Buying a house is expensive enough these days. But the costs of owning one have been rising, too — not least because of soaring insurance premiums. As policymakers of both parties have made housing affordability a top priority in recent years, they’ve done far too little to address this crisis in the making.

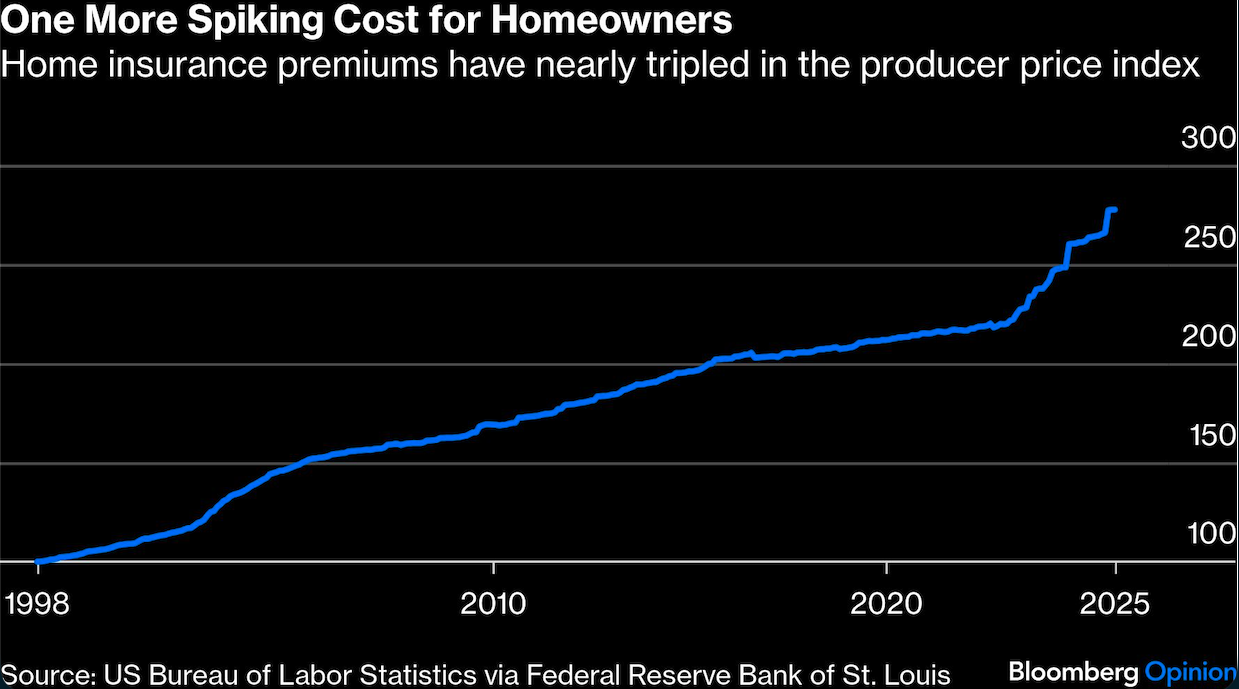

The figures are striking. Average homeowners insurance premiums rose almost 25% from 2019 to 2024 in real terms. Such costs have contributed to a slump in the condo market, with prices at a decade low, and are one reason for rising rents. New York City landlords with rent-stabilized units reported an 18.7% increase in insurance costs in just one year.

What’s behind this surge? Politicians have been quick to blame greedy insurers, but the real story is more complicated.

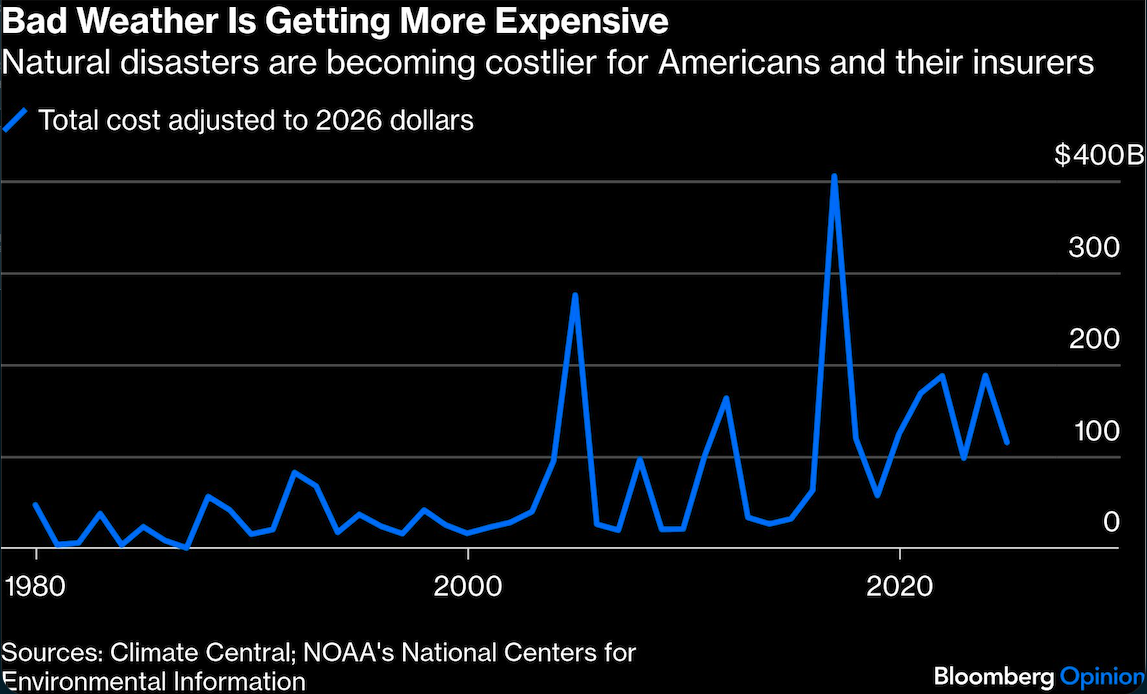

One problem is that disasters are getting more expensive. Thanks to climate change, surging construction costs and the “expanding bull’s-eye effect” — whereby increasing populations and property values in vulnerable areas lead to costlier damage — there’s been a sharp increase in billion-dollar disasters. Insured losses from such calamities reached $108 billion in 2025.

Second, despite these costs, policymakers haven’t done nearly enough to prepare. States still spend a tiny fraction of their disaster budgets on resilience measures, such as retrofitting public works and enforcing appropriate building codes. Meanwhile, the White House is attempting to cancel the largest pre-disaster mitigation program at the Federal Emergency Management Agency, which has supported thousands of state and local preparedness projects.

Finally, escalating legal costs are also getting passed on to homeowners. In many states, underwriters must contend with laws that favor plaintiffs, outsized jury awards and a proliferation of funds that specialize in financing lawsuits. Research suggests that such costs have been the single biggest driver of premium increases in recent years.

For policymakers, it’s all too tempting to look for simplistic solutions, such as capping premiums, subsidizing homebuyers or punishing investors. Such measures are likely to backfire. When California tried to artificially suppress premiums, underwriters fled the market and left homeowners and the state’s insurer of last resort exposed to last year’s horrific wildfires. (The state has since allowed significant increases to lure insurers back.)

A smarter approach will require attending to the underlying causes driving premiums up.

States should start by prioritizing the resilience of buildings and public works. Tax breaks and grants for hardening homes against floods, fire and wind are a short-term expense with long-term benefits; one study found that communities lose as much as $33 in future economic activity for every $1 not invested in preparedness. Alabama provides one model: By offering grants up to $10,000 and discounts on wind-damage insurance, the state encouraged thousands of homeowners to install roofs that have been proven to reduce the cost and frequency of claims.

The federal government, for its part, should commit to restoring FEMA’s pre-disaster mitigation program and similar efforts. With strong oversight, such investment can protect property, limit job losses, accelerate rebuilding, reduce premiums, improve public health, and ultimately save money and lives. The key is to shift the balance from reacting to natural disasters to preparing for them. (Also worth noting: Tariffs on building supplies and Draconian immigration roundups have hardly helped construction costs.)

As for out-of-control litigation, Florida offers an encouraging example. In 2021, the state was home to 6.9% of homeowner claims but 76% of the lawsuits against insurers. State lawmakers enacted reforms over the next two years that limited plaintiffs’ ability to allege negligence and recoup expenses, with significant results: At least 17 new insurers entered the market and dozens reduced premiums. Other states known as “hostile jurisdictions” should take note.

The soaring cost of housing is a crisis for many Americans, and insurance premiums are a growing part of the problem. Policymakers need to grapple with the challenge in all its complexity, avoid facile solutions and embrace incremental improvements — then build on them.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.