Pay for top bosses at the biggest US banks has reached new records in the past couple of years, surpassing even what chief executive officers got in the pre-crisis peak of 2007. Someday these vast rewards might run dry. After all, in the age of artificial intelligence, what is a CEO even for?

A prediction that many white-collar jobs will be automated away within 12 to 18 months gave markets a scare this month. But few people are yet asking what protects those in the C-Suite from similar future irrelevance. If the capabilities of autonomous AI keep leaping forward, the importance of executives will surely be downgraded to echo that of the technical staff who watch over robots in a modern car factory.

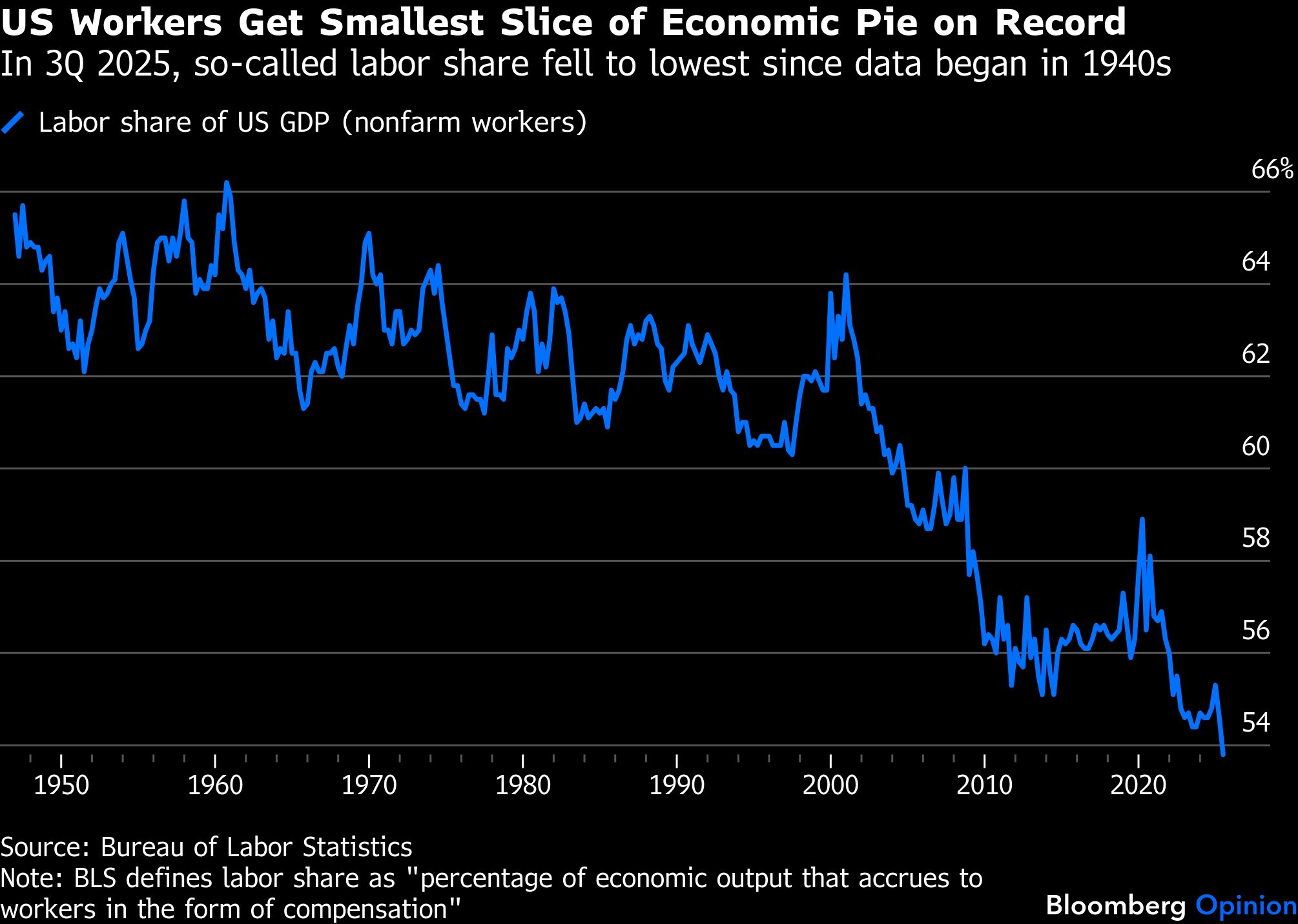

Simple economics tells us that the more work is done by machinery or software, the greater the share of profits that should go to owners rather than any form of labor, no matter how grand the latter’s offices and titles might be today. Indeed, the US is already setting new record lows for the share of gross domestic product that goes to labor: It fell to less than 54% in the third quarter of 2025, the smallest recorded by the Bureau of Labor Statistics in data going back to 1947. Only 20 years ago, it was still in the low 60s.

Big banks have always been close to the sharp end of technology and automation, as well as the use of intangible capital — the licenses, brands and ideas that can generate more scalable returns than physical equipment. This helps them generate huge profits — and bonuses — when revenue increases.

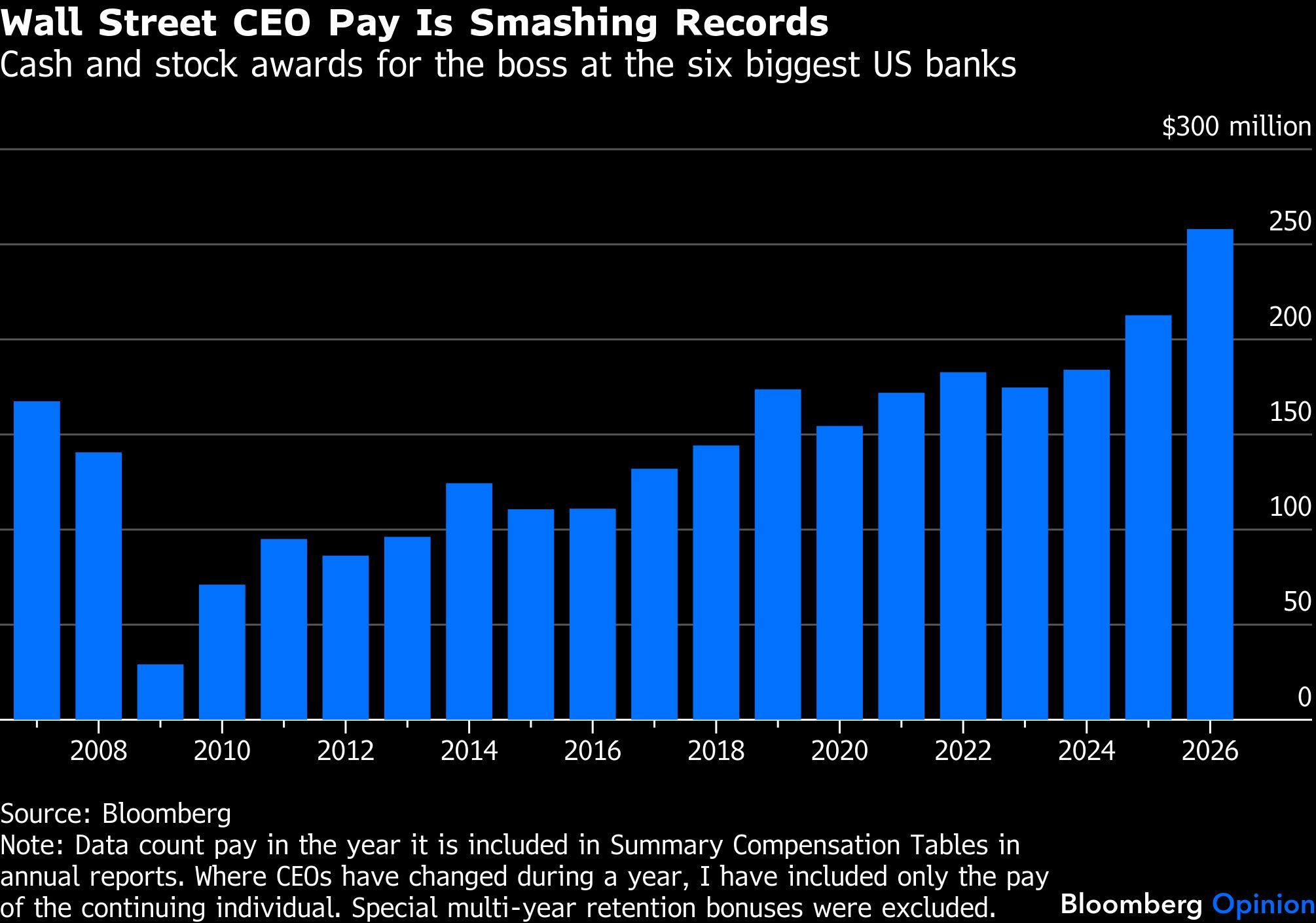

The six CEOs of America’s big banks all got total payments of more than $40 million for 2025, which took their combined income to nearly $260 million. That was easily ahead of the $213 million they got in cash and stock for 2024, which was the first time six individual finance leaders had been collectively paid more than $200 million — although this excludes special options grants like the roughly $50 million retention bonus given to JPMorgan Chase & Co.’s Jamie Dimon in 2021.

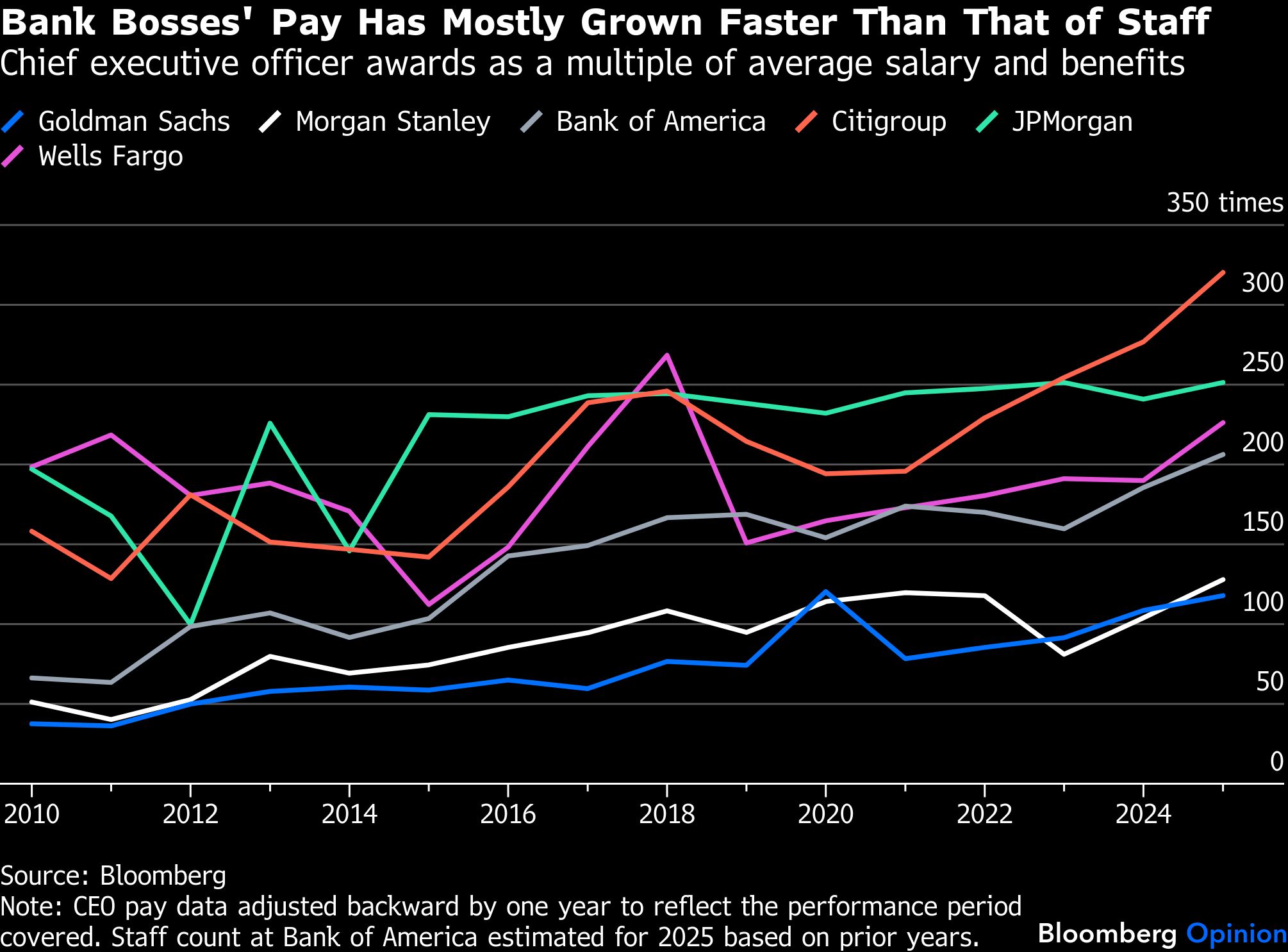

JPMorgan spends more on technology than any other bank — more than most banks even make in revenue — and it has the lowest bill for salaries and benefits as a proportion of revenue among the big six. The firm with the next lowest costs by that measure is Goldman Sachs Group Inc.; it’s cut the share of income that goes to labor consistently over the past 20 years. That’s something few others have managed.

One thing true for all banks, however, is that CEO pay has grown faster than average employee costs since about 2010. It ranges from roughly 120 times at Goldman Sachs and Morgan Stanley to more than 300 times for Jane Fraser’s latest package at Citigroup Inc.

If you think widespread AI automation is coming, you should expect all these numbers to change in the years ahead. First, total salaries and benefits should shrink as banks need fewer people to do the same things. Next, the pay differences between staff should shrink as each individual that works with AI becomes much more productive. Finally, everyone’s pay should decline as the decisions and actions they take become ever less significant in the workings of an increasingly autonomous machine. And yes, that includes the CEOs. Goodbye billionaire bosses!

But how likely is career death for CEOs, or anyone else, even if you believe this radical robot future? There’s a well-known wrinkle in the workings of companies known as the principal-agent problem: The interests of the shareholders — the principals — don’t always match those of their managers or agents. To combat this, executives are paid mostly in stock to help keep them on the same page as other stakeholders. But bosses are different from other owners, with jobs and salaries they’ll want to keep. Acting as intermediaries between shareholders and the business itself should remain powerful and necessary roles.

And, to be honest, I’m not convinced by the idea of fully autonomous banks or anything else because there are things that AI can’t do today and probably never will. These are the decisions that need to be made before a robot can even be put to work.

For example, I recently spent time with a company called ArabesqueAI and its AutoCIO platform, which forecasts how company shares will perform in the near term and claims to be incredibly efficient at constructing a portfolio. It’s very impressive, but to start investing a human still needs to choose whether they want income or growth, to focus their money locally or go global, to avoid dirty industries or not care about the climate crisis. And, almost by definition, AI isn’t able to hypothesize about potential black swans.

Or imagine that you produce consumer goods: Do you want to be a luxury brand, or ubiquitous? Another question for any business: Are you trying to make as much money as possible as fast as you can, or do you want to create something that keeps churning out profit for years and years? Decades ago, a senior Goldman Sachs partner called Gus Levy voiced what is meant to be a key characteristic of the investment bank — to be long-term greedy. That’s the kind of abstract goal an AI can’t set for you.

Similarly, as these machines become increasingly part of the workforce, human judgment will still be needed at many stages. Financial analysts who are already highly skilled can use existing AI tools to build their forecasting models faster, but they still need to know what questions to ask as well as what sort of answers to expect. Bankers and private equity managers will have to ensure younger staff still have a proper sense for numbers and for what the point of their work is. The same human intuition and vision remains essential for creating cars, handbags or anything else.

And as long as humans remain involved, there will be culture and competitiveness, politics and hierarchy, all of which need to be managed, as this great essay describes. And we haven’t even mentioned relations with regulators, politicians, or customers. In industries like finance, AI is likely to be a great leveler in terms of skill and productivity. That ought to compress pay differentials between all staff. The CEOs will likely be whoever is best at managing the moods and expectations of everyone else – and at acting as the go-between with the owners, too.

Capital probably will continue to take a growing share of the profits in the coming years, but I’m sure top bosses will still convince everyone else that they deserve very healthy rewards for watching over it all.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Paul Davies