There are calls in Europe to “sell America” and invest that money at home in response to political tensions over Greenland. European businesses could sure use the boost after printing some $6.7 trillion less in revenue than their US peers last year – a gap that’s set to expand. And no, it’s not all about Big Tech.

Sergio Ermotti, chief executive officer of Swiss-based UBS Group AG, ruled out divestment from the US in a recent interview with Bloomberg TV, calling it a “dangerous bet” given the US’s “highest level of innovation.” For many, that innovation and its financial rewards conjure the US technology titans — the Magnificent Seven plus Broadcom Inc. — that account for nearly a third of the US and Europe’s combined stock market value. At their size, excluding them from a portfolio would be a big gamble indeed.

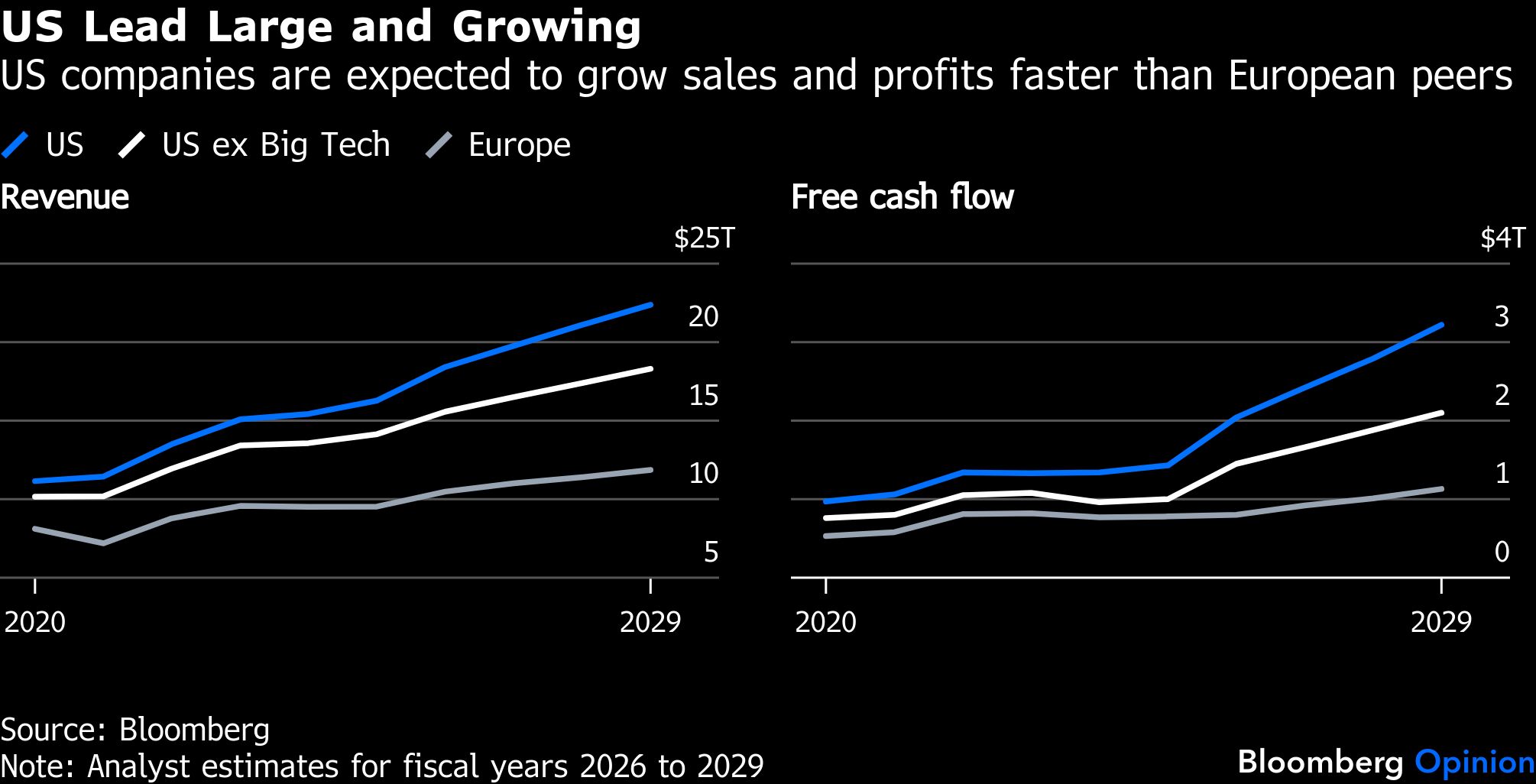

But the US’s edge runs deeper than eight companies. It extends to most sectors, from consumer products and health care to communications and energy, across more than 1,600 US and European stocks for which Bloomberg compiles revenue and free cash flow results and forecasts. The two groups, roughly equal in number, represent about 85% of US and European stocks’ combined market value. (I’m looking at free cash flow because it accounts for spending on both research and development and capital expenditures.)

In aggregate, revenue at US companies grew by 8% a year over the past five years, while European companies grew sales by just 3%. Excluding the tech titans, US revenue growth was still an impressive 7% a year. The difference in growth adds up to a lot of money. In fiscal year 2020, US companies generated $3 trillion more in revenue than their European counterparts, and $2 trillion more excluding the tech titans. Last year, the US lead swelled to $6.7 trillion and $4.6 trillion, respectively.

Surprisingly, European companies grew free cash flow at the same rate as US companies despite lower revenue growth. That’s because they compensated by expanding their FCF margin by a chunky 5% a year during the past five years while US margins were flat.

Here’s the rub: Margins grew faster in Europe mainly because US companies spent a lot more on R&D and capital investment. US companies invested nearly $9 trillion over the past five years, about $7 trillion excluding the tech titans, compared with $4.7 trillion in Europe. When accounting for the difference in investment, profit growth is higher in the US with or without the tech titans.

Analysts expect that investment in R&D and capital projects to pay off nicely — and soon. Consensus estimates are that US companies will continue to grow revenue by 8% a year over the next four years, compared with 6% in Europe. The big leap will be to profitability: Analysts estimate that US companies will grow FCF margins by 13% a year with or without the tech titans, compared with margin expansion of only 4% in Europe.

If analysts are right about the next four years, the US and Europe’s already sizeable performance gap will become massive. US companies are expected to generate $10.5 trillion more in revenue than the European group, $6.5 trillion of which excludes the tech titans. US companies are also expected to achieve $2.1 trillion more in free cash flow, about half attributable to the tech titans.

You can see why Ermotti dismisses the idea of divesting from the US. He acknowledges, though, that investors might consider underweighting the US for a time, perhaps a nod to the old Wall Street adage that the best businesses are not always the best investments. European investors are likely already on board. While US companies account for about 63% of global stocks by market value, European stock funds’ average allocation to the US is well below 50% despite trending higher in recent years.

Underweighting the US may finally pay off. In the medium term, the total return from stocks is a combination of dividends, earnings growth and change in valuation. European stocks have the edge in two of the three. US companies are clearly expected to grow faster, but European companies offer a higher dividend yield and lower valuations that leave more room for expansion, particularly if European companies beat expectations. That probably explains why the biggest money managers, including BlackRock Inc. and UBS, expect higher stock returns from Europe than the US in the coming years, despite America’s innovation advantage.

Fresh capital will come in handy, as European companies’ modest margins and revenue growth relative to the US leave less room for investment. Without it, they risk a negative feedback loop where declining R&D and capital investment lead to deteriorating fundamentals, making the case for long-term investment in Europe ever more difficult. In the long run, fundamentals drive returns.

With investment and commitment to innovate, there’s no reason European companies can’t rival those in the US. European policymakers can help by providing financial incentives and removing regulatory hurdles where possible. But as things stand, the long-term trajectory of European business points in an unfavorable direction.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Nir Kaissar