digital tokens that mimic dollars. The risk of such instruments is clear: Two companies, Tether Holdings SA and Circle Internet Group Inc., have already amassed some $261 billion of the market’s $311 billion in assets. A run on either company could destabilize financial markets.

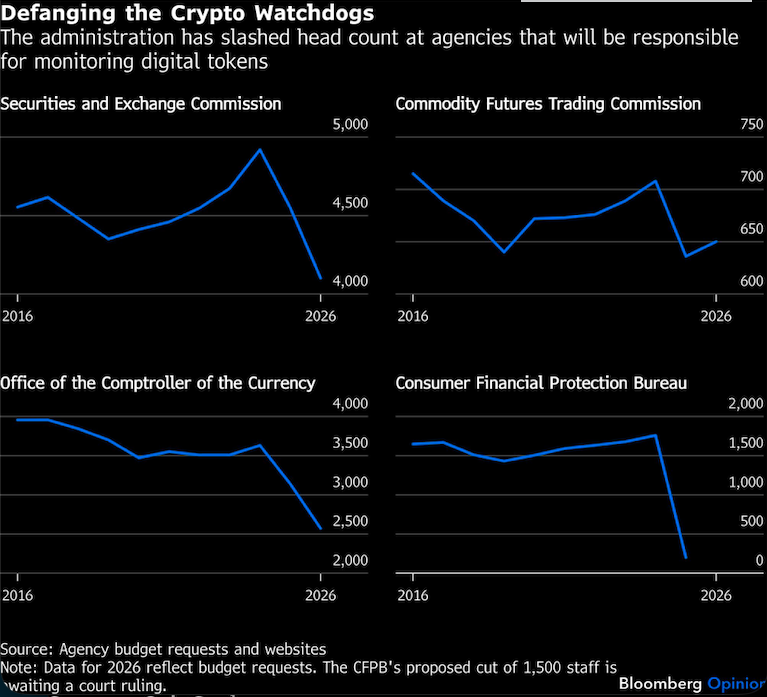

It will fall to regulators to ensure that the coins are backed by safe, liquid holdings and easy to redeem. Yet the law divides responsibility between different overseers, and much of the authority will lie with the Treasury Department’s Office of the Comptroller of the Currency, an agency that lost about a quarter of its staff in 2025 and is still reeling from a disastrous cyberattack.

A different proposal, called the Clarity Act, also attempts to streamline crypto regulation. Yet its criteria may prove hard to apply in practice, and it would explicitly limit the Securities and Exchange Commission’s authority over tokens, deeming most of them “digital commodities” under the purview of the Commodity Futures Trading Commission.

The CFTC, with a budget one-sixth that of the SEC’s, has already slashed enforcement staff and is being led by just one commissioner of the five required by statute. (The new commissioner, Michael Selig, hasn’t committed to raising more funds for the agency by levying fees on crypto companies, as the law would allow.)

Meanwhile, the one financial regulator that tracked consumer complaints related to crypto assets — the Consumer Financial Protection Bureau — has been effectively dismantled.

By now, the folly of this approach should be evident to the industry. Crypto entrepreneurs have been inviting regulation for years, hoping to boost trust and adoption, and to gain access to banks and retirement accounts. If “regulation” by enfeebled agencies leads more Americans to invest in cryptocurrencies, only to learn that fraud and crime remain pervasive, this effort is likely to backfire.

A better approach would be to create a new legal framework for trading in all digital assets that aren’t easily categorized, such as Bitcoin and Ether. The SEC and CFTC could then jointly draft rules to ensure that all market participants meet basic requirements for safety and soundness, customer protection, and disclosure and governance.

A rulebook of this kind would be more adaptable as technology evolves, preventing companies from exploiting statutory loopholes.

Any such framework, though, will fail unless Congress ensures that the industry’s regulators have the authority, competence and resources needed to keep crypto safe. Until it does so, buyer beware.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.