Sell first, ask questions later. That was the stock market’s response to last week’s new artificial-intelligence tools that challenge the software, legal data and media industries. But bargain hunters seeking victims of indiscriminate selling may need patience waiting for a recovery. Corporate beneficiaries on the other side of the trade — businesses that actually use AI to improve how they operate — could be the more lucrative opportunity.

Investors have been nervous for months about AI’s potential to threaten long-standing business models by giving customers a cheaper, or free, means of doing things they currently pay for. The threat became tangible last week when AI firm Anthropic PBC released add-ons enabling lawyers to use its Claude chatbot for reviewing contracts and other tasks without needing coding skills.

That had implications beyond companies providing law-based data services. Cue a broader sell-off capturing publishers, marketing groups and business-information providers. Vindicating the fears, Anthropic swiftly followed up with a product for finance professionals.

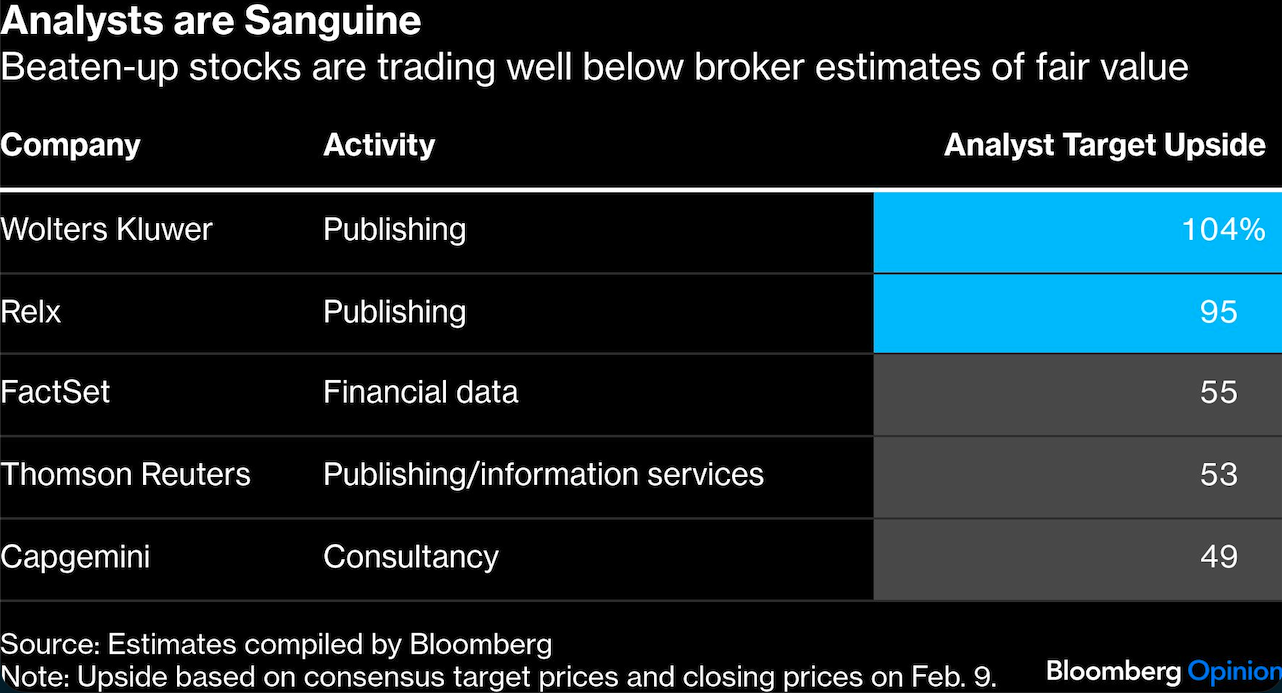

In the face of a sudden shock like this, investors have little time to sort winners from losers and will sell baskets of stocks exposed to the same theme. The modern market, denuded of active fund managers, may also overreact in either direction to specific pieces of information like Claude’s new “plug-ins.” And yet, one week on, much of the market damage persists. That’s despite equity analysts remaining bullish on some of the worst-hit stocks.

The difficulty this cohort of companies faces is proving a negative: showing that their earnings won’t be hurt by the AI competition. Relx Plc, one of the legal publishers at the center of the concerns, illustrates the problem. It owns an authoritative database of case law and appeal judgments that would be incredibly hard for a new entrant to replicate. The stock’s price-to-earnings multiple soared between 2021 and 2025, partly on the idea that AI could create new markets for that data. Over the last year, this has more than unwound as the stock halved. Ostensibly, it looks cheap.

But if analysts eventually end up cutting the company’s earnings forecasts, the rating won’t look so reasonable. And if Relx fails to capture the previously anticipated growth boost from AI, it would deserve a lower price-earnings ratio. The cast-iron way to rebut these fears is by delivering on the current profit forecasts. And that takes time.

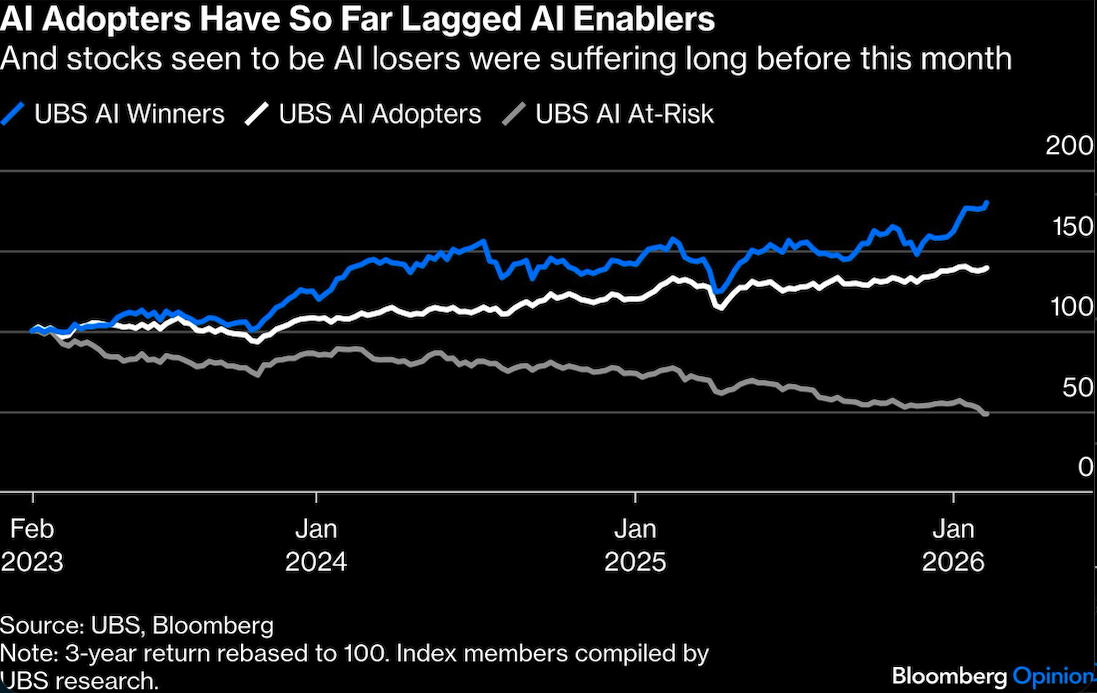

Now consider the flipside of the sell-off. If the market is even half-right to force down the value of software and related industries, the sectors’ customers must be set to make corresponding savings or productivity gains that should lead to lower operating costs or higher revenue.

It is these “AI adopters” who represent “the next phase of the AI opportunity,” according to strategists at UBS Group AG, who say that the theme has yet to catch the market’s full attention even though the use of this potentially transformative technology is accelerating. Instead, investors have been aggressively throwing their money at AI enablers, such as chipmakers and suppliers of kit to data centers, and punishing perceived losers.

If the big commercial law firms were publicly traded, their share prices would be a useful immediate readout for the other side of the “Claude trade.” But there are other potential beneficiaries in the listed universe. They include firms with “valuable data, large customer bases, complex processes and high regulatory burdens,” the UBS strategists argue.

The bank’s research points to financial services, retailers, health care and transport, where technology can support things like fraud detection, insurance-claims processing, personalized marketing, clinical diagnosis and logistics efficiency. In Europe, such companies include the likes of BNP Paribas SA, Tesco Plc, Siemens Healthineers AG and DSV A/S. French lender BNP already sets itself a “value-from-AI” target to calculate the financial boost from using the tech. This year it stands at €750 million ($893 million).

The trick for investors hunting these types of opportunity will be spotting genuine signs of progress in the numbers that corroborate management’s claims of AI-driven gains. Key metrics to look out for would be rising sales per employee and expanding gross margins. The wildcard is whether the productivity benefits of AI come through faster than economists expect.

Of course, one investment strategy amid the maelstrom is seeking out companies that just seem impervious to AI disruption because they’re fundamentally “old economy” businesses. There must, however, be some winners on the other side of the software market meltdown.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.