The S&P 500 Index is in the midst of a tug-of-war. Companies are beating earnings per share estimates by significant margins and are set to deliver impressive 12% growth this reporting season. But the White House’s chaotic approach to policy and concerns about the future of the software industry are combining to dampen enthusiasm for many erstwhile hot growth stocks.

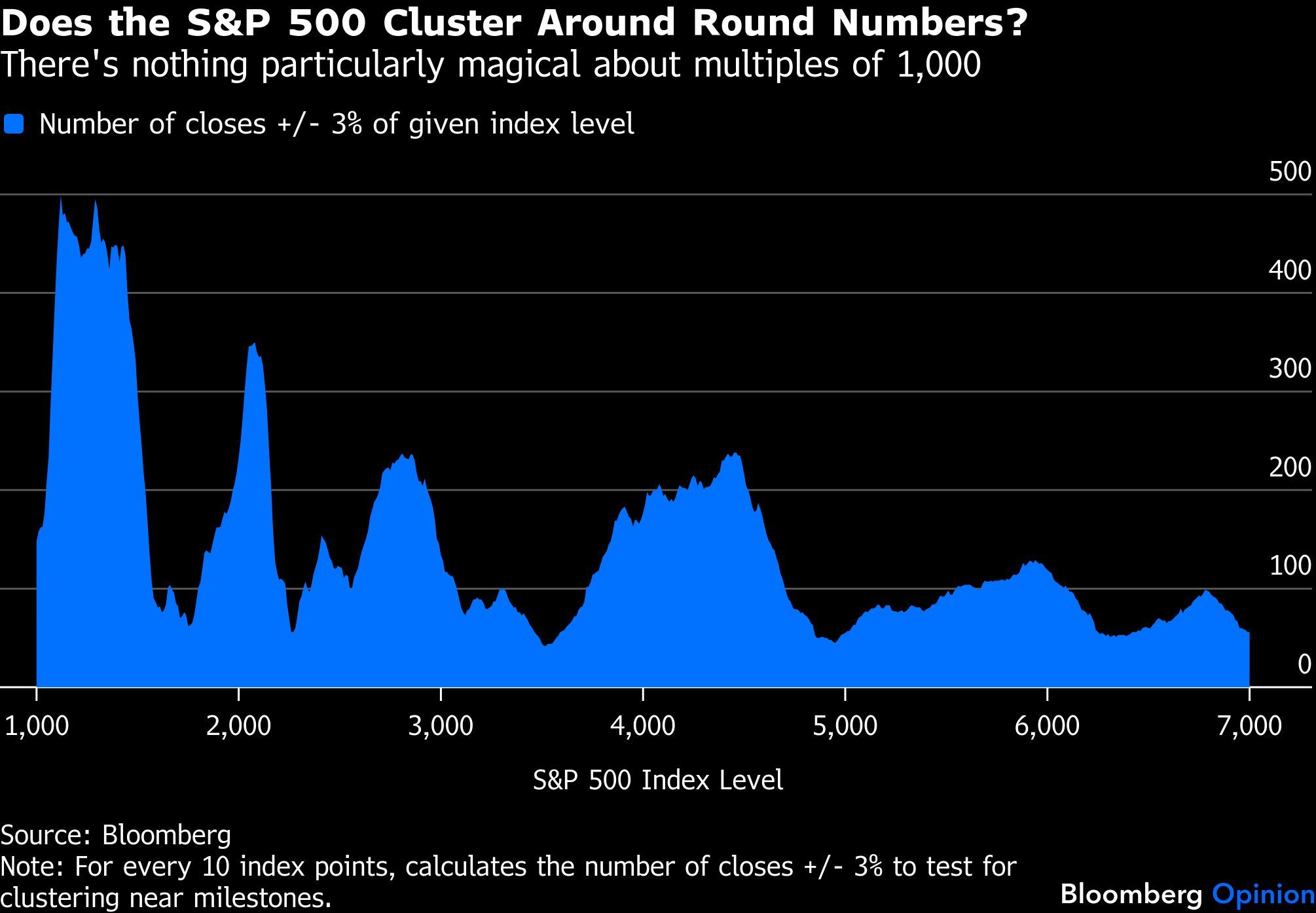

The outcome? The index has struggled to break through 7,000 since it made its first approach in October. More and more, its sideways shuffle is taking on the look of a coiled spring (or maybe it’s a ticking timebomb). In the near future, expect more volatility of the variety that investors experienced this week as this tension tries to resolve itself.

In the second year of his presidency, Donald Trump has further embraced his habit of delivering market-moving policy surprises, often via social-media pronouncement. Among other things he’s done in 2026, he has arrested the leader of Venezuela; hinted at regime change in Iran; threatened to raise tariffs and then retreated; attacked credit-card companies over interest rates; lambasted institutional investors for their role in the single-family housing market; and issued a warning to defense contractors who conduct share buybacks or pay dividends.

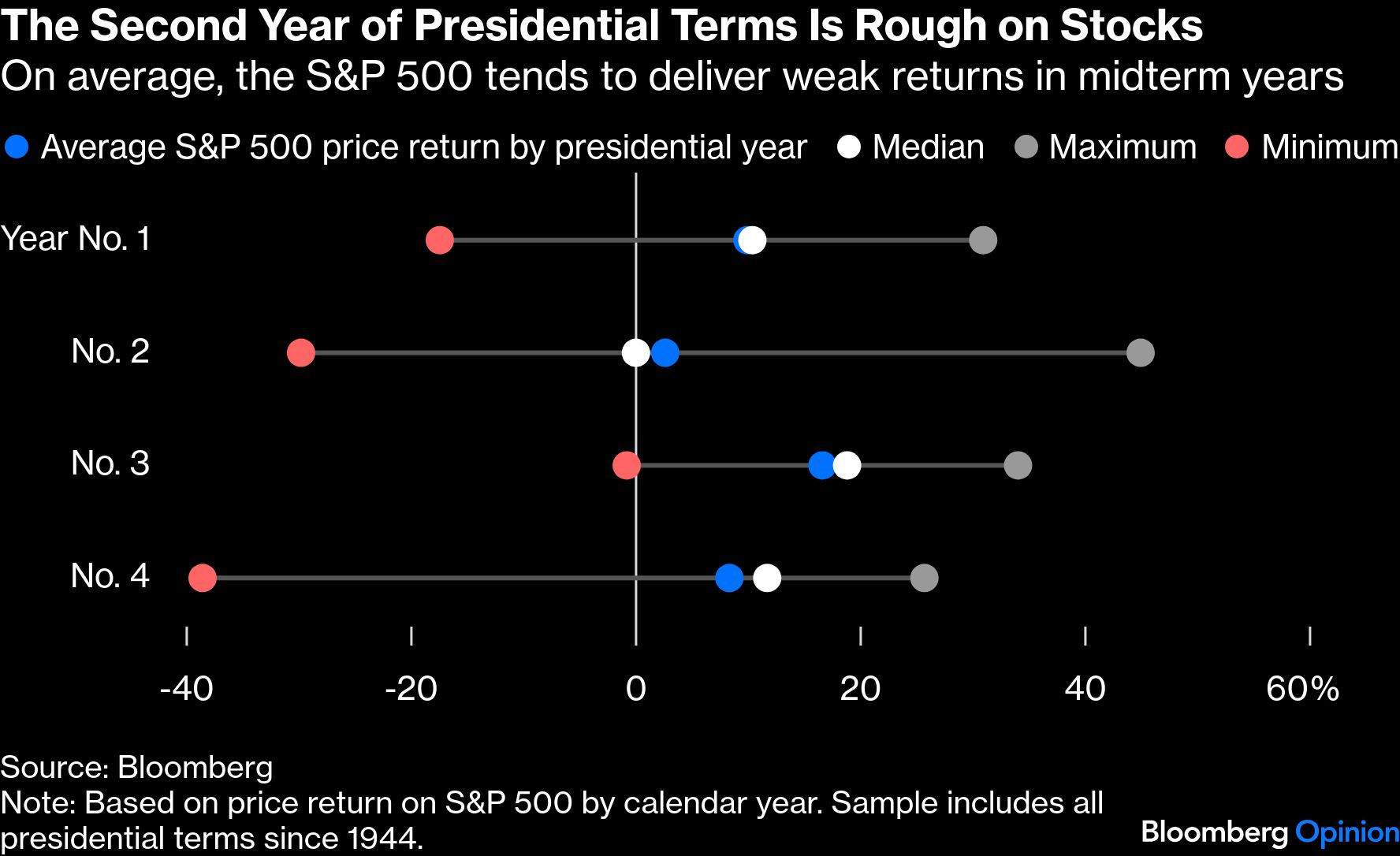

Some of this was to be expected. On average, the second year of a presidential term tends to be the worst one for US stocks: After all the big first-year promises, investors tend to temper some of their optimism as second-year presidents, under pressure to help their parties in midterm elections, sometimes crank up the populist rhetoric.

But Trump has taken this tendency to an extreme. Back in 2018, he used the second year of his first presidency to ramp up the trade war with China and attack the Federal Reserve. This year, he’s doing all that and more. Meanwhile, his nomination of Kevin Warsh, a long-time monetary policy hawk who has pledged to shake things up as future Fed chair, is introducing additional questions about how the US central bank will conduct itself.

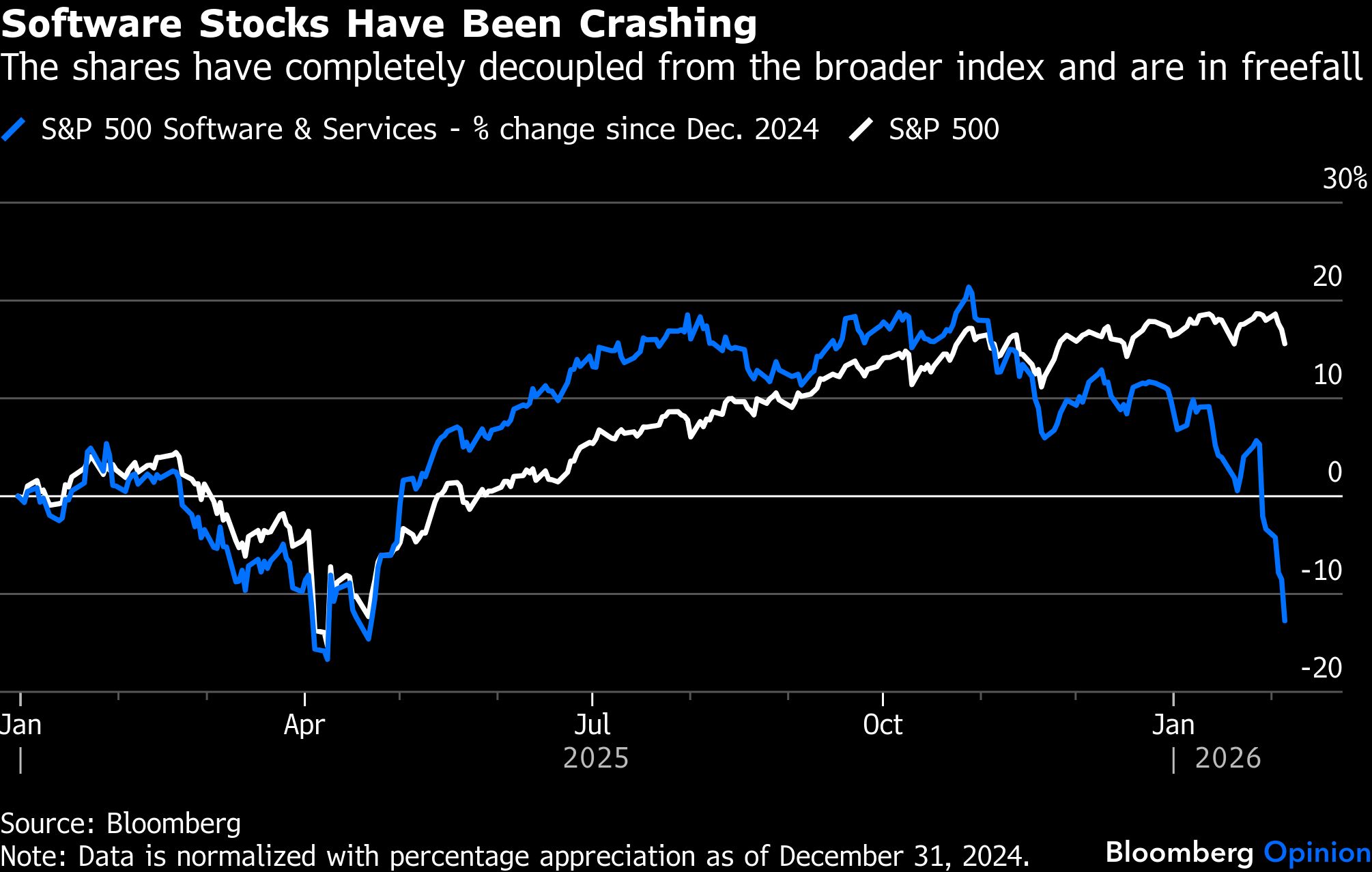

On top of all this, investors are becoming jittery about software stocks. For the past decade, subscription-based enterprise software companies have been regarded as cash cows, and they were initially seen as potential beneficiaries of the artificial intelligence revolution, leaving them with stretched valuations at the end of 2025. Recent developments have investors entertaining the possibility that AI might be able to replace some enterprise software products — an idea that picked up steam after Anthropic PBC launched a new AI automation tool.

In the near-term, it’s hard to find any real fire behind all the smoke: Analysts still expect software and services earnings per share to expand around 13% in 2026. That hasn’t prevented traders from driving the S&P 500 Software & Services Industry Group down by 20% this year (the drawdown now stands at 28% from the October high.) The swiftness of the collapse has echoes of other narrative-driven sell-offs, including the bear market crashes in regional banks and real estate investment trusts in 2023. And while those stocks have since recovered, bearish narratives kept them in investor purgatory for the better part of a year.