When interest rates are near zero, government debt doesn’t matter. That was the theory at least, in the previous decade, not just from economists on the fringe but also from a few in the mainstream. If rates stayed low, the argument went, the US didn’t need to worry about debt.

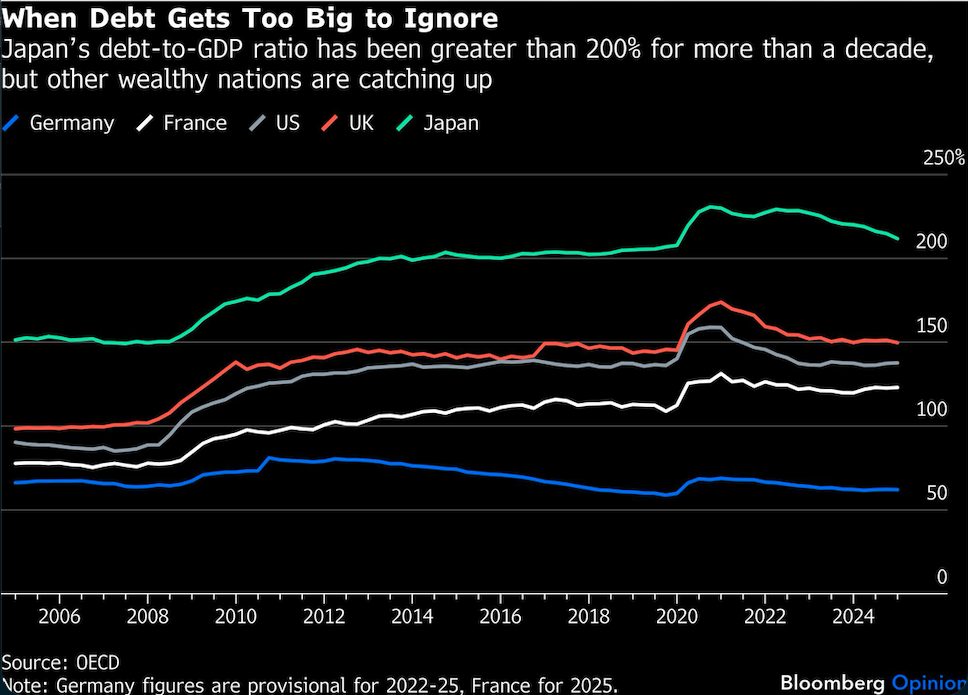

And it didn’t. Debt increased, and economists who cautioned against it (ahem) were dismissed as cranks, with many of our critics pointing to the history of one nation: Japan, which managed to keep interest rates low even as its debt grew to more than 200% of its GDP.

Reality, however, has a way of catching up with theory eventually, and now it has for Japan, whose long-term bond yields are rising as the yen is depreciating. The Japanese experience, it turns out, is not an excuse to run up lots of debt. It is a cautionary tale.

The Japanese economy has always been unusual. In the early 1980s, it looked unstoppable. But in 1985 it was forced to let the yen appreciate relative to the dollar, and it faced a financial crisis in 1992. Growth never resumed, and debt increased. Japan was able to manage the situation by holding down short and long-term interest rates, both through financial repression and quantitative easing.

It seemed to work, albeit with some distortions and low growth, until global inflation returned after the pandemic. Suddenly Japan was in a bind: If it increased rates to fight inflation, then debt costs would balloon. If it kept rates low and let inflation run high, the yen would depreciate.

In the end, it chose the second option. Long-term bond yields increased too, and in the last few weeks they’ve gone up further while the yen continues to depreciate, causing turmoil in global bond markets. The timing couldn’t be worse, with Japan mulling more fiscal expansion to revamp its economy, and it’s now risking a full-on debt crisis.

The situation not only offers a warning for emerging-market economies, where bond vigilantes are always ready to pounce. It also offers at least three lessons for richer countries that still behave as if they can run up debt without paying any costs.

Long-term interest rates are market prices — mess with them at your peril. For years it seemed that Japan could get away with so much debt because interest rates stayed low. Debt enthusiasts argue that you can’t default if you issue debt in your own currency and interest costs can be kept low with policy intervention. It is true that monetary policy has a strong influence on short-term interest rates. But longer-term rates normally are set in the market and reflect macro conditions such as inflation, debt and growth. Japan suppressed this dynamic by making sure there was a large captive buyer (often the central bank), and this kept debt costs down. This is an old trick that emerging markets often try, but it usually blows up quickly.

Japan, as a large and advanced economy with a big appetite for its own debt, was supposed to be different. It wasn’t — the blowup just took longer. There were also short- and medium-term costs; the artificially low rates created economic distortions, contributing to low growth. It also enabled policy makers to avoid badly needed structural reforms.

Inflation will return one day and undermine all your fiscal plans. For a few decades, it seemed monetary policy had tamed inflation. More than that, the idea that countries could run up debt and suppress interest rates depended on the assumption that inflation would never return. This was especially true in Japan, which suffered from extremely low inflation for decades.

But once inflation returned, markets pushed yields up — which meant keeping rates low took more intervention. It also forces central bankers to choose between higher inflation or higher costs to service the debt. They can only choose debt for so long before higher inflation expectations become entrenched, pushing rates up even further, causing a vicious cycle that is impossible for even the best central banker to manage.

The lesson here is that inflation risks never disappear. Inflation has been a risk since the creation of currency. Yes, monetary policy is much better at containing it, but as the world learned after the pandemic, inflation can always come back.

Governments can sometimes run up big debts and nothing happens, but it is not a long-term strategy. Or, to use a more homely (sorry) analogy: You can build a house on a fault line and live there for decades without it being destroyed in an earthquake, but that doesn’t mean it was a smart thing to do. If a country carries lots of debt, it is more vulnerable to financial crisis or more volatility in the bond market. There is no amount of government intervention that can ensure stability in all market conditions.

Even rich countries can have a debt or currency crisis. To be clear, Japan is not in a crisis yet. It still has lots of assets on its balance sheet, and it’s possible it will be able to manage a transition to a new kind of economic regime. But its debt gives Japan less room for the fiscal expansion it now needs. That’s the problem with having too much debt: Markets are least inclined to grant you grace when you need it most.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Allison Schrager