A quick scan of Pricefx’s website leaves little doubt how the company sees itself. “The #1 Leading Pricing Software” is splashed across its homepage. As is “Great Pricing Software Makes Dreams Reality.” In all, “software” appears more than a dozen times on that first screen alone.

One of Pricefx’s biggest financial backers prefers a different label, though. Sixth Street Partners, a top direct lender to the firm, classifies Pricefx not as software but as a “business services” company.

And so it goes in the world of private credit. Time and again, companies widely regarded as software firms are frequently labeled otherwise by lenders, a practice that raises fresh questions over the full extent of their exposure as the threat from artificial intelligence upends markets and rattles investors. Bloomberg News reviewed thousands of holdings across seven major business development companies — funds that pool direct loans — and found wide variation in how investments tied to the sector are categorized.

At least 250 investments, worth more than $9 billion, weren’t labeled as loans to software firms by one or more of the BDCs, even though the companies borrowing the cash are described that way by other lenders, their private equity sponsors, or the firms themselves. The discrepancies, market watchers say, underscore broader concerns about private credit, a famously opaque industry marked by inconsistent reporting standards, complex fee structures and significant discretion over valuation practices.

While the differences don’t necessarily signal an attempt to obscure exposure, they make it harder for investors to gauge sector concentration at a time of heightened scrutiny, according to Robert Dodd, an analyst at Raymond James Financial Inc.

“The software classification in a BDC schedule of investments is only going to include generally industry agnostic software — it understates the exposure to it as a business model, and it’s not negligible,” Dodd said. “Software is a theme in its own right, and that classification scheme breaks down even if historically it was helpful.”

A representative for Sixth Street declined to comment. In filings, the firm says it groups companies by end-market, meaning software isn’t shown as a standalone category, even as it acknowledges that “many of our portfolio companies principally provide software products or services, which exposes us to downturns in that sector.”

Bloomberg reviewed disclosure documents of BDCs overseen by Sixth Street, Apollo Global Management Inc., Ares Management Corp., Blackstone Inc., Blue Owl Capital Inc., Golub Capital and HPS Investment Partners. Across all of them, multiple companies considered software by at least one other lender were put in a different industry bucket.

‘More Responsibility’

While questions over how companies are categorized aren’t unique to private credit, the issue takes on added weight in a market already known for its limited transparency.

Because these loans are privately negotiated and thinly traded, there’s little independent price discovery or commonly referenced benchmarks to fall back on. The labels managers assign can therefore carry outsized importance, shaping how investors gauge sector exposure, concentration risk and vulnerability to shifts such as the rapid advance of AI.

It “puts more responsibility on the BDC manager to evaluate, value, and categorize these assets correctly,” said Michael Anderson, head of global credit strategy at Citigroup Inc. “These aren’t loans that trade publicly or sit in widely followed indices that investors can independently review.”

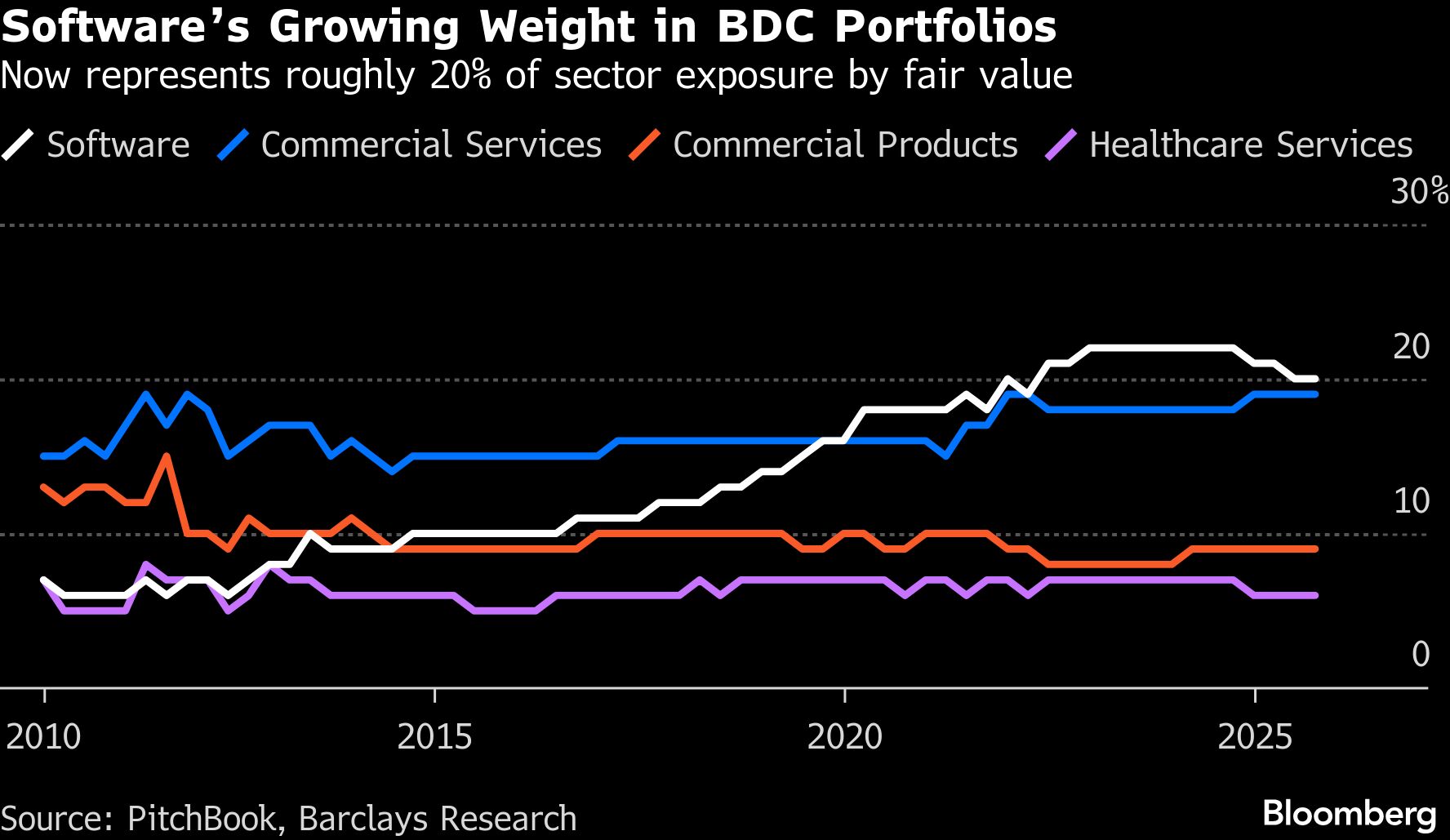

Drawn by predictable revenue streams, alternative asset managers piled into software for more than a decade. Industry executives have been forced to address investors’ questions about this concentration on recent earnings calls. Apollo President Jim Zelter said earlier this month that about 30% of private equity firepower went into the industry during the period, and that software also accounted for roughly 40% of all sponsor-backed private credit.

Barclays Plc estimates software now makes up about 20% of all loans held by BDCs, making it their largest sector exposure. By comparison, software makes up about 13% of the US leveraged loan market, according to Morningstar LSTA index data.

Blurry Lines

Angst about the future of the software business has escalated rapidly — and hit the stock and credit markets hard — after the AI startup Anthropic PBC released a series of new tools that threaten everything from financial research to real estate services. The S&P North American software index has posted daily declines of more than 4% three times in the past few weeks, and is down more than 20% this year.

What even qualifies as “software” isn’t always clear-cut.

Apollo, for example, categorizes Kaseya, a self-described “IT management software” company, as “specialty retail” in filings. Other lenders, including Blackstone and Golub, place it in the software bucket.

Restaurant365, which calls itself a “back-office restaurant system software” provider, is labeled as “food products” by Golub. That puts it alongside companies such as Louisiana Fish Fry and the maker of Bazooka Bubble Gum. Ares groups the company with its software and services holdings instead.

Representatives for Apollo, Blackstone, Golub and Ares declined to comment.

“It’s clear that lenders face challenges in placing a given investment neatly into a single sector,” said Corry Short, a strategist at Barclays. “Some BDCs classify investments by end market, while others classify by the issuer’s primary sector. This inconsistency can make it difficult to compare software exposure across the space.”

In some cases, inconsistencies arise within a single firm.

At least four companies in Blue Owl’s largest publicly traded BDC, Blue Owl Capital Corp. (which trades under the ticker OBDC), are classified under categories including “chemicals,” “infrastructure and environmental services” and “business services,” yet are labeled as “software” in its technology-focused fund, Blue Owl Technology Finance Corp.

“Our job as a manager is to provide information in a consistent way so investors understand the risk that they are taking,” a spokesperson for Blue Owl said. “Each of our funds has a different investment strategy, so the industry classifications can differ.”

Some say private credit managers may face increasing scrutiny over how they define and disclose their holdings as AI reshapes the software industry.

“The fact that BDCs report the same loan differently does create a problem. There’s an expectation that there’s a uniform approach to things, but it doesn’t necessarily tell the whole truth,” said Raymond James’ Dodd. “The AI revolution — what it’s doing to software and how it functions as a business — it completely upends what the historical guidelines called for.”

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.