When it comes to housing affordability, the logic of “build build build” is straightforward enough: Housing is too expensive. If there were more of it, prices would fall. Ergo, build more housing. Homebuilders are even pushing a plan for a million new affordable houses, which they are calling “Trump Homes” to appeal to the president.

Unfortunately, it’s not that simple. The problem of housing affordability is much bigger than insufficient supply; it’s a mismatch with demand. And that demand is driven by income inequality that has seen soaring income growth at the top and tepid growth (or even stagnation) in the middle.

In other words: The way to improve housing affordability is to reduce income inequality.

Start with some context. After the housing bubble burst in 2005, the homeownership rate fell for 11 years, from 69% to 62.9% in 2016. It has since inched upward and is now about 65%. Meanwhile, mortgage debt service as a percentage of personal disposable income has also fallen, from a peak of 9% in 2007 to below 6% now, which is lower than before the pandemic. Neither of these signals is flashing red.

Whether the US has an overall housing shortage is a matter of dispute. The number of homes needed in the US is determined by the number of households, not the number of people. Since household formation has slowed — as children live at home longer and marriage and fertility rates have fallen — the need for housing is less great.

Plus, it is a morbid thought, but the supply of available housing is set to increase as baby boomers move into assisted living or die. Owner-occupied housing in the US is dominated by older people, and the youngest boomer turns 62 this year, while the oldest turns 80. Over the next 10 years, an estimated 15 million boomers will die.

A closer look at households and housing shows that, to the extent the US has a housing supply problem, it’s a supply of affordable housing. Just building more won’t solve this problem. Affordable housing requires government intervention into the market — developers don’t build housing for low-income families (and increasingly, middle-income families) without it.

No doubt those developers would say that government intervention, in the form of regulations, is what makes it so hard to build affordable housing in the first place. Yet here too, the acceptance of the claim precedes its proof.

A team of researchers from the Federal Reserve Bank of San Francisco assessed supply and housing prices from 2000 to 2020 and concluded that “supply constraints are unimportant in explaining differences in rising house prices among US cities.” Instead, they write, what predicts higher prices is “higher income growth.”

In a blog post summarizing their findings, they give the example of four cities: Houston, Austin, San Francisco and Los Angeles. The Texas cities saw much faster-than-average population growth but slower-than-average income growth. The California cities saw average population growth but much faster-than-average income growth. Supply responded to population growth in all four cities fairly closely; what pushed up prices in California was excess demand from very high earners.

No doubt part of the appeal of “build build build” is that it addresses housing affordability with only a light touch of government intervention: Just impose fewer rules and restrictions on builders, and let the market work its magic.

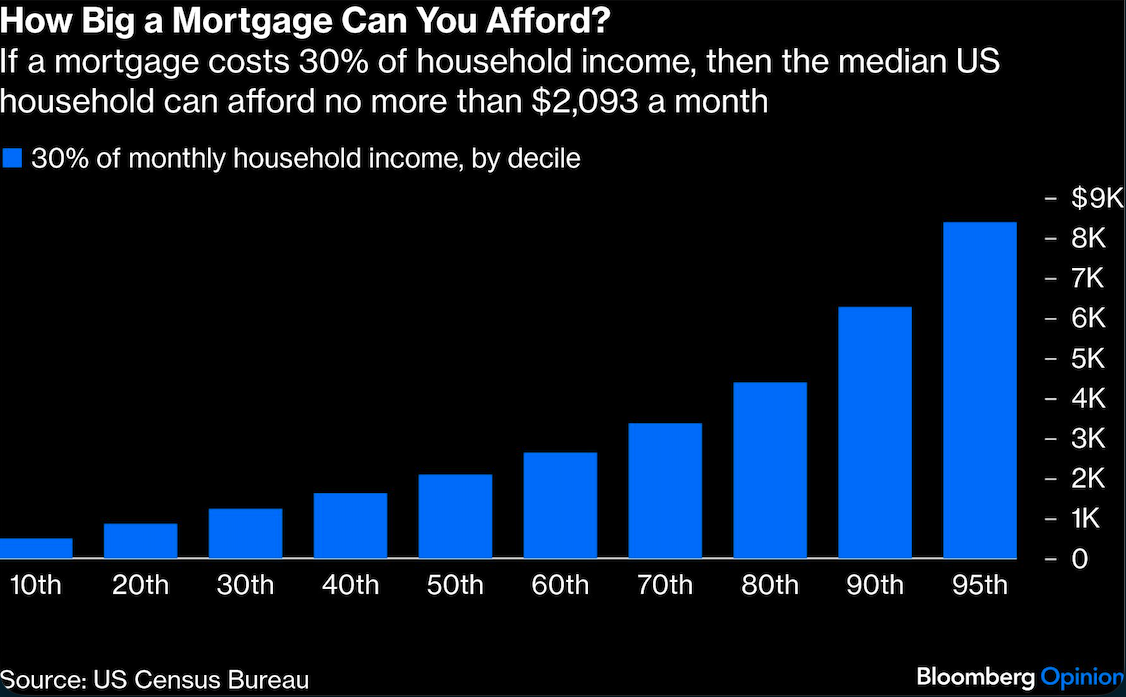

That magic isn’t as powerful as free-market believers would like to think. More supply can help, but to make a difference, it has to be available to households that are currently priced out of the market. Assuming that “affordability” means a household pays 30% of its income, the median household can afford no more than $2,093 a month — already $200 less than the median mortgage.

What’s needed are policies that increase income for households at the bottom and middle. Rather than boosting the housing supply in the hope that they benefit, the answer is to fix the labor market to make sure that they do. That means, among other things, raising the minimum wage, regulating shifts and time off so it’s easier to maintain a job, and helping workers unionize.

Granted, this is not exactly an easy fix. But the easy solution is often the inadequate one. The US has added 17 million housing units since 2009, a period during which labor’s share of income has remained flat at 59%. It’s not enough just to increase the housing supply. What America needs are policies that will steer the economy toward income growth.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Kathryn Anne Edwards