The $5 trillion hedge fund industry posted its best returns since the Global Financial Crisis last year, a welcoming reprieve for an asset class that has been overshadowed by the rise of private alternatives. Before declaring the worst is over however, boutique funds have one more myth to bust.

Everything worked last year. A global stock boom lifted equity funds, while macro traders thrived amid the volatility created by President Donald Trump’s tariffs. Event-driven strategies also did well thanks to a surge in activist campaigns, especially in Japan where the government is pushing for better corporate governance.

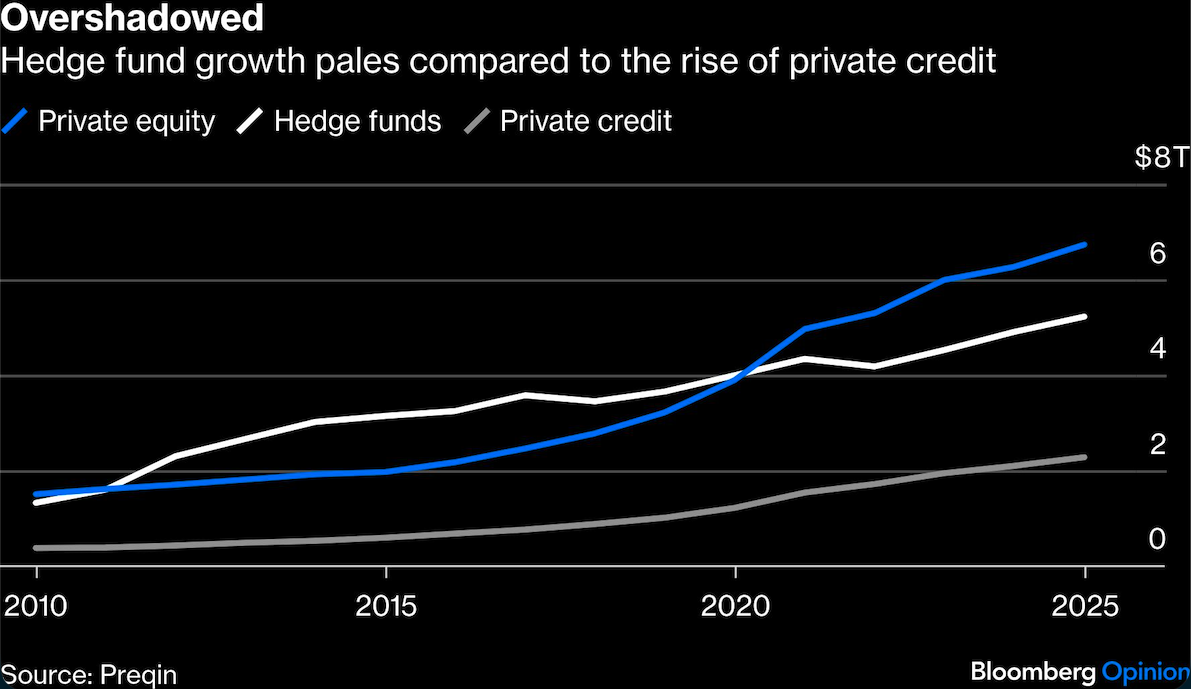

By comparison, private credit, marketed as a safer alternative that nonetheless offered handsome capital gains, was dogged by talk of “cockroaches” — distressed, indebted companies lurking in the shadows — and regulatory concerns over systemic risks. Private equity, meanwhile, continued to struggle with deal exits and returning cash to investors.

For hedge funds, there must be a sense of vindication. Fundraising has been tough since 2022, when investors pulled back because of poor performance and the lure of private credit. The number of new fund launches has contracted for four years in a row, while liquidations are becoming more frequent, according to Preqin, a private data provider owned by BlackRock Inc.

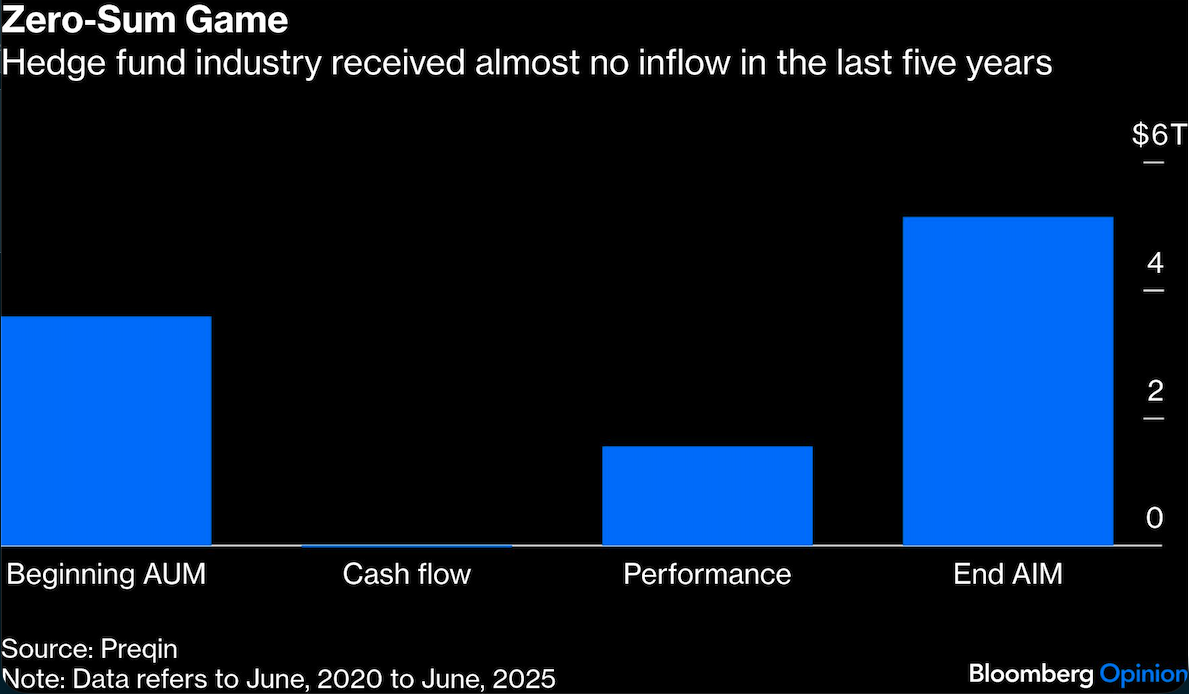

In the five years leading to last June, the expansion in total assets under management, or AUM, was almost due entirely to performance. In other words, hedge funds as a whole hardly attracted any new money, and fundraising became a competitive zero-sum game where a few winners take all.

Multistrategy funds have been sucking up all the capital. Just like private credit, these platforms, also known as pod shops, give investors the impression of delivering safe and superior returns.

Endowments and pensions can be forgiven for placing their faith in multistrats, because they offer textbook examples of diversification. They often host hundreds of semi-autonomous trading desks, each led by a portfolio manager who runs their own strategies. The pods’ risk exposures, in turn, are carefully monitored by top commands.

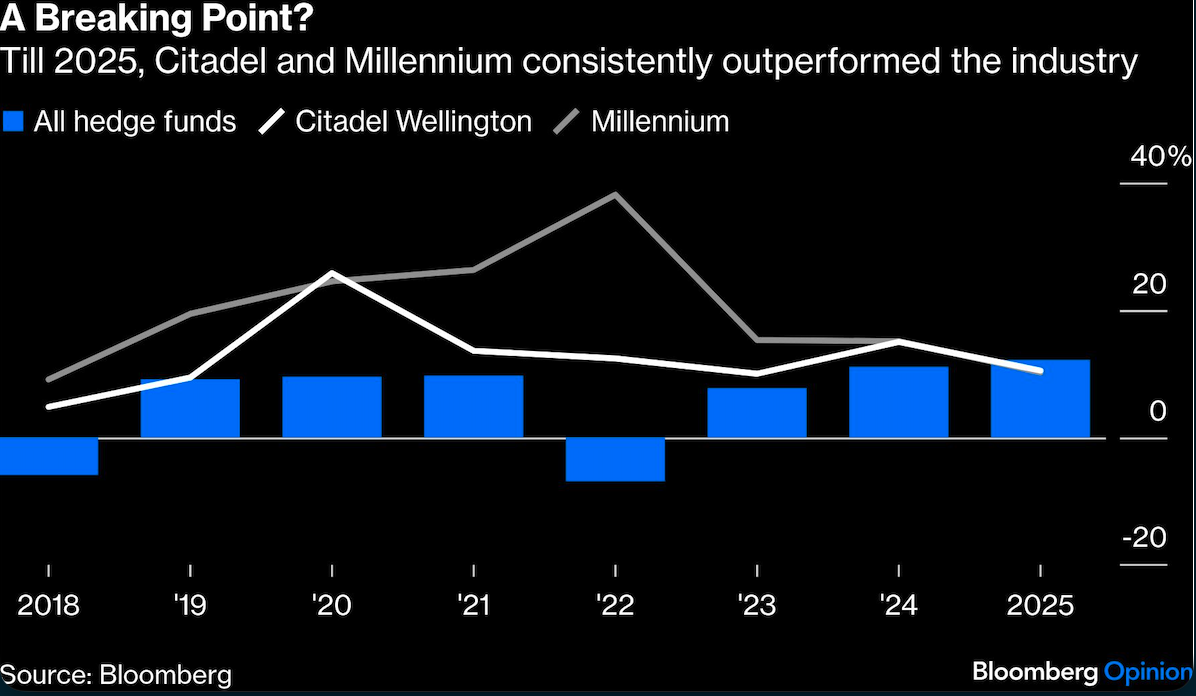

Stellar returns from the forerunners have only solidified that impression. Since 2020, flagship funds at Ken Griffin’s Citadel and Izzy Englander’s Millennium Management have delivered double-digit returns every year, particularly in 2022, when the whole industry posted negative gains.

Citadel and Millennium’s outperformance only dimmed in 2025, which explains in part why global investors are starting to open their pocketbooks to boutique shops. In recent weeks, we’ve witnessed a few billion-dollar-plus debuts, each devoted to stock-picking, or specialized trading strategies such as profiting from relative price differences of credit derivatives.

But a few trickles do not make a flood. Strategy-specific funds still have to face tough questions, as global investors look past 2025 to an uncertain future.

Take equity-focused funds for example. Last year, the patience of managers running a long-biased strategy, which bet on rises in their stock picks, was rewarded. Chris Hohn’s TCI Fund Management, for example, broke the hedge fund profit record set by Citadel in 2022 for its large, long-standing bets on aerospace companies. However, do these conviction plays work for just one year, or are they the beginning of a yearslong super cycle?

Long-short hedge funds that buy stocks they expect to rise and short shares they expect to fall also did well last year. But as their gross leverage rose, investors are understandably concerned about short squeezes — that they will scramble to cover and incur losses in a rising market. A basket of most-shorted stocked tracked by Goldman Sachs has surged 18% year-to-date.

Fortunately, as hedge funds look to raise new capital, they no longer have to compete with private credit. But unless some poorly managed pod shop blows up, demystifying these modern multi-managers’ superior risk-return profile remains a tall order. Boutique funds are not out of the woods yet.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Shuli Ren