If inquisitive investors wanted to measure the demand for AI with some actual numbers, one place they might look on the balance sheet is the line reading “remaining performance obligations,” known more simply as the backlog.

The number reflects the total dollar value of contracts signed with customers for cloud computing that has not yet been delivered. This might be because the company doesn’t have the necessary capacity to fulfill it, or the client doesn’t need it yet (but has promised to buy it), or some other opaque combination of factors. It exists as a guide for investors to model potential revenue and for the companies themselves to plan (and justify) their enormous capital expenditures — albeit an imperfect one that raises questions for both sides.

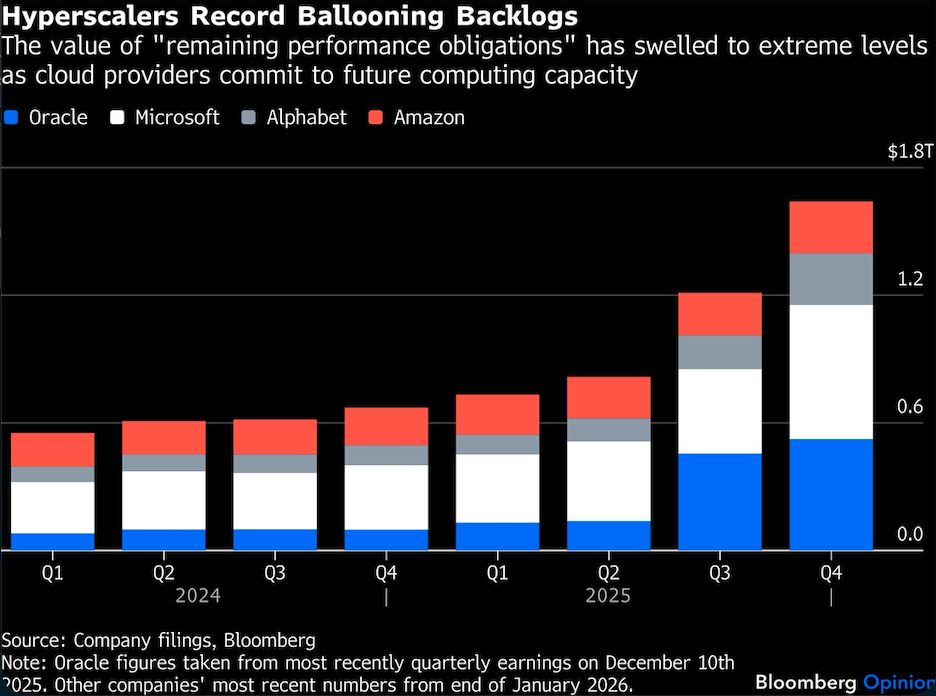

The metric floated relatively under the radar — until, that is, the AI boom and the subsequent scramble for data centers. Today, the backlog of the four biggest hyperscalers — Amazon.com Inc., Microsoft Corp., Alphabet Inc., and Oracle Corp. — exceeds $1.6 trillion, up 146% from last year.

Microsoft has the largest obligations of the four. Its backlog increased by $327 billion in the same period, to $625 billion. Of that, 45% is from a single client, OpenAI. The fortunes of Oracle are similarly tied to the ChatGPT maker and the US government-backed Stargate project. Its backlog, as disclosed at the of last year, stands at $523 billion, a more than fourfold increase in a year.

Will OpenAI be good for the money? There’s no telling what condition the ChatGPT-maker will be in, as it hurries to monetize away its heavy losses with experiments in ads and shopping, by the time the capacity is ready to be used. “It’s a legal contract that OpenAI is committed to, yes, but they actually have to do well to pay the bill,” emphasized Jefferies analyst Brent Thill. I called Thill after hearing him put his concerns about OpenAI’s enormous share of Microsoft’s backlog to the company’s chief financial officer during the firm’s most recent earnings call. The rather terse response was to focus on the remaining 55%; a more reassuring answer might have been to talk up its biggest client, though the two are frenemies at best right now.

The question of survival applies to other AI companies, too, of course, but none have committed to as much compute buying as OpenAI. The “circular deals” that have become a trademark of the AI business could become circular failures. The weekend after Microsoft disclosed its latest backlog figure, Jensen Huang, the chief executive officer of Nvidia Corp., was stopped in the street by eager reporters in Taipei, one of whom asked whether his company was going back on its decision to invest up to $100 billion into OpenAI. “There was never a commitment,” Huang said. This seemingly prompted Oracle to post on X that its deal with OpenAI was not contingent on Nvidia’s money. “We remain highly confident in OpenAI’s ability to raise funds and meet its commitments,” the company added. You can understand why there might be a few jitters out there.

The pressure is by no means one-sided, however. Just as uncertain as AI companies’ ability to pay is the hyperscalers’ ability to deliver. Building data centers is a complicated and volatile business, one that is becoming increasingly expensive and, as we head to the midterms, more politically charged than ever. Falling short could steer some of that backlog toward the “neocloud” companies like CoreWeave Inc. or Fluidstack, though they aren’t immune from the challenges of building data centers either — CoreWeave’s own backlog is around $55 billion. This is a global problem, with plans being derailed as jurisdictions put in place moratoriums against new data centers or insist they can be built only if the power stations they require are built first or slow things down with other stipulations.

For these reasons, just 10% of Oracle’s backlog is expected to serviced in the next 12 months, the company said, and 30% over the subsequent 13 to 36. In AI years, that will feel like a century. Similarly, Microsoft expects to recognize just 25% of its backlog this year.

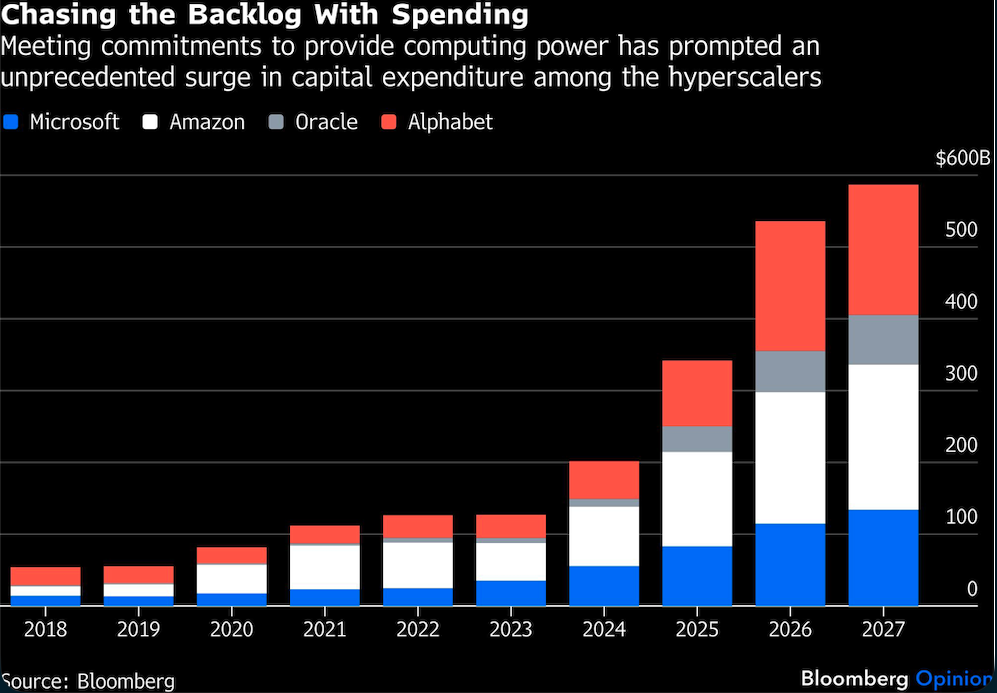

And then the perennial question: Will it be worth it? In 2025, Microsoft’s 58% capex increase translated to 22% higher cloud revenue. Across all the major cloud providers, investment will further outpace returns in 2026. Ballooning backlogs are a reassuring sign that demand is solid and potential revenue boosts are just around the corner, but a conscientious investor should treat the figures as aspirational rather than guaranteed.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.