Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Three months after her husband died, 68-year-old Ruth (name changed for privacy) sat across from me with a plan that sounded reasonable.

“My son thinks I should move out of Ohio and move in with him and his wife in Texas,” she said. “They’re even talking about maybe buying a bigger house together with me.”

On paper, it may have seemed to check all the right boxes: Close to family; a built-in support system; shared living expenses. Upon hearing that, many advisors would support this plan out of an urge to help her “solve the problem” of living alone.

However, red flags emerged as we talked through this plan: Strained family relationships, weak local ties, and pressure to act hastily.

Ruth didn’t get along very well with her daughter-in-law. Their relationship was polite but tense. She knew no one else in Texas — no friends, no church, and no familiar community groups. Connection was lacking. She had no trusted healthcare providers there. Everything familiar — her routines, relationships, and sense of home — was rooted in the Ohio house she had shared with her husband for decades.

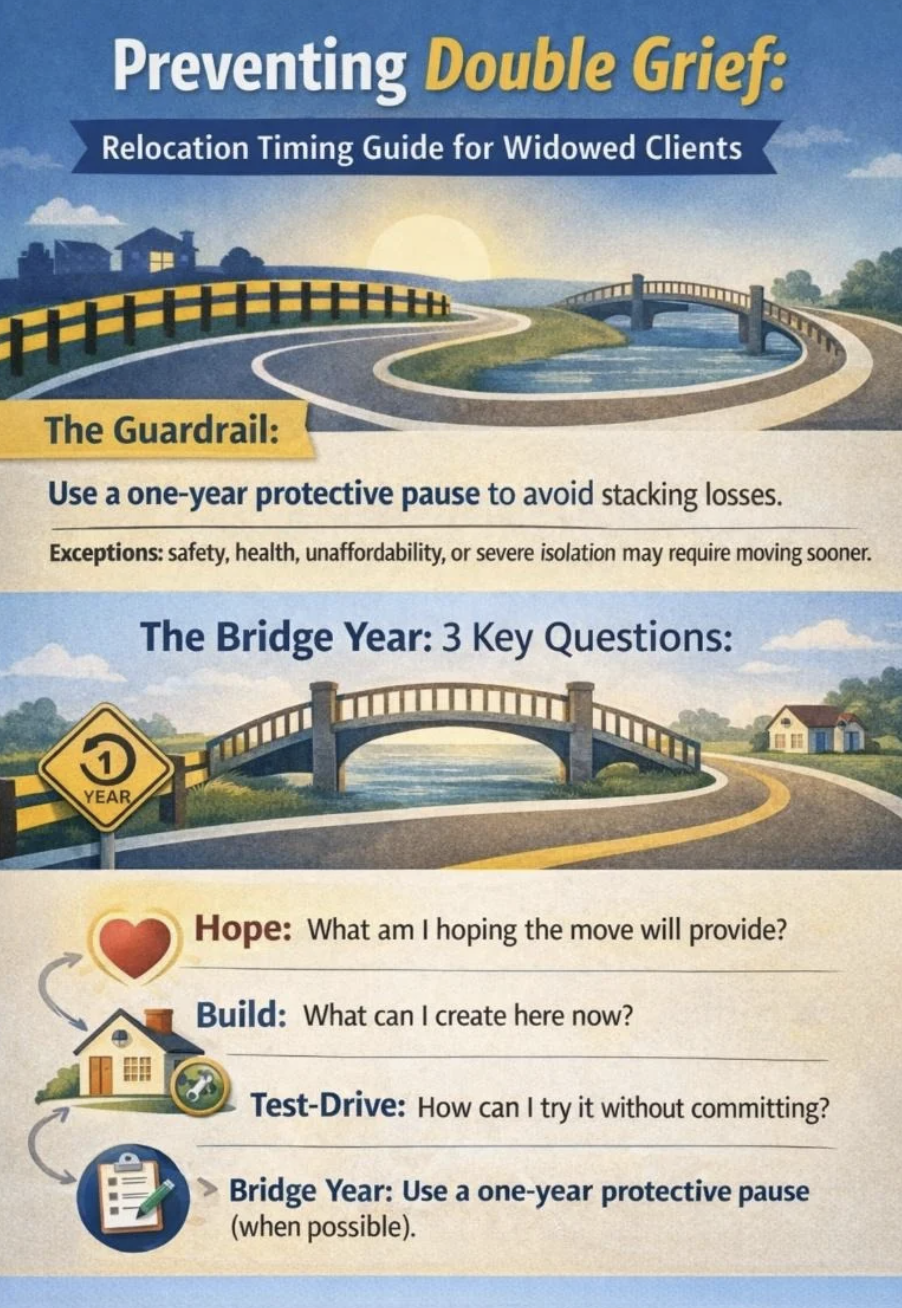

She wasn’t just considering a move. She was contemplating a second major loss — the loss of her sense of place, belonging, and identity after decades rooted in one community. That’s when I proposed something that’s become central in my work with widows and the advisors who support them: a relocation guardrail. This is a one-year protective pause before making a significant, hard-to-reverse move — unless there’s a strong safety, health, or financial reason not to wait.

Ruth decided to pause her decision for a year. As it turned out, during that time, her son took a new job in California. Both he and his wife quickly moved west for this opportunity.

Had Ruth moved right away, she would have faced two major relocations in rapid succession — first Texas and soon afterward California — all while coping with her fresh grief as a widow. Instead, she avoided what I call double grief: the death of a spouse followed by the sudden death of place and community.

Advisors are increasingly asked to weigh in on these decisions. We need a clearer framework for how — and when — to respond. The approach I often recommend has two parts: The guardrail (pause when possible) and the bridge year (a plan for what to do during the pause).

Why Relocation After Widowhood Is Uniquely Risky

Professional advisors generally provide sound technical advice to widowed clients. The mistakes tend to occur around timing and context. After a spouse dies, relocation decisions tend to bundle multiple motivations:

- To be near family and feel safer;

- To lower expenses or simplify life;

- To escape the emptiness of a house filled with memories; and

- To respond to pressure (spoken or unspoken) from adult children.

Each reason is understandable. But under the cognitive fog of grief, those motivations can lead to permanent decisions made in a temporary emotional state.

Relocating — especially across state lines — usually consolidates multiple transitions into one: New home, new community, new routines, new doctors, new legal and tax situations, and often new family dynamics. For a widow who already feels unmoored, that can be overwhelming.

From a planning perspective, there’s another layer of risk: Adult children are more mobile than ever. A move that’s anchored entirely on “living near my son” can unravel quickly if his job or relationship changes. The widow may be left in an unfamiliar place, without the very support she moved for.

The Guardrail: A Protective Pause, Not a Law

When I talk about a one-year protective pause, I don’t mean a rigid prohibition. Life rarely fits into neat time frames. In some situations, moving sooner is clearly appropriate:

- The current home is unsafe or unaffordable;

- The widow’s health requires a different living arrangement; or

- Isolation is severe and local support is minimal.

In those cases, waiting a year might be unrealistic or even harmful. Therefore, I don’t tell widows, “You must not move for a year.” Instead, I suggest a default approach: “Let’s treat major relocation in this first year of widowhood as a high-stakes decision that deserves more time, more information, and more emotional breathing room whenever we can give it.”

The guardrail is simply this: Unless there’s a strong safety, health-related, or financial reason to move quickly, we should pause for about a year before making a big, hard-to-reverse move. That year isn’t empty. It’s a bridge.

The Bridge Year: 3 Key Questions

With Ruth, we focused her bridge year on three key questions:

Hope: What are you really hoping a move will provide you?

When she listed what she wanted — companionship; a sense of safety; help with household chores, including yard work and repairs; and assistance if something major went wrong — it became clear that moving to Texas was just one way to satisfy those needs.

Build: What parts of that vision can we create where you are now?

We strengthened her local support system: friends, neighbors, and faith community. We connected her with a grief support group. We found a handyman recommended by another of my clients for home maintenance and reviewed her cash flow and the true cost of staying versus moving so she could see her options clearly.

Test drive: How can you test drive the Texas idea without committing?

Instead of selling her house and moving in, she visited as a guest. She paid attention to the daily rhythm, the household dynamics, and how she felt emotionally there compared to at home.

That structure was important. Widows are often told not to make any big decisions for a year, but they are rarely given a plan for how to live during that year. Simply saying “don’t decide yet,” can leave them feeling stuck and powerless.

Advisors can offer a different message: “You don’t have to decide on your preferred home right now. Let’s use this year to test assumptions, gather information, and protect your future choices.”

That reframing turns the pause into an active, purposeful period rather than a passive wait.

Naming “Double Grief” With Care

Double grief is a phrase I sometimes share with clients — but I always do so gently.

I might say: “You’re already grieving the loss of your husband. If you also give up the home, neighborhood, and community that hold your memories, that can feel like another kind of grief — the death of place. My job is to help you avoid stacking those losses on top of each other too quickly, if we can.”

Many widows understand immediately. They might still want to move, but they now see the decision as more than just about housing. It’s about their identity and community. Once that awareness clicks, your role shifts from simply approving or disapproving the move to helping her think it through, clarifying trade-offs, revealing unspoken pressures, and guiding her steps.

Exceptions: When Moving Sooner Still Makes Sense

There will always be cases where waiting a year is too long. In those situations, I still encourage advisors to honor the spirit of the guardrail, even if the timeline is shorter:

- Acknowledge that the decision is happening under pressure.

- Plan a check-in several months after the move to reevaluate how it’s working.

- Help preserve some connection to the old place — ongoing relationships, photographs, possible visits, or meaningful rituals—so the death of place doesn’t feel emotionally consuming.

The position remains the same: Protect flexibility, avoid unnecessary extra losses, and support the client in making the most well-grounded choice possible given the circumstances.

What Advisors Can Take Away

For newly widowed clients, the question of whether to move or not is rarely just about real estate and finances. It’s about finding a sense of belonging, safety, and identity, and understanding how much emotional change one person can handle at a time.

Ruth ultimately decided not to move in with her son and daughter-in-law. By the time his job took him to California, she had strengthened her life where she was by deepening friendships, clarifying her finances, and discovering she could carry her husband’s memory forward without needing to leave the home they shared. She also realized that she probably wouldn’t stay in her house forever, but had time to consider all her options later, carefully, in her early 70s. She still grieved, but she didn't have to mourn both her spouse’s death and her place at the same time.

As advisors, we can’t stop the initial grief. However, we can be very intentional about not adding a second layer of loss.

Kathleen M. Rehl, PhD, CFP®, CeFT® (Emeritus), is an author, educator, and speaker who empowers widows financially and trains advisors in grief-aware client communication. After experiencing widowhood herself, she authored "Moving Forward on Your Own: A Financial Guidebook for Widows". Kathleen continues to teach and write about widows and money, legacy planning, and purposeful aging. Her website is https://www.kathleenrehl.com.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more articles by Kathleen M. Rehl

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.