I hate it when people ask if I have any hobbies. I know they are well-intentioned, just trying to get to know me, but how can I explain my hobby is … collecting credit card points?

I am embarrassed to admit how many hours I spend reading blogs, watching videos and mentally plotting out my non-linear objective function. I don’t have the words to describe how much sweeter the Prosecco is in business class when it comes from a hard-won upgrade. It would be so much easier if I just played pickleball.

Still, my embarrassment had never been so bad that I would reconsider my priorities. Until now: The story of Bilt, as told in a Bloomberg Businessweek story earlier this month, may be what breaks me. Bilt, which became known for offering a credit card that enables users to earn rewards on their rent or mortgage, shows what can happen when people feel compelled to get points on every transaction.

I love my points, and always thought they were a harmless pursuit. But I am starting to think otherwise because the size of the points industry could be making the economy less efficient. It is leading people to make poor financial decisions, introducing uncertainty into the economy, and misdirecting resources that could be better used elsewhere.

Just in terms of my own limited resources, I think of the time I devote to the game, even if I do extract some utility and enjoyment from it. Every time I buy something, I think about what card to use. I spend a lot of effort planning how to use my points. And each year the rules change, forcing me to reassess my strategy. If I spent all that time on my pickleball game instead, I might be healthier and have more friends.

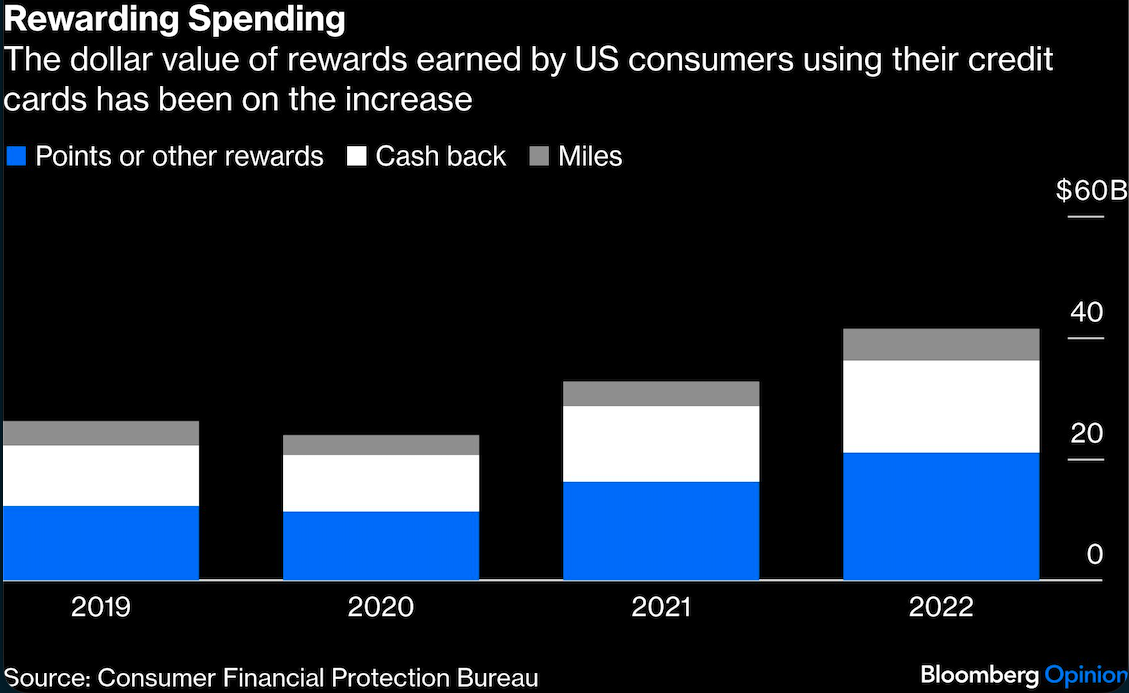

It is not just me. Some 5.5 million Americans pay for their housing with Bilt, suggesting they are even more fanatical than I am — that’s a lot of lost productivity. A whopping 80% of bank customers say they have at least one rewards card, and with cash becoming increasingly rare, points have become a byproduct of almost all our transactions. A large shadow currency exists that is subject to a significant and unpredictable devaluations, which can’t be good for the economy.

Bilt’s recent financial troubles illustrate the costs of points: So many people were using it to pay their rent or mortgage, usually their biggest monthly expense, that the bank that issued the card was losing money. Bilt had to rework its program to become more like other rewards programs; customers can still use it to pay their rent, but they also have to meet other usage thresholds.

Usually consumers share the costs with merchants in the form of higher interest charges, higher fees or higher prices. Banks and award partners are the primary beneficiaries. In 2019, the largest US banks paid out $35 billion in rewards and reported $89.7 billion in interest income and $9.9 billion in fee income from credit cards, in addition to $41.3 billion income from interchange fees.

It is hard to say if there is much economic benefit or cost to increased bank profits. On the one hand, it may allow banks to issue more credit to lower-income borrowers with worse credit. On the other, the point game is regressive. Whether customers come out ahead depends on how good their point game is; more financially sophisticated card users come out ahead (or so we like to think). Lower earners also tend to use debit cards or cash, but they still face the higher prices passed on by merchant and get no points.

The other big winners are the airlines, which earn more selling points than they do flying planes. Points subsidize travel in a risky industry, meaning lower fares, better coverage and more predictability for the airlines. Perhaps airlines would be better-run if they did not have the large bank subsidy.

Efficient or not, the points economy is about to change. The Credit Card Competition Act is gaining bipartisan support, including from President Donald Trump. It would allow merchants to bypass Visa and Mastercard and introduce more competition into so-called swipe fees, which would lower costs. When something similar happened to debit cards, rewards disappeared. Another threat is the rise of payment apps that offer convenience but no rewards.

Maybe neither of these changes will kill the points economy, which is large and has an affluent customer base. But this economy will probably shrink and become less generous, making point-chasing a more costly and niche pursuit. Which may not be the worst thing, to be honest. Like gambling, the points game can be unhealthy if it takes over too much of your life — or the economy. No matter how desperate I get, however, I will never take up pickleball.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Allison Schrager