A tweak here, a twiddle there, and now possibly a 3% sweetener on the price. It’s all progress. But the billionaire Ellison family has yet to make an offer for Warner Bros Discovery Inc. that clearly beats the studio’s December deal with Netflix Inc. Now it’s time to see what tech luminary Larry and film producer son David can really deliver.

On Tuesday Warner boss David Zaslav finally agreed to takeover talks with Ellison-backed Paramount Skydance Corp. — if only for a week. Netflix has consented. Despite persistent gaps in the rival suitor’s pitch, this was the right step by Warner. Paramount last week delivered high-level answers to objections to its then $30-a-share proposal, which valued the Hollywood firm at $108 billion including debt. Now the Ellisons are dangling $31 per share, taking it to about $111 billion.

Zaslav would have had a tough job writing a credible rejection letter. And by agreeing to talks, he hasn’t conceded much negotiating leverage. Warner’s trump card remains the value to Paramount of securing an agreed deal. That would lay out a smoother path to ownership than having to make a hostile offer. Zaslav’s task is to extract the juiciest possible sweetener in return for his endorsement.

Warner has outlined how Paramount can fix the remaining flaws in the fine print of its proposal. These broadly involve covering Warner’s costs if any Paramount tie-up fails to pass regulatory muster. Assuming the Ellisons mean what they say about backstopping these expenses, this should just be some extra work for the lawyers.

A trickier issue is whether the Ellisons would inject more equity in the event their debt financing had to be scaled back. Larry is underwriting more than $40 billion of the price right now. He’s worth $213 billion even after a $35 billion hit to his wealth this year. Going higher doesn’t look too difficult. But can he make a cast-iron commitment?

Paramount must address these potential objections to match Netflix when it comes to the what-ifs in any deal. On the central issue of price, camp Ellison was arguably ahead even before dangling a sweetener. Netflix is offering $27.75 a share in cash and leaving Warner shareholders with the legacy cable-TV operation they currently own. Whether adding in the value of that unloved business closes the gap on Paramount’s first offer, let alone its raised one, depends on which analyst’s calculations you trust.

Of course, Paramount needs to do more than beat Netflix’s existing deal. The Ellisons must make an offer that forces the streaming giant to give up its pursuit rather than simply counterbid.

What’s Paramount’s pain barrier? The suitor benefits from the vast cost-cutting potential of combining its own cable assets with Warner’s. Thanks in part to those expected savings, it can justify $35 a share, reckons Bloomberg Intelligence. Such a price would also clear the value of Netflix’s offer combined with a super-optimistic valuation for Warner’s cable assets.

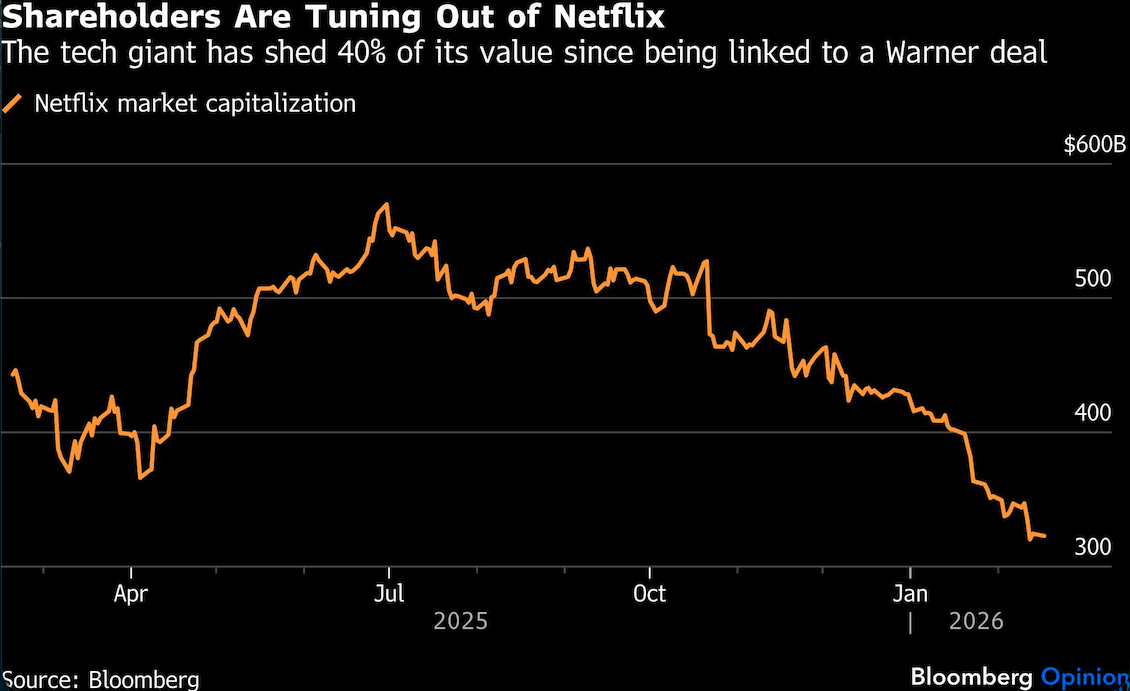

Netflix can afford to raise, too, thanks to its strong balance sheet and plentiful cash generation. Justifying such a move to its investors is another matter. The company has shed 40% of its market value, or more than $200 billion, since being linked to Warner.

The prices being offered for Warner are nearly 150% higher than its share price before the interest emerged in September. Even if the auction ended today, Zaslav has done a stellar job for his shareholders.

But he should still be greedy on their behalf. He now wants Paramount to make its “best and final” offer. That’s a label that buyers provide only when they are confident they’re making a knock-out bid and they’re sure of no competing interest. Paramount could instead just add another sweetener while keeping its options open. That would still put the pressure back on Warner. But the Ellisons have previously stressed that earlier offers weren’t best and final. Fine. Then what is?

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.