Tesla Inc. has long been an odd member of the ‘Magnificent 7.’ Strangely, its renewed efforts to fit in better only exacerbate that condition.

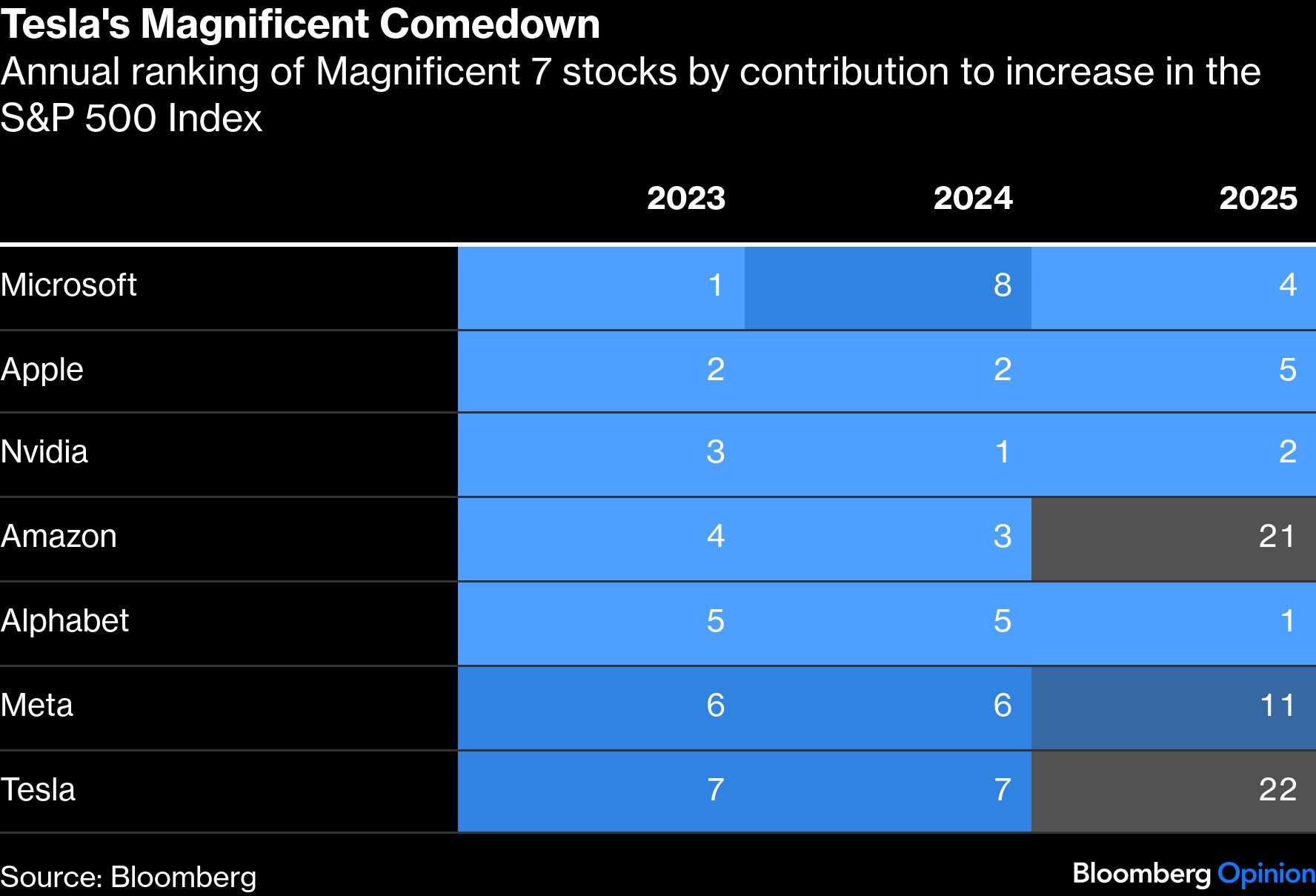

The term was coined in 2023 to describe seven stocks leading gains in the S&P 500 Index: Alphabet Inc., Amazon.com Inc., Apple Inc., Meta Platforms Inc., Microsoft Corp., Nvidia Corp. and Tesla. That first year was the only one in which they lived up to their billing, holding all seven of the top spots. By 2025, some looked decidedly less magnificent than others.

The obvious lesson here is that this designation — like ‘FAANG’, ‘Nifty 50’, and the lyrical ‘MANAMANA’ before it — is past its prime. Yet Tesla’s intensifying pivot into artificial intelligence, and the parallel reorganization of Chief Executive Officer Elon Musk’s business empire, lend the label a newfound usefulness, if only because it shows what Tesla is not.

While centered on stock performance, the Magnificent 7 became synonymous with Big Tech. This also makes Tesla’s inclusion incongruous since it is, primarily, a maker and seller of electric vehicles and, increasingly, battery packs. Sure, Apple also makes money from selling discretionary consumer products, and Amazon’s giant e-commerce platform feels closer to retail than AI. But both are undeniably information technology giants, and profitable ones at that. While Tesla does boast technological chops, especially in terms of EV design and advanced driver assistance systems, its more recognizably tech efforts — robotaxis, humanoid robots, chipmaking plans — are more like research and development than actual commercial businesses.

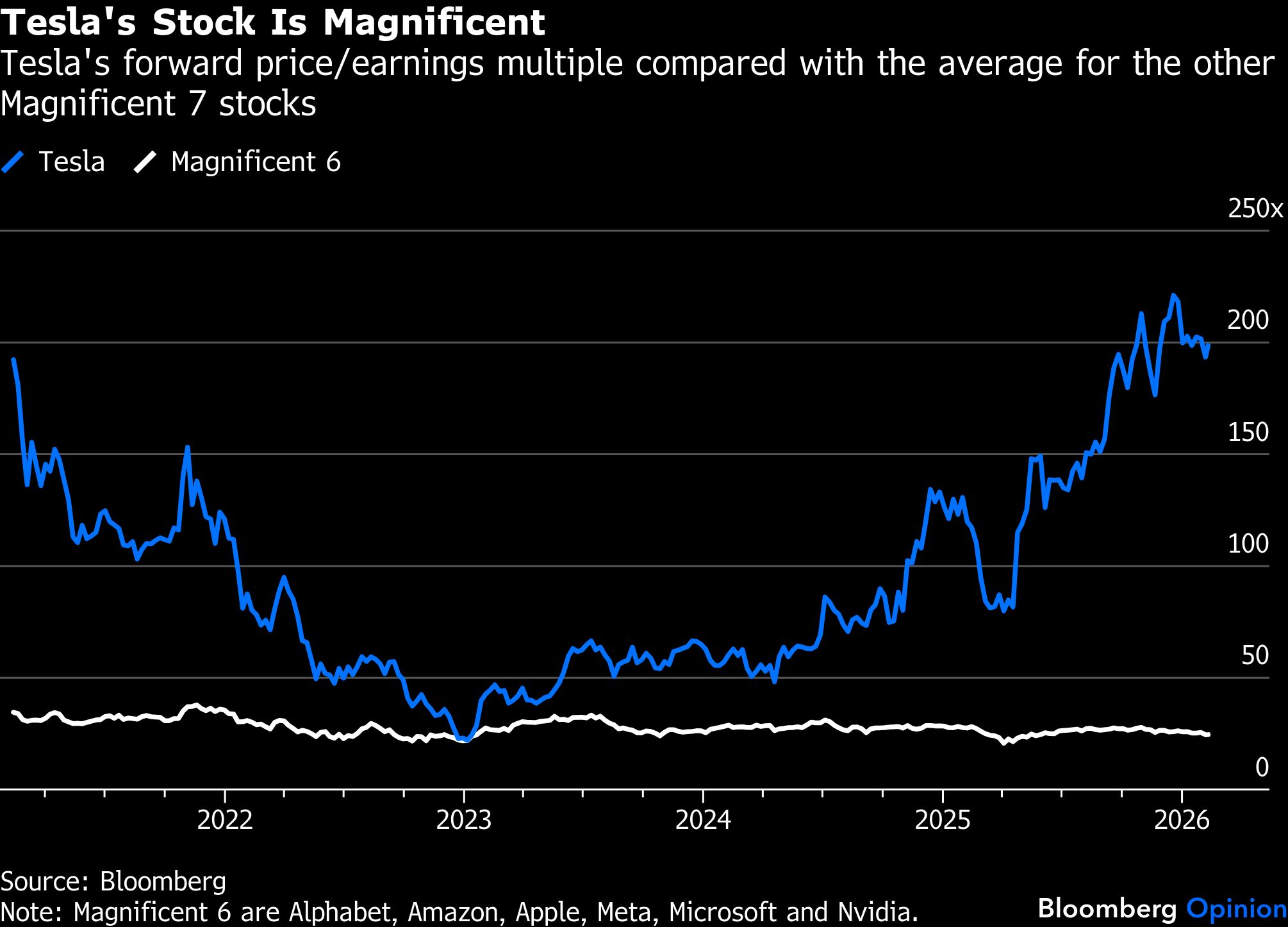

The thing that put Tesla into the Magnificent 7, its valuation, also signals that it isn’t like the others. Here’s Tesla’s forward earnings multiple compared to a simple average for the other six.

A soaring multiple is an investor’s dream, but in this case it mostly reflects a growing disconnect with deteriorating fundamentals: Two-thirds of that expansion over the past three years is explained by falling earnings forecasts. Tesla is the only member of the group whose reported earnings actually declined over that period.

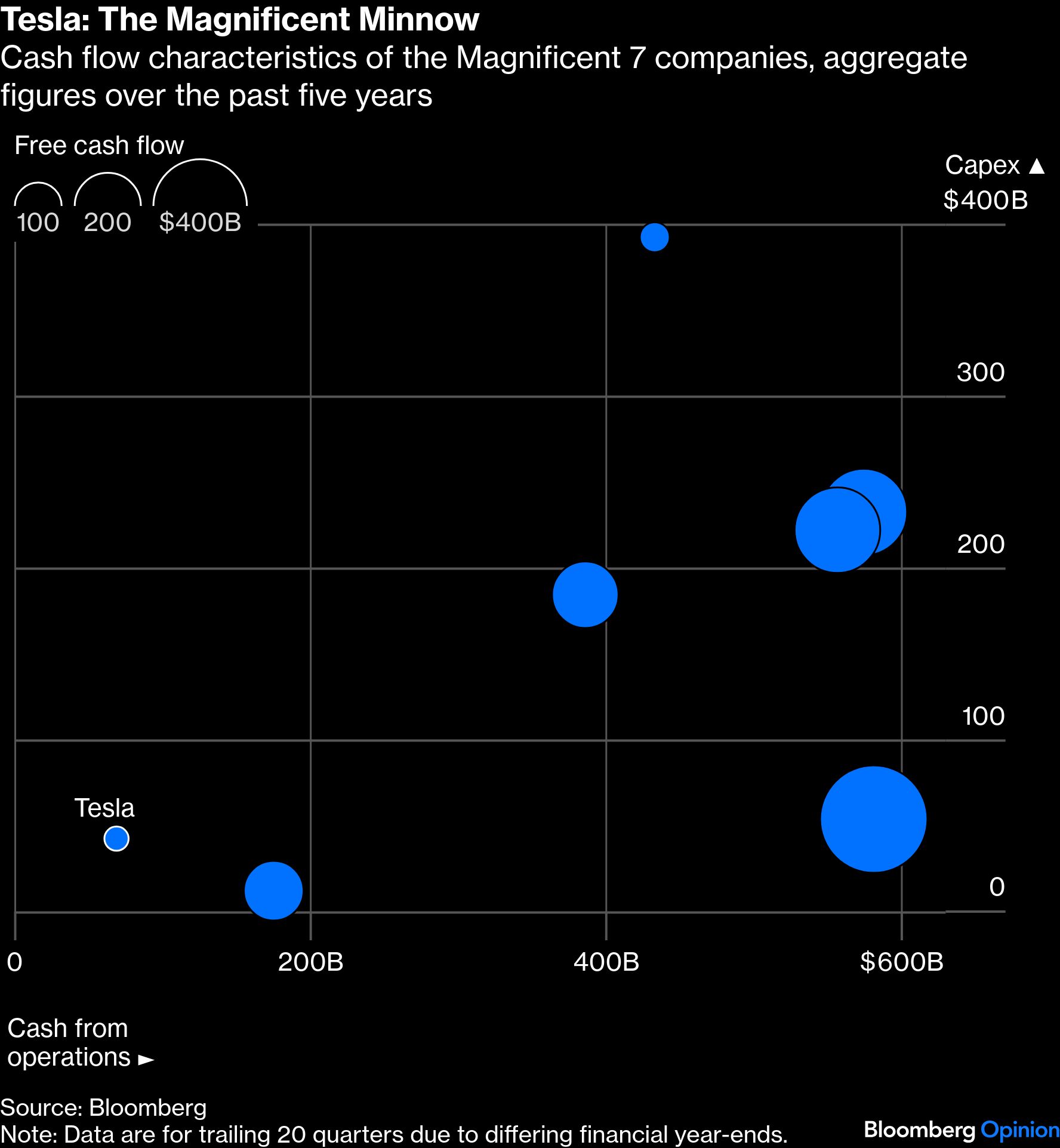

Cash flow is the real tell, and especially pertinent with Tesla planning to more than double capital expenditure this year. In terms of cash from operations, capex and what’s left over — free cash flow — Tesla is simply not in the same league.

Sure, Amazon’s free cash flow over the past five years is ‘only’ about 50% bigger than Tesla’s $27 billion. But that reflects Amazon’s capex being nine times bigger. Think of it like this: Apart from Amazon, every other member of the Magnificent 7 made far more free cash flow in just the past year than Tesla made across five years.

Sheer size isn’t everything, but in this case it counts. Tesla is recasting itself as an autonomy, robotics and AI leader. Its capex budget for 2026 of about $20 billion will push free cash flow sharply negative for the first time since 2018. Yet that budget is only about one-ninth of what, for example, Alphabet is forecast to spend — and that company is still expected to generate $34 billion of free cash flow in 2026.

The discrepancy in cash flow reflects the underlying businesses. All of the other members can be considered leaders, or even dominant, in their respective fields. Tesla can be considered that way if you focus narrowly on battery EVs, where it is the second-largest seller in the world. But the pertinent metric is that Tesla has a 1.8% share of global vehicle sales. Certainly, its high EV ranking doesn’t translate to high profits, with an operating margin of less than 5% compared with a range for the other six between 11% at the low end, Amazon’s, and almost 60% at the top end, Nvidia’s.

In other words, if you want to build a technology giant, a car company is a tough place from which to start. In terms of competing in AI and potentially even chips, Tesla is up against the massive budgets of several other Magnificent 7 members, who can, nonetheless, cover their spending with operating cash flow. Tesla also competes with Alphabet’s Waymo LLC, which just raised $16 billion to expand its robotaxi operations, and the likes of Open AI LLC, reportedly targeting an initial public offering at a $1 trillion valuation as soon as this year.

This offers some context for the reshaping of Musk Inc. Tesla will burn cash this year, and has told investors it may require “additional funding.” Tapping the public equity market is deeply ingrained in Tesla’s DNA: It has done so 11 times in its history, according to data compiled by Bloomberg, almost as many as for all six of the other Magnificent 7 members combined.

Meanwhile, xAI reportedly torches about a billion a month. SpaceX reportedly made $8 billion of Ebitda last year, which would be a plus, but that doesn’t take account of capex. For example, only 39% of Tesla’s Ebitda converted to free cash flow over the past five years. Plus, SpaceX just took on xAI’s furnace. Tesla does have more than $40 billion in the bank, but sustained draws on that could unnerve investors, unflappable as they seem. As could a mooted combination of all three companies, which would raise the possibility of that bank balance being spread across multiple ventures.

A successful IPO for SpaceX, bringing in perhaps tens of billions of dollars of fresh money, looks important not just for that company but the broader empire. Questionable as Tesla’s status as the Magnificent 7th might be, Musk could really use an 8th.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.