Private Credit Should Worry About a Singularity in Software Debt

Artificial intelligence fears have ripped through stock and bond markets, but investors in loans and private credit are still playing catch-up. Part of the problem is working out which areas of the debt market are exposed to disruption and which aren’t. Because fund managers apply industry categories in varying ways, some companies that are really software sellers are misclassified as anything from retailers to food producers, according to Bloomberg News.

Different business models within the software industry — whatever their labels — will prove more or less vulnerable to AI disruption. Investors in loan-focused mutual funds, collateralized loan obligations, business-development companies (BDCs) and private-credit funds all have work to do to comprehend their holdings. Only then can they start to assess which credits might be at risk of default, or refinancing problems, or other shenanigans that could lead to losses down the track.

Within the relatively transparent world of BDCs, at least 250 loans to software firms worth more than $9 billion were categorized as some other kind of business by one or more of those often publicly-traded vehicles that invest in private credit, Bloomberg News found. A pricing-software business called Pricefx was labelled “business services” by one lender, while Restaurant365, which supplies software to eateries, was called “food products” by another. Such idiosyncratic classification doesn’t make the business more likely to be blown up by AI — but it sure doesn’t help investors.

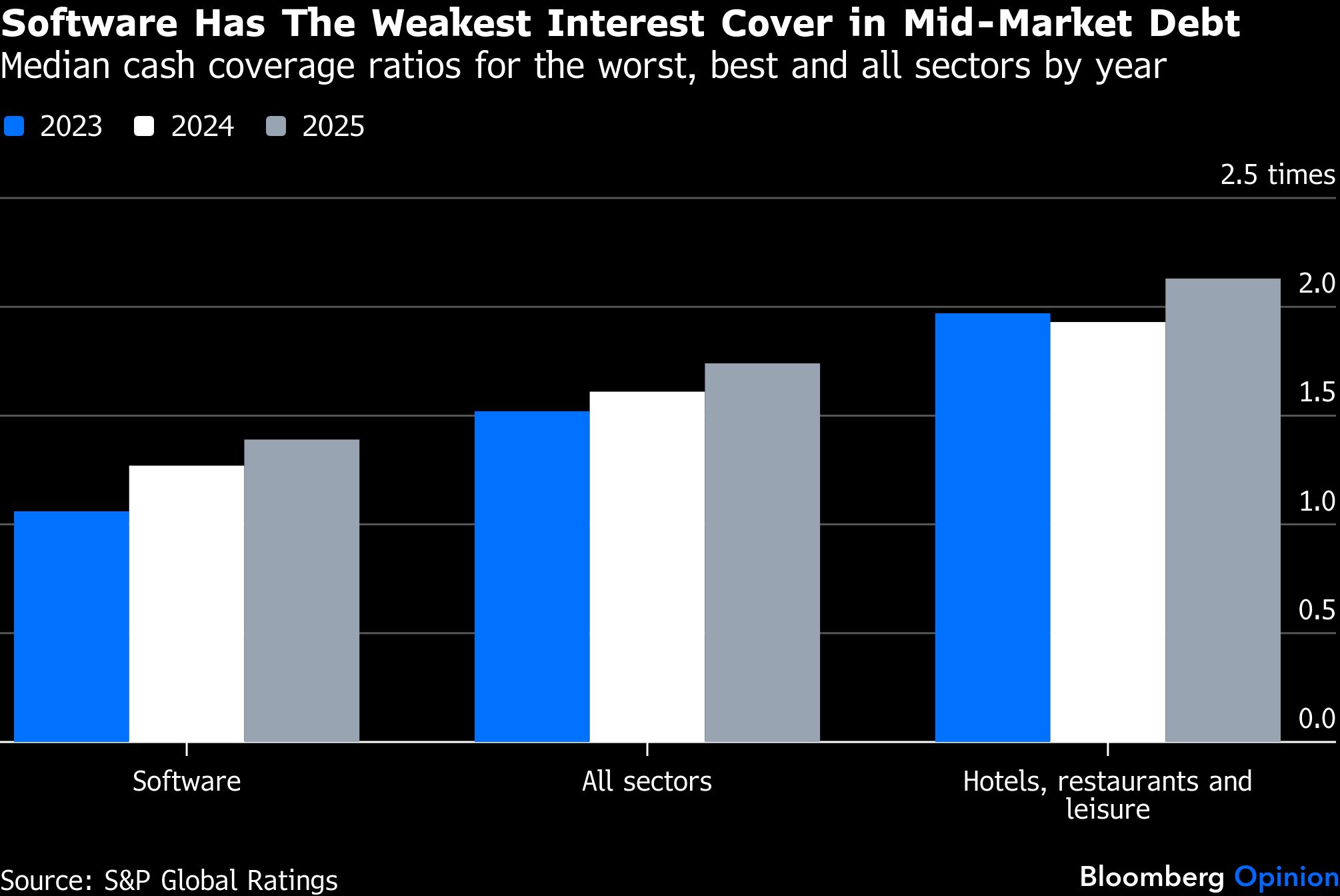

In fact, software is the biggest single industry among private-equity-backed businesses, however you cut it. In mid-market CLOs, which package up loans to smaller companies and are a good proxy for private credit funds, software makes up 19% of portfolios, according to analysis by S&P Global Ratings. Another ratings company, KBRA, categorized borrowers using its own data on mid-market CLOs, BDCs, and bonds backed by companies that got credit based on their recurring revenue. It found that 22% of this debt by value was owed by software firms.

Private equity and private credit managers have fought back against the disruption fears stalking their assets. Several listed managers, for example KKR & Co. and Apollo Global Management Inc., said on earnings calls this month that they had already cut software exposures through sales over the past couple of years. Others, including Ares Management Corp., said the share of their portfolios invested in the sector was significantly smaller than the industry average.

Bankers and other managers, meanwhile, have been highlighting the low loan-to-value ratios of many deals. Marc Lipschultz, co-chief executive officer of Blue Owl Capital Inc., told shareholders two weeks ago that its software loans on average were granted at just 30% of the borrowers’ enterprise values (the sum of their equity and debt). Even after the recent selloff in public software stocks, companies are still worth more than two years ago, Lipschultz said, suggesting the same applied to private-equity backed companies in the same space.

“If the software business evolves over time, well, that'll be to the benefit or loss of the equity holders,” he said. “But we're in a position, we think, to continue to get our capital back and earn a very strong return.” For lenders to really lose significant money, more than 70% of the total value of these businesses would need to be destroyed, he added. In other words, the equity would have to go to zero.