Alphabet Inc. has this week embarked on the next leg of its debt program to meet the voracious funding needs of its artificial intelligence program. Nothing quite signifies global domination like issuing bonds with ease across all of the world’s major bond markets and at a range of maturities, including the ultra-long arena that’s typically reserved for the most favored of borrowers.

Monday saw Google’s parent successfully raise $20 billion in a multi-tranche issue, following the November sale of US debt worth $17.5 billion and an additional €6.5 billion ($7.8 billion) denominated in euros. Several issues in Swiss francs and British pounds followed on Tuesday, raising the equivalent of a further $11 billion. Alphabet now has bonds outstanding that offer a liquid yield curve across major currencies, enhancing the attractiveness of its debt to investors, which in turn will likely reduce its funding costs, make it a benchmark versus other corporates and even offer a useful diversification from government debt.

Alphabet enjoys a very strong AA+ investment grade rating from S&P Global Ratings, helped by cash on its balance sheet of more than $125 billion. Although relatively new to the debt capital markets, it's exploited its Magnificent Seven status — and its market value of almost $4 trillion — perfectly in crafting its borrowing strategy.

A 100-year £1 billion ($1.4 billion) sterling tranche is this week’s standout transaction. It's quite the statement for a tech company to find buyers for such a long-dated bond; previously, only Oxford University and the Wellcome Trust charity have ventured this long in sterling. Not even the UK government issues this far out as there isn't consistent investor demand from pension funds and life insurers to build a liquid part of the yield curve. Although Motorola Solutions Inc. sold a dollar century bond in 1997, the telecom company’s issue was a minnow worth just $300 million, and with only half of that amount currently outstanding it's long faded from memory.

Alphabet’s century-long security was priced at 120 basis points over the longest-dated 2073 gilt, offering a yield of just over 6%. The order book was worth almost £10 billion, illustrating what appears to be huge demand, but allocations are unlikely to be distributed to all of those who expressed an interest; the lead managers of the sale will make sure the bulk is placed with long-term holders, and the deal will probably not trade much.

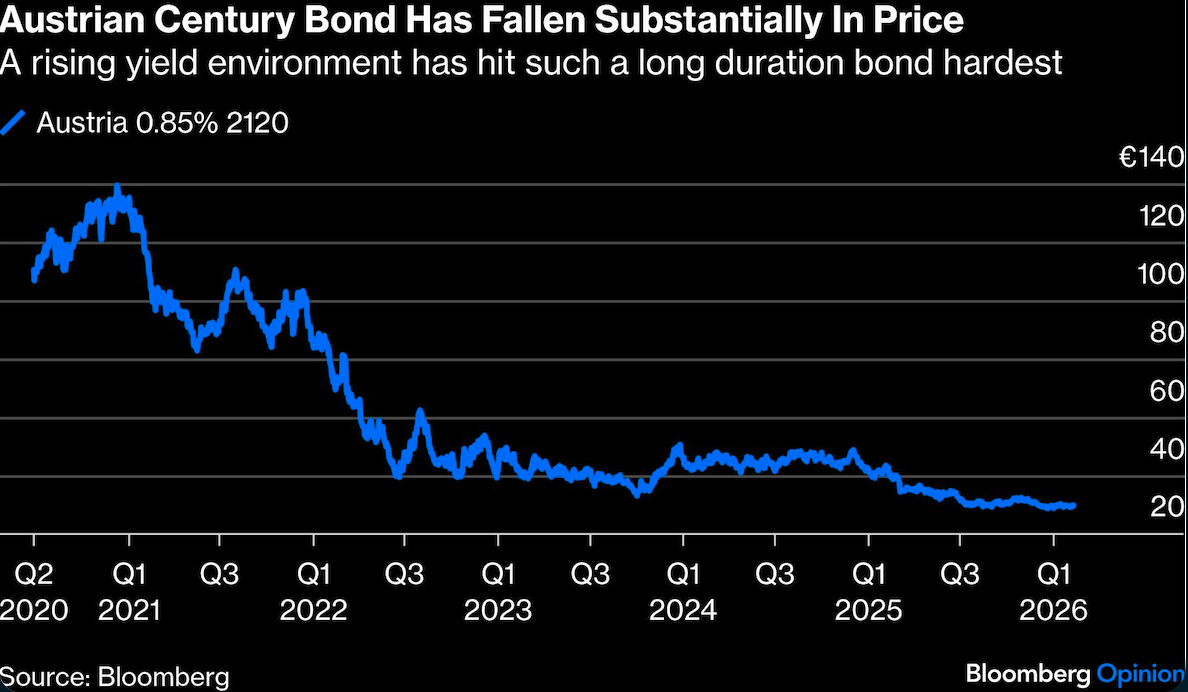

The Republic of Austria has issued ultra-long deals over the past decade, including the 0.85% of 2120 that’s been tapped several times since its initial sale in 2020 and now stands at €5.8 billion. Although the credit rating is the same as Alphabet, these sovereign bonds are not comparable in terms of the bond math. Austria was issuing when prevailing interest rates were much lower, and have performed poorly as a result to currently trade at below 30% of face value.

The Austria century bond has a much longer duration because the low annual coupon payments make up less of the overall cashflow return versus the principal repaid at maturity. The Alphabet sterling deal will have a coupon more than six times higher. Using the most powerful force in the universe — the power of compound interest — at constant yields, it will pay investors back in fewer than 17 years, whereas the Austria issue's coupon payments will never fully match the principal.

Buyers of these types of security are looking to dynamically balance the risk of an entire portfolio rather than caring about annual coupon weights. Ultra-long debt allows portfolio managers to barbell their duration needs by buying more 10-year liquid debt rather than illiquid 20- to 50-year maturities. it's likely the investors will both be reinsurance companies, which have far longer duration needs than life insurers, or final salary pension funds. The Alphabet deal may well have been sought out in advance by reinsurers looking for such rare assets, which greatly improve balance sheet capital relief under EU Solvency II regulations.

With annual investment expenditure on AI likely to soak up at least half of its annual revenue of around $340 billion, it’s clear that Alphabet will keep coming back to the bond market for more. Investors have every reason to take strong interest in a high-end credit with major growth plans promising investment returns way in excess of the cost of its debt servicing. In the world of fixed income world, Alphabet is a vanishingly rare beast amid the herd of indebted sovereigns.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Marcus Ashworth