Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The January 2026 Bloomberg article, “Japan Bond Meltdown Sends Yields to Record High on Fiscal Fears,” is one of many headlines warning that Japan’s abrupt interest rate increase is an omen of dire trouble. While that may be the case — given decades of economic woes, declining demographics, and extreme levels of outstanding debt — we hold an alternative view.

Might the recent sharp rise in Japanese yields simply reflect the normalization of its economy, inflation, and interest rates following decades of stagnation and aggressive monetary and fiscal policies?

Whether you follow Japan or not, its situation is incredibly important for investors because it is a major provider of global liquidity. Instead of being overly dramatic about the slim chance of a near-term Japanese crisis, we prefer to focus on how Japan normalizes policy after years of artificially suppressed interest rates and how that process will impact the yen carry trade.

Japan’s Lost Decades

To help appreciate Japan’s current situation and why some pundits claim it is near the end of its fiscal line, we will recap Japan’s plight.

In "Japan’s Lost Decades," we explained that Japan’s prolonged stagnation traces back to the collapse of one of history’s largest asset bubbles in the late 1980s. Enormous real estate and stock market valuations imploded, leaving banks burdened with bad loans.

“From 1956 to 1986 land prices in Japan increased by 5000% even though consumer prices only doubled,” Ben Carlson wrote in “The Biggest Asset Bubble in History.” At its peak, the Nikkei stock index P/E ratio was close to 70.

The government chose to support failing banks and extend the economic pain over decades through massive spending and near-zero interest rates rather than endure a short-term, deeper contraction.

This response contributed to a fragile financial system with “zombie” banks, suppressed lending, and a private sector unable to drive robust growth, leading to deflationary pressures and very low economic growth for decades.

Demographics and structural factors have compounded the issue. Japan’s population is aging and declining, while minimal immigration dampens labor force growth and consumption, making growth harder to achieve.

Japan Removes Its Financial Support

Prior to the last few years, Japan experienced decades of economic malaise. The post-WWII economic boom was spectacular, and the ensuing correction was equally stunning.

A recent uptick in inflation, GDP, and interest rates has allowed Japan to gradually remove the monetary policy crutch that has supported its banks, economy, and financial markets for decades. This primarily entails the Bank of Japan (BOJ) reducing its balance sheet and letting interest rates gravitate toward normal market levels.

Some investors watching the sharp increase in interest rates warn that rising rates signal a default risk. Others, including us, think this is the normalization process.

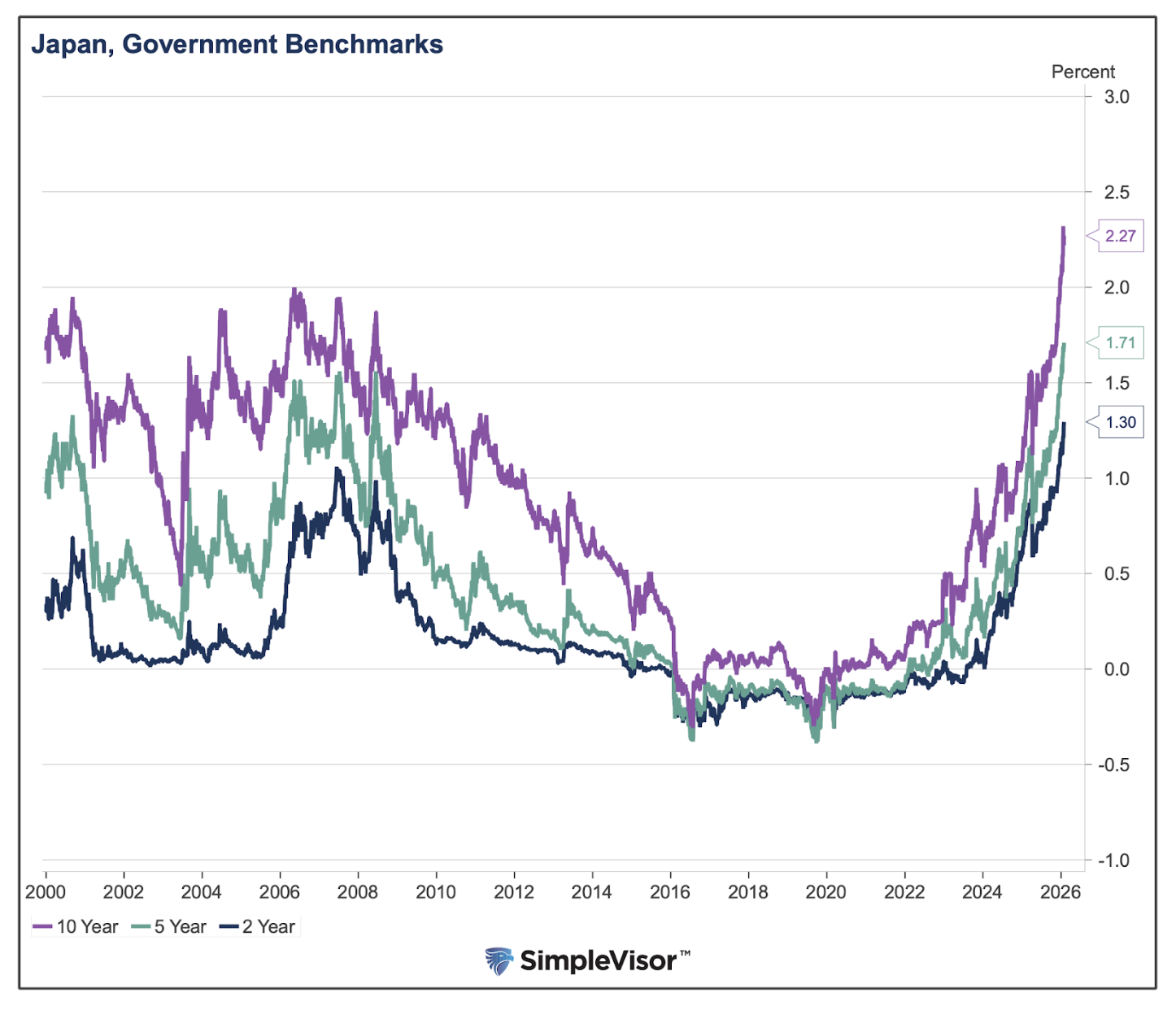

The first graph below shows the current benchmark interest rates for Japanese two-year, five-year, and 10-year bonds.

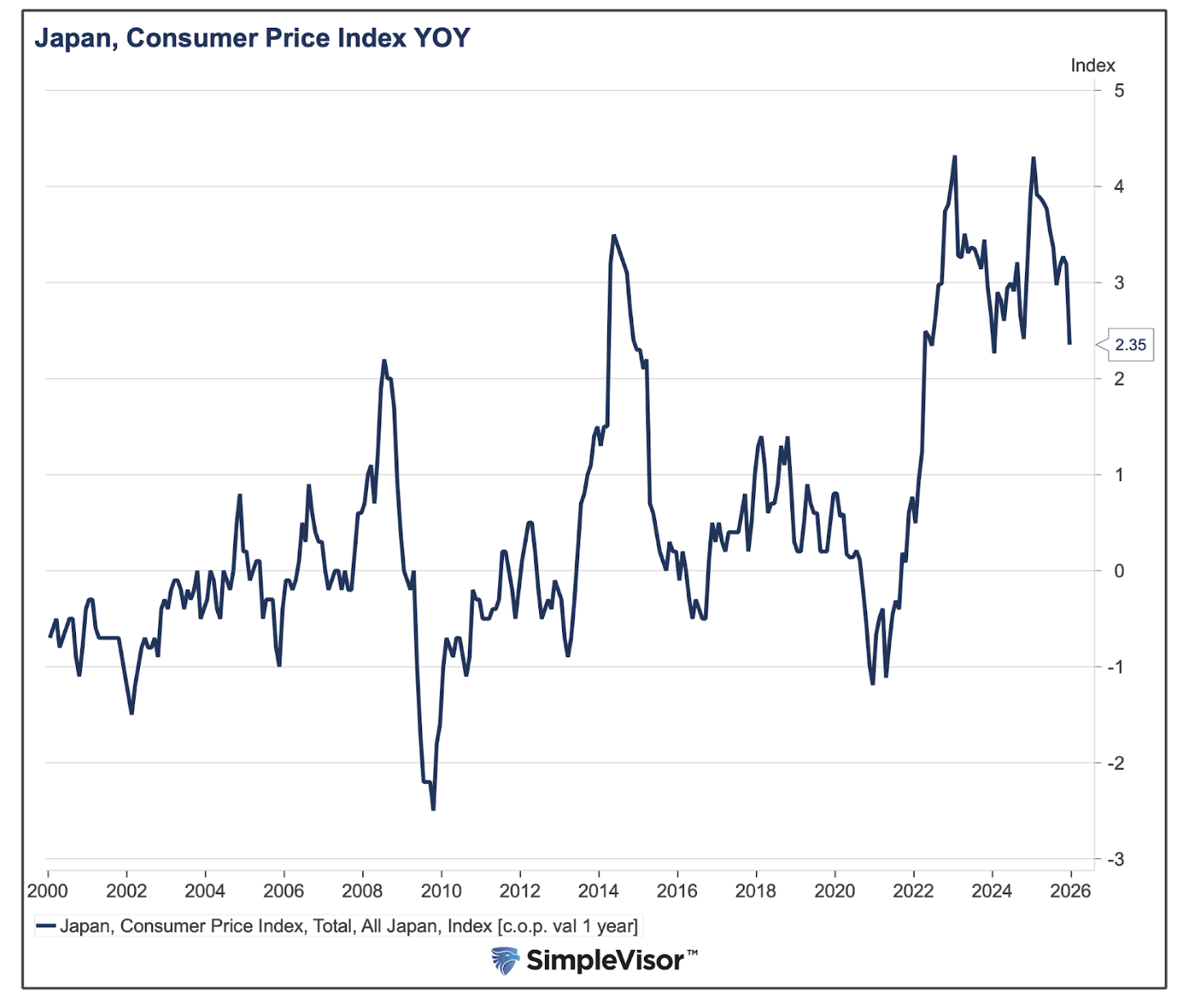

The recent increase in interest rates from negative levels is significant. The next graph shows that the inflation rate has recently been much higher than in the pre-pandemic era.

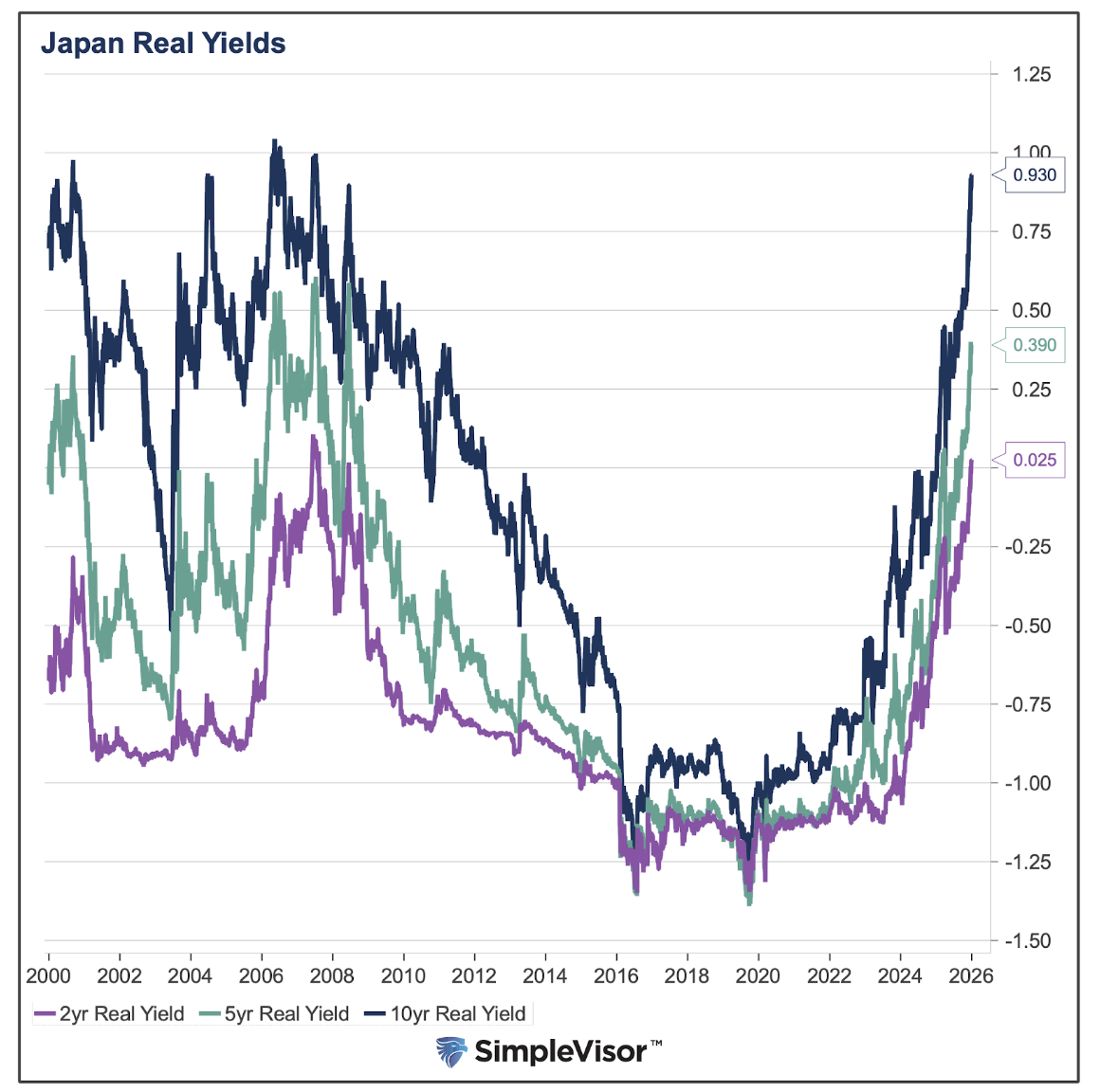

Next, we combine the two graphs to arrive at real (inflation-adjusted) yields. As shown, the two-year, five-year, and 10-year real yields are below 1%, albeit well above the -1% real yields that persisted from 2016 to 2022. They are now in line with the pre-financial crisis period.

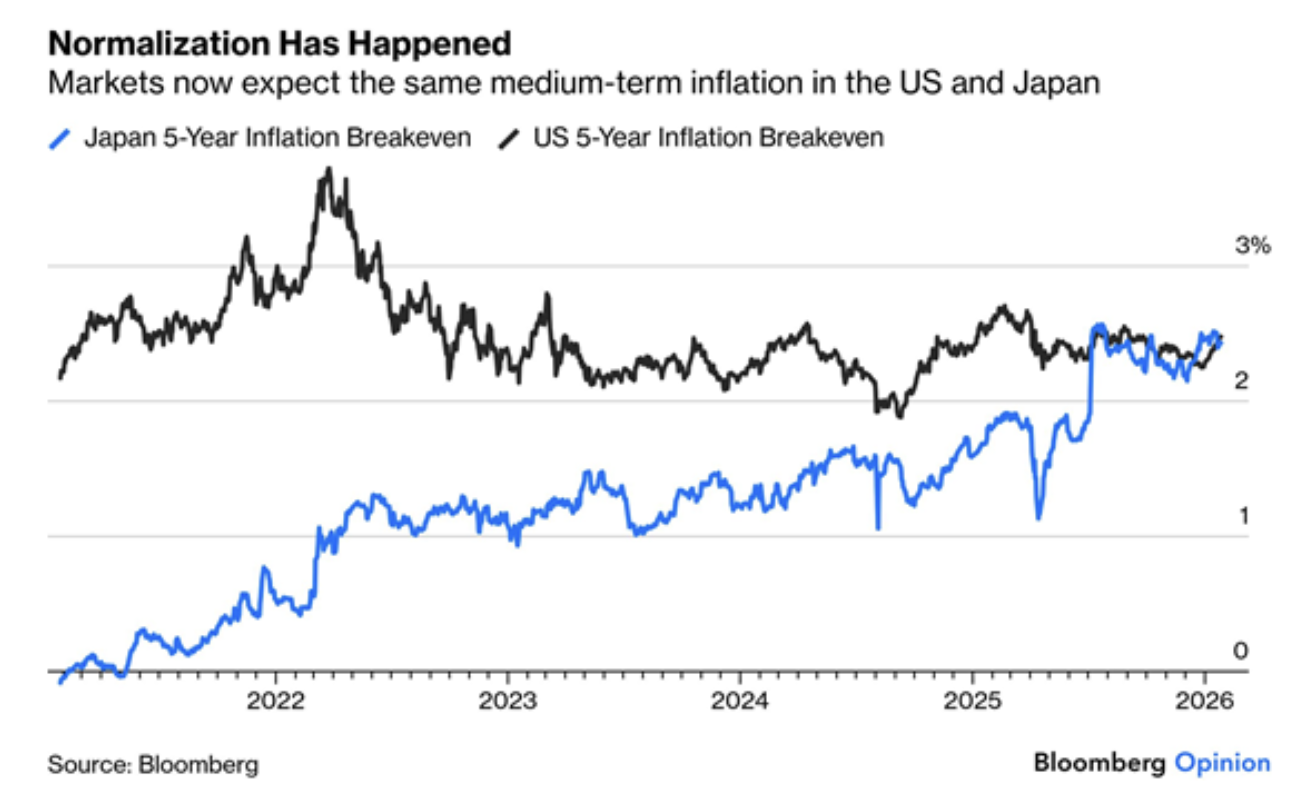

The takeaway from the three graphs is that Japan has allowed yields to gravitate toward a normal spread relative to inflation. The next graph provides global context: Inflation expectations are very similar for Japan and the U.S. However, Japanese yields remain about 2% below U.S. Treasury yields.

The charts signal that Japanese interest rates and inflation are moving toward levels more in line with those of other large economies.

Economic Signs of Normalization

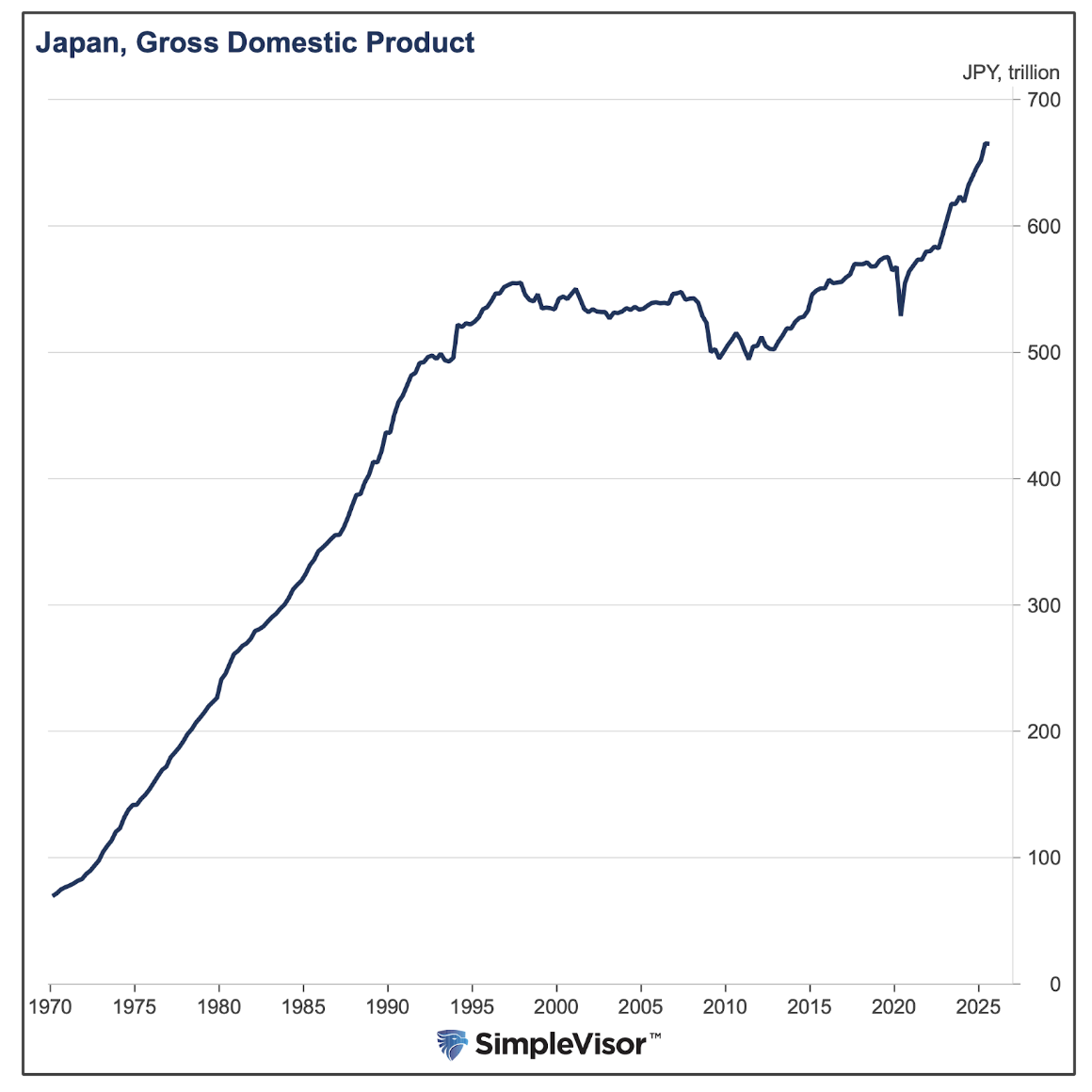

The normalization argument is further supported by a recent spurt in economic activity. The graph below shows Japan’s economy was stagnant for 23 years (1997–2020); however, economic activity has accelerated in earnest since the second half of 2022.

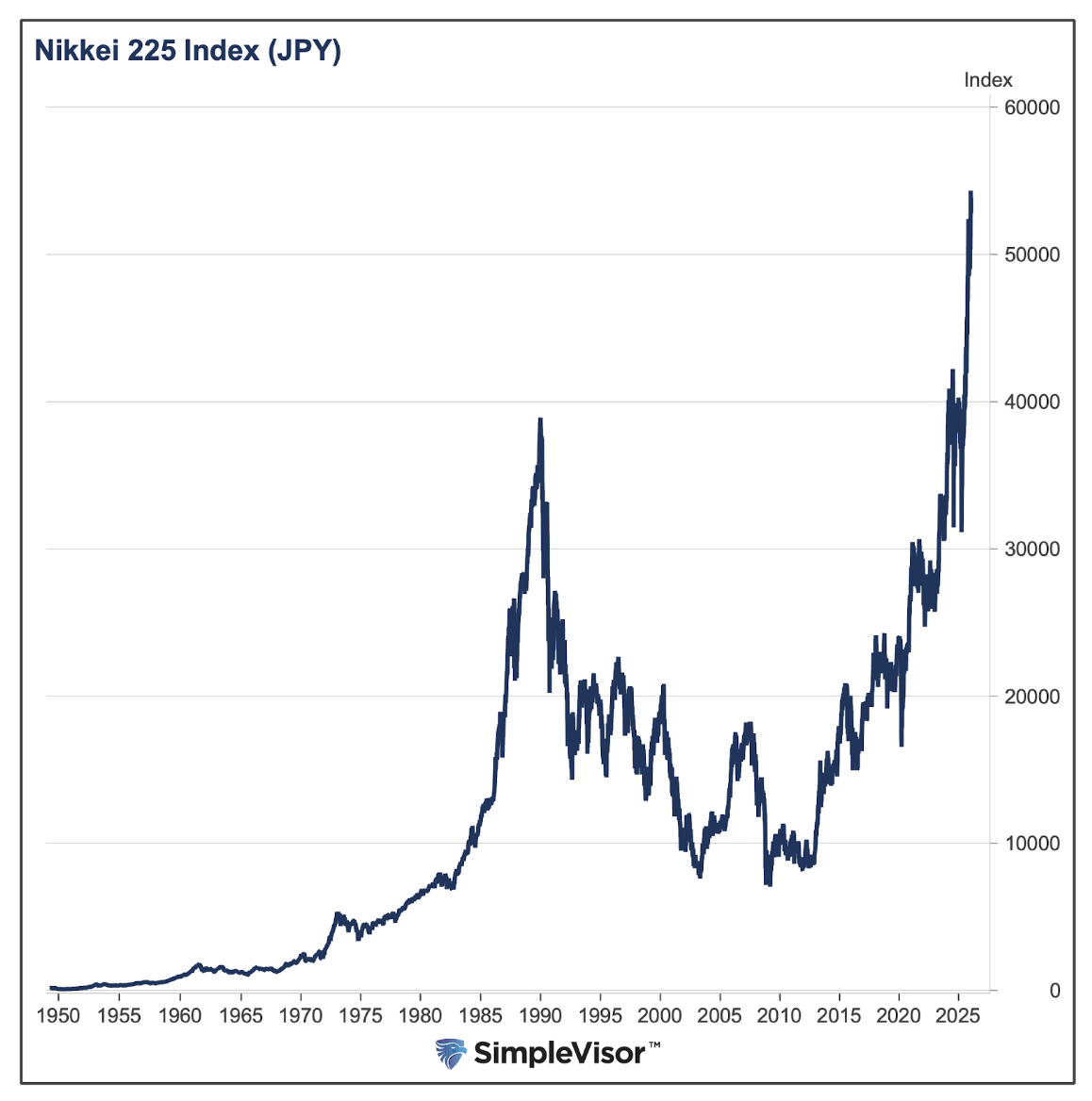

Furthermore, the Nikkei 225, Japan’s primary stock index, recently broke new record highs, finally eclipsing the prior peak seen at the end of 1989.

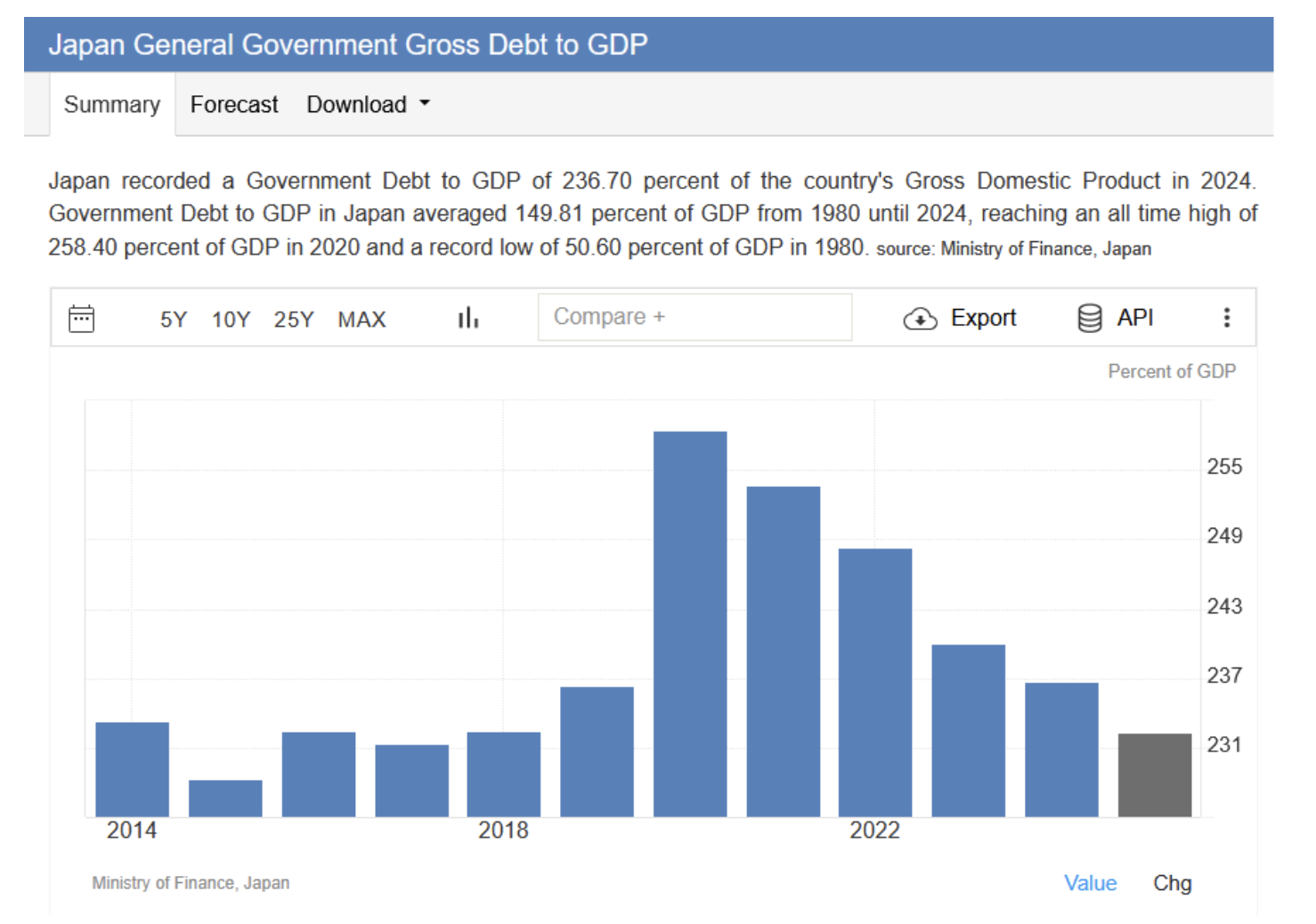

Lastly, Japan’s debt, while rising nominally, is falling as a percentage of economic activity. As we show below, its debt-to-GDP ratio peaked at 2.58x and has since moderated to 2.32x. It remains exceptionally high, but it is trending in the right direction. For context, the U.S. debt-to-GDP ratio stands at 1.21x, which is considered problematic by some economists.

Japan Is in a Pickle

Normalization after years of significant fiscal and monetary stimulus will not be easy. The public, accustomed to near-zero inflation, is growing uneasy with rising prices and calls for fiscal austerity. Policymakers are being forced to decide between economic growth and inflation.

Policymakers could contain inflation by raising interest rates and implementing fiscal austerity, thereby resulting in yen appreciation. The risk is that they reduce economic growth in the process. Conversely, they could keep rates at current levels and increase fiscal spending, as some politicians want, but risk that inflation keeps increasing.

As if that decision isn’t hard enough, they must also manage interest rates to accommodate the funding of Japan’s massive debt. As we noted earlier, Japan has a debt-to-GDP ratio almost twice that of the U.S. Higher interest rates increase the government's interest expense. In turn, they must issue more debt to fund existing debt. This is the “trap” noted by Japan’s bond vigilantes.

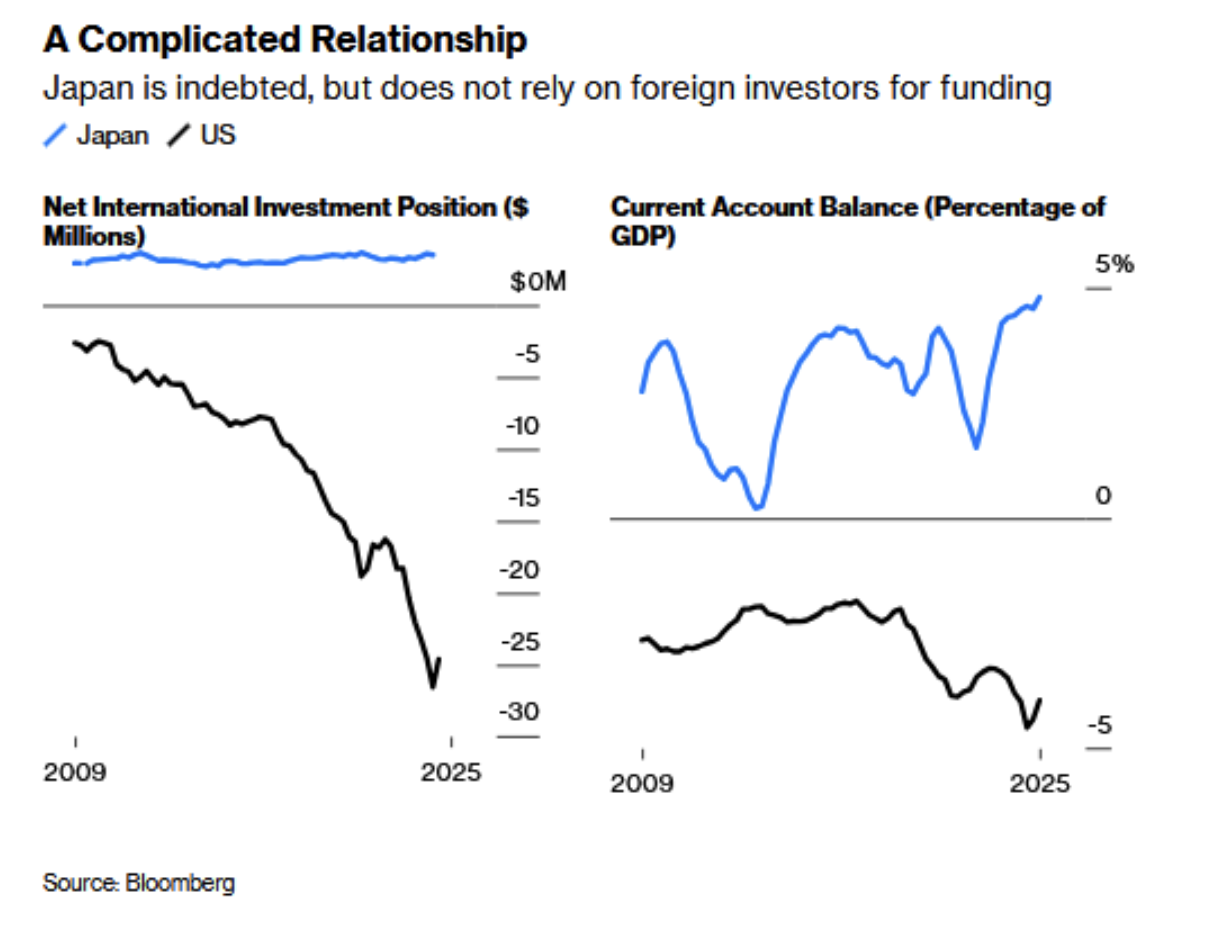

However, Japan’s debt situation is not identical to that of the U.S. John Authers of Bloomberg recently reminded us why Japan can maintain higher levels of debt than most other countries. Per his missive, "Japan Needn’t Drive An International Crisis":

Another key argument against a crisis is that, despite its huge pile of debt, Japan is stable. It maintains a current account surplus (unlike the US). Also, unlike the US, it has a positive net international investment position, meaning that it holds more foreign assets than foreigners hold assets in Japan:

Further, he argues:

Moreover, fears of an imminent fiscal accident appear overstated. Political constraints may limit aggressive fiscal expansion, the primary deficit has been shrinking, and authorities retain extensive tools to manage yield volatility. Unlike sudden crises driven by foreign capital flight, Japan’s challenge is one of gradual adjustment, not sudden loss of confidence.

Global Liquidity: The Yen Carry Trade

The most important aspect of Japan’s normalization is its impact on global liquidity through the yen carry trade. Here is a basic example of how it works:

- A U.S.-based hedge fund borrows ¥15.3 billion ($100 million) at 0.75% for one month.

- They convert the yen to $100 million and purchase U.S. assets (for example, shares of IBM.)

- The profit depends on the borrowing cost (0.75%), the change in the yen-dollar exchange rate, and the asset’s price change.

Recently, borrowing costs in Japan have risen but remain well below U.S. rates. Despite higher rates, the yen has depreciated against the dollar, which has benefited the carry trade, offsetting higher interest costs. However, a rapidly appreciating yen can easily offset the interest rate differential, making the yen carry trade less favorable.

If Japan can gradually normalize its interest rate and support its currency with minimal volatility, the yen carry trade can unwind in a market-healthy fashion. But, as we saw in 2024, sudden shocks to the yen can trigger a swift reversal of the carry trade, harming global stock and bond markets.

Summary

In our opinion, Japan’s rising yields and currency volatility reflect an economic normalization. We do not think Japan is on the verge of fiscal collapse. However, the transition from a monetary- and fiscal-policy-dependent economy to a free-market economy could significantly affect a major source of global market liquidity. Policy decisions that cause sharp, sudden changes in rates and/or the yen can have a notable effect on stock and bond markets worldwide.

We witnessed this in August 2024, when the BOJ unexpectedly raised rates; the Nikkei 225 fell by over 12% in one day, and the S&P 500 corrected by 6% shortly after. We trust policymakers will aim for a smooth normalization process, free of market shocks, but their endeavor to return to a free-market economy entails significant risks for both Japanese and global markets.

Michael Lebowitz is a portfolio manager with RIA Advisors and author for Real Investment Advice. For more information, contact him at [email protected] or 301.466.1204.

Join RIA Advisors and elevate your career within a deeply experienced team focused on innovation. Our collaborative environment is built on a foundation of advanced technology and effective investment models, designed to enhance your ability to serve clients and grow your practice. Benefit from a supportive culture that encourages professional development and fosters a forward-thinking approach. By joining our team, you’ll be part of a group dedicated to excellence and continuous improvement, empowering you to focus on building meaningful client relationships and pursuing your business ambitions. Discover the advantages of working with our accomplished advisory team by starting your conversation today.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more articles by Michael Lebowitz

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.