On an evening in late September, a few dozen wealth managers gathered at a $63 million French château-style mansion owned by Paris Hilton and venture capitalist Carter Reum in the exclusive Los Angeles enclave of Beverly Park. Sipping drinks a stone’s throw from the pink tennis court and five-hole golf course, the attendees had convened to discuss a topic that’s obsessed the asset management industry: how to give individual investors better access to private markets.

The host of the soiree—and of a forum in the less glamorous business district of Century City the following day—was a financial technology company called Allocate. (Reum is on its board.) Founded by a pair of former First Republic Bank colleagues, the company helps wealth managers access alternative investments including venture capital and private credit for their clients.

Allocate is just one of many companies trying to get in early on the biggest “next big thing” to hit financial services since the exchange-traded fund. Virtually every major firm on Wall Street has joined the push into private markets. Private capital giants Apollo Global Management, Blackstone, KKR and Carlyle Group have been among the most vocal proponents of the idea that investors should look beyond public stocks and bonds. To broaden private assets’ appeal to Main Street, some money managers have turned to TV commercials, print ads and sports sponsorships. Although these firms are best known for leveraged buyouts and other equity investments, they’re increasingly focused on putting together private credit funds that make loans directly to companies, bypassing banks or the bond market. And they want individual investors to buy in.

At first glance the appeal of private investments to an ordinary investor might seem limited. An S&P 500 index fund, which can be purchased for a management fee close to zero, has delivered an annualized return of about 20% over the past three years. With public returns like that, who needs private?

Of course, that’s with 20/20 hindsight. In the tumultuous years following the Covid‑19 lockdowns, private credit in particular emerged as a sought‑after new asset class—all the more alluring because it’s not easy for most people to purchase without the help of an adviser and a (richly compensated) asset manager. Swiftly rising interest rates hammered returns on bonds, the traditional choice for investors seeking regular income and lower risk. But private credit funds typically make higher‑yielding loans with adjustable rates, so their returns actually got better as rates rose. In 2023, Jon Gray, Blackstone’s president and chief operating officer, said investors were living in a “golden moment,” when private credit could deliver “equity-like” returns with the kind of risk you’d expect from a loan that’s first in line for repayment if something goes wrong. Today, many managers stress that private credit can deliver better returns than public fixed-income markets.

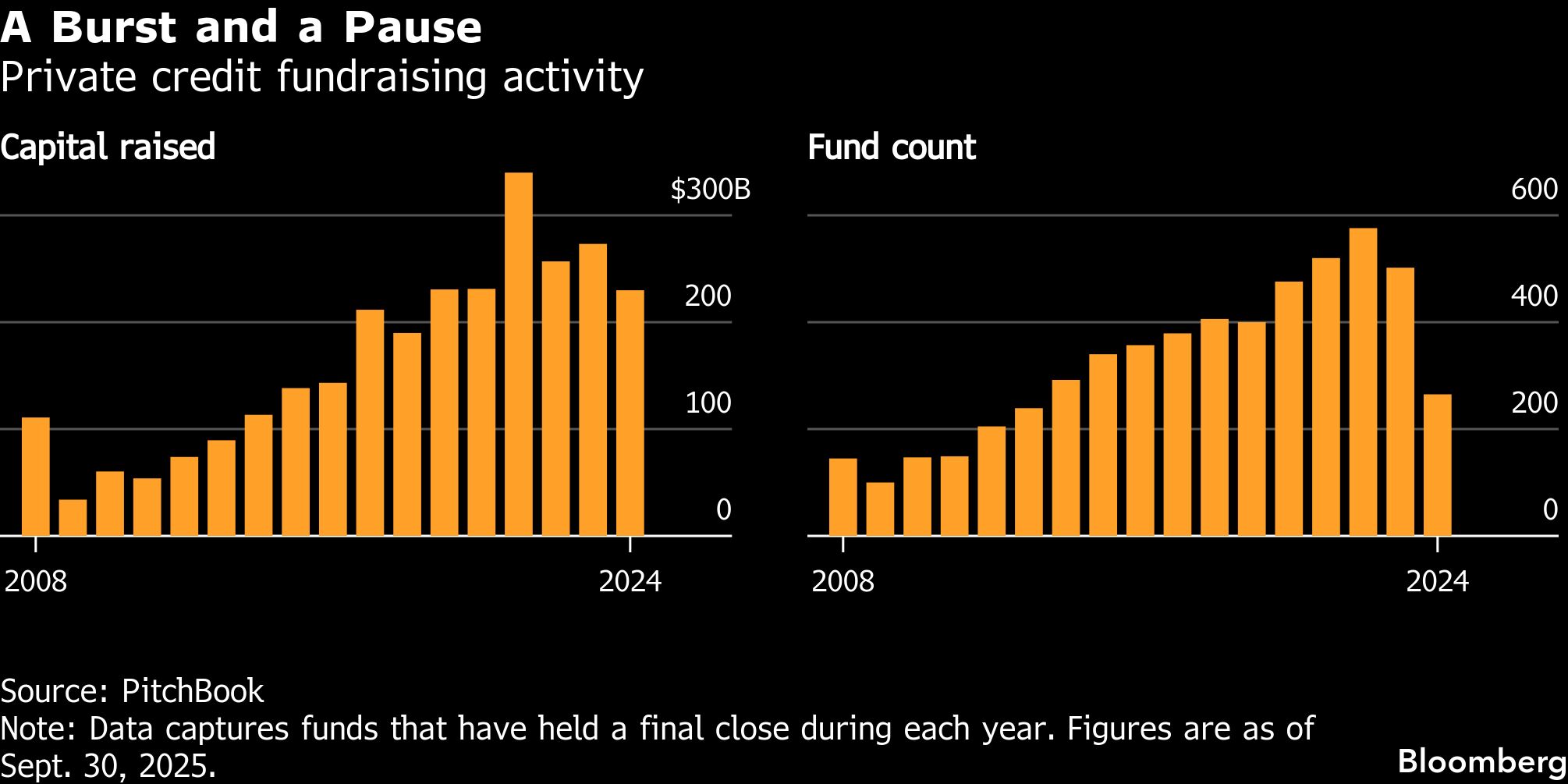

Globally, private credit assets now sit at $1.7 trillion, up from about $500 billion a decade ago, according to data provider Preqin. Bloomberg Intelligence says the broader universe of private capital—which includes private equity, infrastructure, venture capital and real estate funds—has swelled to almost $23 trillion in the US.

But for all the excitement and hype, the pitch for private assets has gotten more complicated lately. For years now private equity firms have struggled to cash out of their holdings at prices that would generate the kind of double-digit returns investors have come to expect, making it harder for many of them to raise new funds. Many venture capital firms are also struggling to monetize investments as companies opt to stay private for longer. Skeptics are also asking questions about the accuracy of private market valuations and about systemic risks arising from private capital firms’ ties to the bank system and insurance companies.

The twin blowups of subprime auto lender Tricolor Holdings and auto parts maker First Brands Group amid allegations of fraud have led to a serious reckoning on Wall Street. Neither company was owned by private equity, and most of their borrowing had been vetted by banks. But their collapse has sparked concerns of investor complacency and poor underwriting standards across public and private markets alike. It also put the spotlight on asset-based finance, since Tricolor bundled car loans into securitizations, while First Brands racked up billions in off-balance-sheet debt backed by invoices. Asset-based loans have been popular with private credit lenders looking for a safer alternative to traditional corporate loans.

And private capital firms are directly in the crosshairs of the latest market angst: software companies at risk of being displaced by rapid developments in artificial intelligence. Private equity and credit asset managers, which bet big on software providers in recent years, have seen their shares tumble this week.

These investor jitters come after several black-eye moments. In the past few months, private credit investments in home remodeling business Renovo Home Partners and a telecommunications group run by a little-known businessman have turned into zeros. The bankruptcy of portable toilet maker United Site Services, meanwhile, exposed the dangers of private equity continuation funds, which are used by buyout shops to transfer investments from one group of investors to another without selling them outright. The company had been one of those hand-me-downs.

Jeffrey Gundlach, founder of DoubleLine Capital, has gone so far as to warn that “garbage lending” in private credit could tilt global markets into the next meltdown, arguing the asset class has “the same trappings as subprime mortgage repackaging had back in 2006.”

Get the Going Private newsletter for coverage of private markets and the forces moving capital away from the public eye. Delivered on Wednesdays and Fridays.

Moody’s Ratings recently highlighted the increase in risk and complexity that stems from some of private credit’s favorite tools: payment‑in‑kind arrangements, which allow borrowers to defer cash interest payments, and off-balance-sheet transactions, which let companies raise debt against some of their assets without compromising their main credit ratings.

Regulators and policymakers have started to ask more pointed questions about valuation practices and systemic risks. One of the main concerns is whether managers have too much leeway to determine the value of the assets in their portfolios. Democratic Senators Elizabeth Warren of Massachusetts and Jack Reed of Rhode Island recently urged the top three banking regulators to scrutinize the private credit market and its links to the banking system, arguing that “fast and dramatic writedowns to zero raise serious questions about the discretion of fund managers to value private credit assets.”

Jay Clayton, who became Wall Street’s top prosecutor last year after serving as chairman at Apollo, has made clear the Department of Justice is watching the industry closely and won’t stand for managers cherry-picking their prices. He’s also said, however, the “pearl-clutching” over private credit writ large is “a little overblown.”

Outside the US, the Bank of England has launched its first-ever stress test of the private credit and equity markets. Watchdogs in the European Union and Australia have pushed for more transparency in private markets as they assess financial stability and contagion risks.

If that weren’t enough, many of the tailwinds that propelled private credit over the past few years are now moving in the opposite direction. Banks, which lost a lot of their corporate lending business to private credit when interest rates were rising, are back to financing mergers and leveraged buyouts, often beating private credit on terms. Interest-rate cuts, meanwhile, are reducing the appeal of private credit and other floating-rate products, complicating the pitch that Blackstone’s Gray and others have made. Josh Easterly, the co‑president of private assets firm Sixth Street, warned recently that returns in private credit are going to be “a lot lower” than they used to be and that investors are due for some disappointment.

Concerns over private credit’s prospects have already started to manifest in business development companies, a popular wrapper for private credit funds aimed at individual investors. Many BDCs trade on the market like stocks and are currently priced at double-digit discounts to the value of their assets, indicating that investors expect returns to fall.

In spite of these strains, asset managers are already invested in offering private markets to more investors. Franklin Templeton, T. Rowe Price and BlackRock have made a flurry of acquisitions to broaden their footprint in private markets. Others, including Capital Group and KKR & Co., have forged partnerships to sell private market funds to individual investors. And then there’s Apollo, which teamed up with State Street to start the first exchange-traded fund with exposure to investment-grade private credit. The fund accumulated around $100 million of assets after about a year—a drop in the ocean compared with the almost $2 trillion that State Street manages across its ETFs. Then it saw a spike of nearly $396 million in a single day of inflows from one unnamed investor in February.

There’s good reason for private capital firms to look to retail. Fundraising from traditional channels—public pensions, sovereign wealth funds and endowments—has slowed. Retirement and insurance accounts, on the other hand, are still largely untapped, which translates into a huge opportunity to gather more assets and fees. In August the industry got its strongest win to date in Washington, when President Donald Trump signed an executive order that paves the way for private assets to enter the roster of investments suitable for the retirement accounts of millions of Americans.

For many of the industry’s top executives, fighting the skeptics has become part of the job description. Marc Rowan, the key engineer of Apollo’s transformation from a sharp-elbowed private equity shop into a giant credit investor and insurance manager, has dismissed negative headlines about private credit as “hysterical.” In a 125-slide presentation published in December, his firm argued that private capital is critical to the US economy and that it has made the banking system stronger by shifting long-term risk to investors better able to bear it. Much of the worried talk about private credit, it said, has ignored a far larger universe of investment-grade private debt that Apollo has focused on. KKR co-founder Henry Kravis has similarly come to the industry’s defense, arguing there’s no systemic risk stemming from private credit.

Back on the conference circuit, the pitch continues. A couple of weeks after Allocate’s event, a platform called CAIS, which connects investment advisers to private market funds, logged record attendance of more than 1,200 for its own summit in Beverly Hills. A thousand more people had to be wait-listed.

The CAIS summit, which is free to attend for advisers, has become a crucial platform for private capital firms to connect with the intermediaries that could unlock trillions of dollars of savings for their retail-oriented funds. Apollo and Franklin Templeton are financial backers of CAIS.

Speaking in the same ballroom that hosts the Golden Globes, Franklin Templeton Chief Executive Officer Jenny Johnson had a clear answer as to what makes it all worth it for her. “It kind of sounds funny, but we do God’s work,” she said. “We help people achieve the most important goals of their lives.”

Money managers want to offer investors every useful part of the market. With so much of the public markets driven by the performance of just a handful of megastocks, it’s easy to see why a push for diversification would be appealing. But large swaths of private markets are yet to be tested through a downturn, along with ordinary investors’ willingness to stick with them when their lifetime savings are at stake. If private investments are a new asset class that investors can believe in, it’s up to the evangelists to prove it. —With Rene Ismail

Scigliuzzo is chief correspondent for private capital at Bloomberg News in Los Angeles.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Davide Scigliuzzo