Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

A picture is worth a thousand words. What follows, instead of 7,000 words, are seven illustrated examples of what could go wrong with the U.S. stock market or the economy.

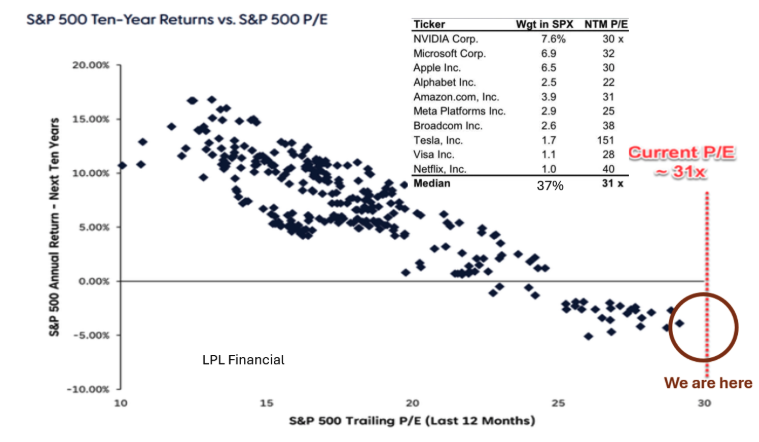

1) U.S. stocks are very expensive and dominated by just a few names.

The stocks known as the Magnificent Seven and a few other companies are disproportionately large relative to the rest of the domestic stock market. A significant downturn among them could easily result in a marketwide crash.

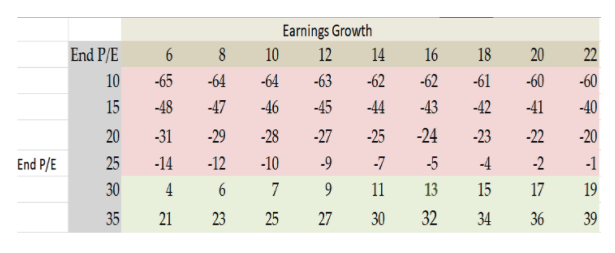

2) Earnings growth won’t save the market.

If P/Es contract below the current 30, stocks could lose more than 60%, as shown in the table below, which depicts expected returns based on ending P/E and earnings growth. If P/Es contract to just 25, the market would need earnings growth of more than 22% to just break even.

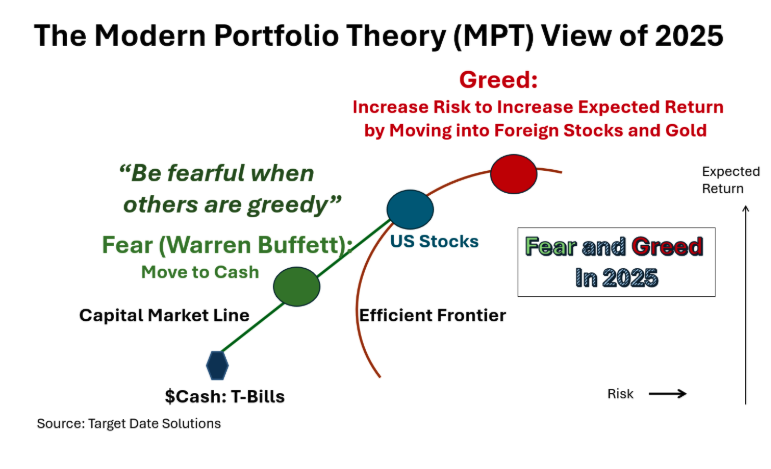

3) Fear and greed are tugging investors in opposite directions, representing two distinctly different strategies that appeal to very different types of investors.

Berkshire Hathaway’s Warren Buffett advises, “Be fearful when others are greedy, and greedy when others are fearful.” Right now, greed is driving investors into foreign equities and gold, while fear is pulling them into cash or cashlike investments.

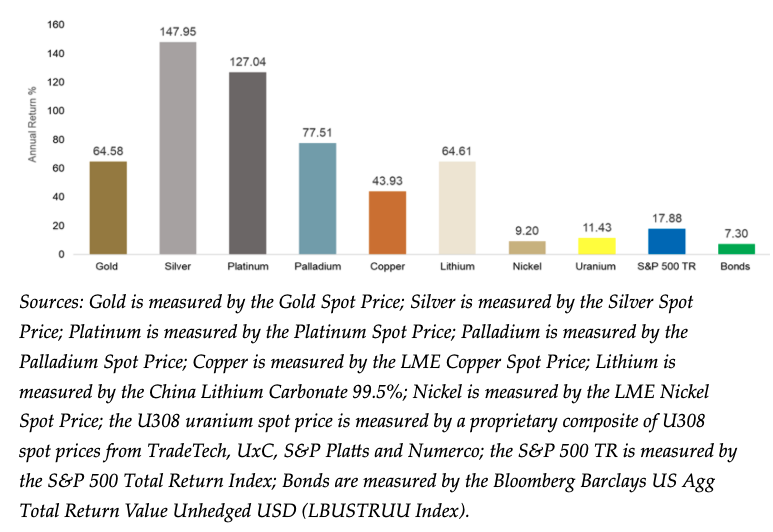

4) Precious metals did well last year, with assets flowing in due to early inflation fears. However, greed drove much of the later inflow.

A recent meltdown in gold and silver, sparked by the nomination of Kevin Warsh to the Fed, erased some of those gains. It seems to be reversing itself, at least partially.

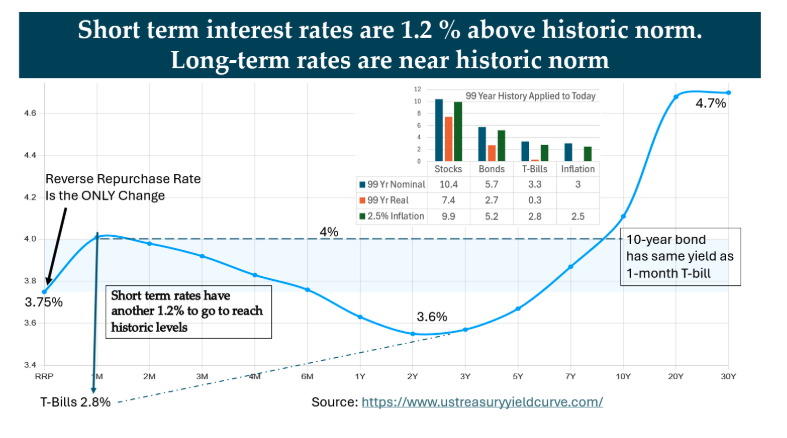

5) There’s plenty of room to lower interest rates to stimulate the economy.

The current effective federal funds rate is sitting at around 3.64% after a series of cuts in the latter months of 2025. Despite that, they’re still nowhere close to the near-zero rates of just a few years ago. Over the past 100 years, T-bills have averaged 0.3% above inflation. So, with inflation at 2.5%, T-bills would yield 2.8%, which is 1.2% below the current 4% rate.

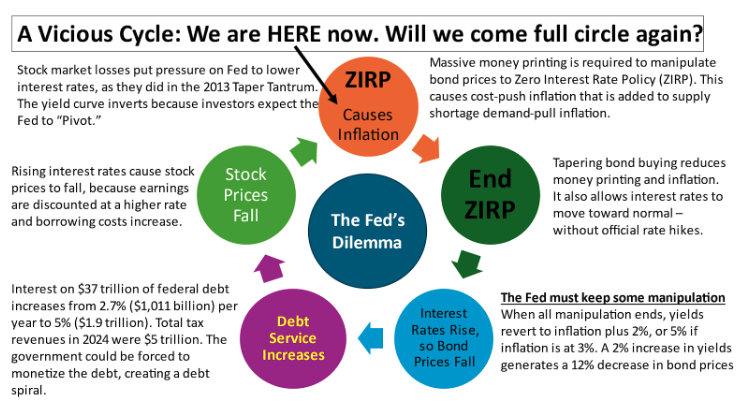

6) Does the economy need stimulation or moderation?

Each loop through the cycle is more dangerous than the last, causing the debt to balloon even further.

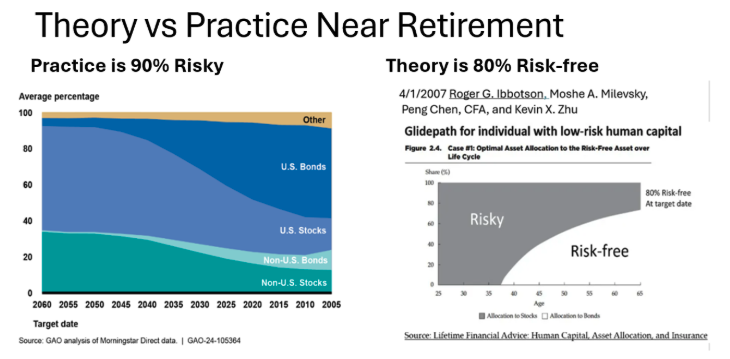

7) Baby boomers in target date funds are not protected against the next crash.

The allocations of such funds are far riskier than theory dictates.

Conclusion

I have been warning my readers about these dangers for a long time, thus earning my reputation as a permabear. You can judge whether my concerns are warranted.

If you decide to act, it’s worth noting the two distinct strategies that are currently in play. Many have moved beyond U.S. stocks, to precious metals and foreign stocks. Momentum might continue in these asset classes this year. On the other hand, Warren Buffett, prior to stepping down as CEO of Berkshire Hathaway, moved most of the firm’s assets in the opposite direction — to the safety of cash.

In other words, risk-on and risk-off are both in play. Baby boomers should choose risk-off at this point in their lives because they are in the retirement risk zone, when the sequence of return risk can literally ruin the rest of their lives. However, they might more safely choose risk-on if they’re beyond the risk zone, which is five years into retirement.

Younger people didn’t feel the crash of 2008, so they don’t know what risk is. Risk-on is a likely choice for them, and with their longer time horizon to retirement, they can generally afford this choice.

Ron Surz is president of Target Date Solutions, developer of the patented Safe Landing Glide Path and Soteria personalized target date accounts. He is also co-host of the Baby Boomer Investing Show. Surz’s passion is helping his fellow baby boomers at this critical time in their lives when they are relying on their lifetime savings to support a retirement with dignity, so he wrote a book, “Baby Boomer Investing in the Perilous 2020s,” and he provides a financial educational curriculum.

For anyone who relies on TDFs — or advises those who do — Surz’s new book is a must-read guide to understanding the risks, solutions, and future of a secure retirement.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more articles by Ron Surz

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.