It’s been a wild few months for software and other “middleman” stocks. First, there was “SaaSpocalypse,” in which investors dumped enterprise software purveyors that help companies manage accounts and internal workflows. Then, traders unloaded a variety of other intermediary businesses including insurance brokers, wealth managers and travel booking platforms. As one argument went, who needs expensive software subscription platforms when AI coding tools could spin up made-to-order new software in hours?1 Who needs insurance brokers or wealth managers when AI chatbots can guide consumers on their financial journeys?2

Sure, some of those fears will be validated, making bottom-fishing in individual stocks a bit of a minefield. But from the standpoint of diversified S&P 500 Index investors, these episodes of volatility may be a blessing in disguise — a sign that market psychology is shifting and the air is coming out of the AI bubble.

However imperfectly, market participants are trying to be more discerning about our highly uncertain AI future. And remarkably, the multiple on earnings that investors pay has compressed in an environment of still-rising expectations for profits, a stable economic growth outlook and falling 10-year Treasury yields. On balance, this is a net positive for long-term investors with diversified portfolios.

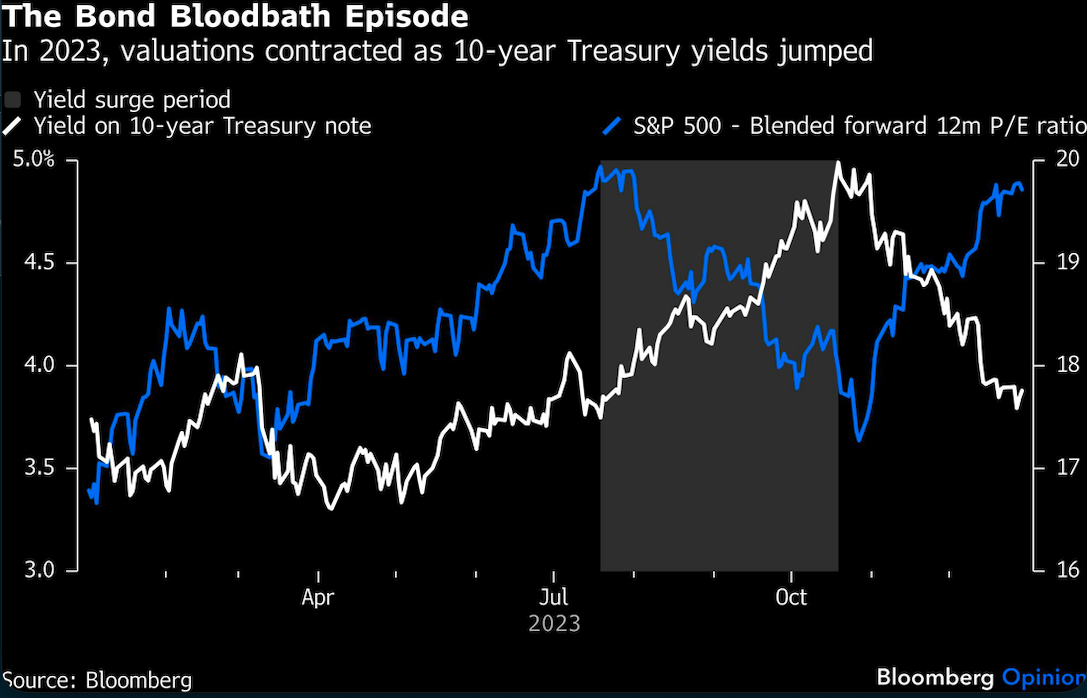

At the time of writing, the S&P 500 trades at about 21.4 times blended forward 12 months’ earnings, down from 23 times earnings in late October. That’s no bargain, yet it’s healthy to see the ceaseless expansion of multiples finally taking a breather. Since the release of ChatGPT in November 2022, the S&P 500 market-multiple has increased by a whole number roughly every six months; we were all sleepwalking toward 1999-like valuations and poised to get there as soon as late 2026.

Consider the dot-com bubble analogy (which I know is overdone, but bear with me). Then, the internet was a novel and impossible-to-forecast technology, the economy was humming and retail participation in the stock market was exploding. In the absence of any major macroeconomic disruptions, investors began to price the market as if there were no downside risks to the internet boom thesis at all. High valuations begot even higher ones, until a series of corporate letdowns — and later the 9/11 terrorist attacks — led to a fairly abrupt collapse in the proverbial house of cards. Individual investors got hurt and investment slowed, even for the most worthwhile projects.

That’s the boom-and-bust scenario we all want to avoid. In late 2025 and early 2026, by contrast, we’ve seen multiples compress almost painlessly against the backdrop of a sideways market. At present, the index is only about 1% off its all-time highs.

While multiple expansion has taken other breaks in recent years, the others have been driven by macroeconomic variables rather than a fundamental reassessment of the AI risk. For instance, the 2023 multiple contraction was driven by a 1.24 percentage-point surge in 10-year bond yields in the space of just three months.

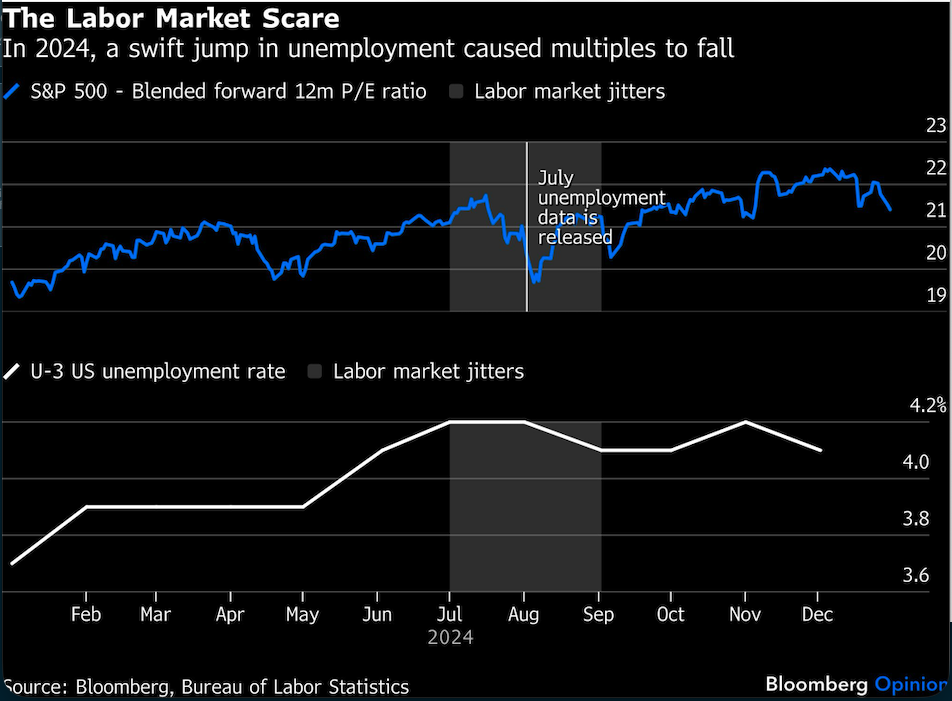

In 2024, multiples were hit again as a jump in the unemployment rate prompted recession worries.

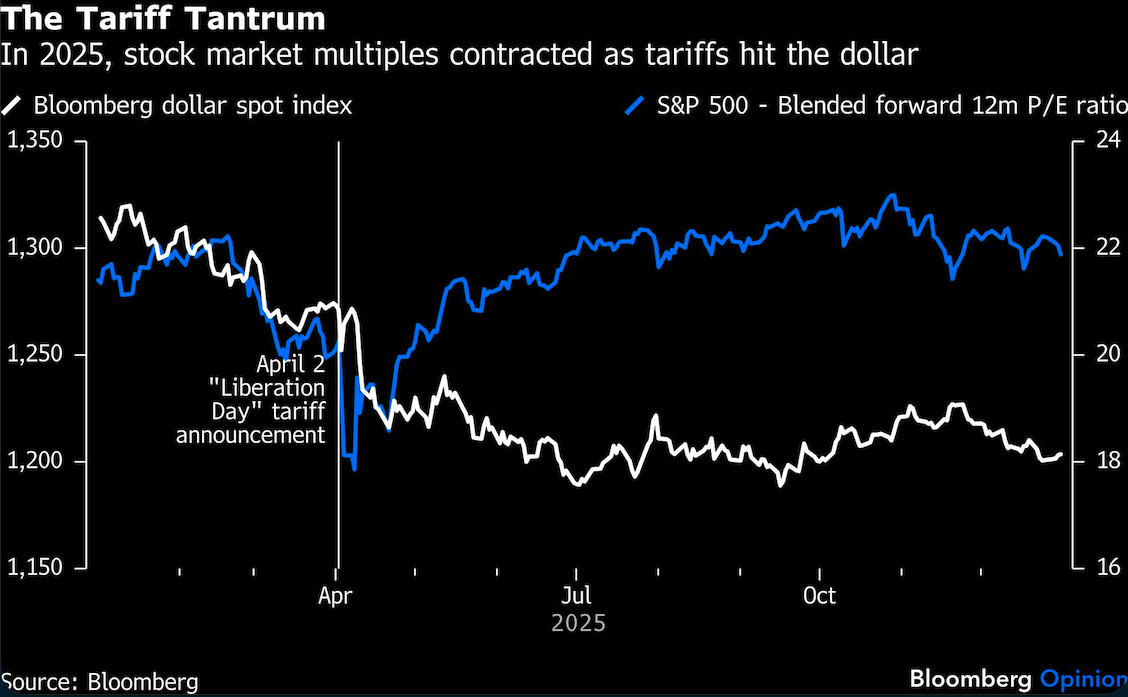

And in 2025, the P/E multiple declined in the run-up to — and announcement of — President Donald Trump’s “Liberation Day” tariffs, which clouded the outlook for corporate profit margins and American consumers. Analysts revised down their earnings outlooks and economists nudged up their recession odds. Even more than that, the announcement came across as an economic attack on essentially every US trading partner; worries mounted that it would lead to flight from US capital markets, as exemplified by the sharp drop in the US dollar. (To be sure, a weaker currency can help some companies’ earnings, but the April 2025 episode of dollar selling was fundamentally different since it suggested that America’s place in the world was under threat.)

None of those macro factors are currently at play: Bond yields have been broadly stable for around six months (and have fallen in recent weeks), and the growth outlook is strong. This is the first significant multiple contraction of the ChatGPT era that is primarily about AI itself and occurs in an environment of otherwise stable growth and interest rates expectations.

Certainly, there’s no guarantee that this one will remain painless for index investors. In one scenario, the tremors could spread and the multiple contraction could extend further. Recall that in the five years prior to ChatGPT’s release, the index had an average multiple of around 18.7 times forward earnings, so stocks could conceivably fall another 12%-13% from here on sentiment alone and we’d still only be back to “normal.”

Alternatively, dip-buyers could decide that the AI scare trade was much ado about nothing, and we could conceivably race back to a forward P/E of 23. Although AI could legitimately hurt growth prospects for incumbents that fail to innovate, it’s still something of a sci-fi fantasy to believe that the new tech will completely replace human intermediaries in the near term in fields such as insurance, real estate and investing.

Still, I wouldn’t be shocked if we’ve seen a medium-term top in market multiples (particularly with the uncertainty around trade tariffs about to enter a newly chaotic phase). Beyond just scrutinizing potential AI losers, investors are also starting to rethink the risk premia they demand to hold the premier AI companies themselves, especially as some of them now deploy the lion’s share of their free cash flow toward capex with uncertain payoffs. Something in the market’s psychology appears to have changed, and that’s a very good thing.

1 Another take posits that, since many enterprise software companies charge per user, the business model will be challenged in an environment in which AI makes companies more efficient.

2 The counterargument here is, in part, that humans are programmed to prefer human-to-human guidance, especially when it comes to major financial decisions. Maybe so, but it's hard to imagine that AI won't take a bite out of some of these businesses.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin